Understanding Cryptocurrency Tax Government

Before diving into how the SPF, the cryptocurrency tax government organ, taxes crypto activities, it’s crucial to understand the types of digital assets and platforms that are commonly involved. Each of these operates differently and, consequently, can be treated differently from a tax perspective.

Airdrops

Airdrops are essentially free distributions of cryptocurrency tokens to holders of a specific blockchain asset. They are often used by blockchain projects to promote adoption or reward early supporters. One Belgian court ruled that all instances of airdrops shall be taxed according to the capital gains tax for speculators – 33%.

NFTs

NFTs are unique digital assets that represent ownership of items such as digital art, collectibles, music, or in-game assets. Unlike cryptocurrencies like Bitcoin or Ethereum, each NFT is one-of-a-kind and cannot be exchanged on a one-to-one basis. The SPF treats NFTs differently depending on whether they are held as collectibles for personal use or as part of a professional investment strategy.

Selling NFTs occasionally as a hobby on one hand will incur capital gains taxation, while frequent buying and selling as part of a business activity could be classified as professional income.

Staking

Staking involves locking up cryptocurrency in a blockchain protocol to help secure the network. In return, users receive staking rewards, usually in the form of additional tokens. There is no official position the government holds on this regard. Some argue this is the same as movable income and thus would entail a 30% charge to the state.

Mining

Mining involves using computer hardware to validate blockchain transactions and earn newly minted coins or transaction fees. It’s different from DeFi because it requires active work and infrastructure. This is inherently considered a professional activity and thus is not charged at the 33% capital gains tax but instead at the 25% to 50% income tax.

Lending Interest

DeFi lending allows investors to lend crypto to others through decentralized platforms, earning interest on the loaned assets. Interest income from crypto lending is taxable. The rate depends on whether the activity is occasional (possibly treated as miscellaneous income) or systematic (considered professional income).

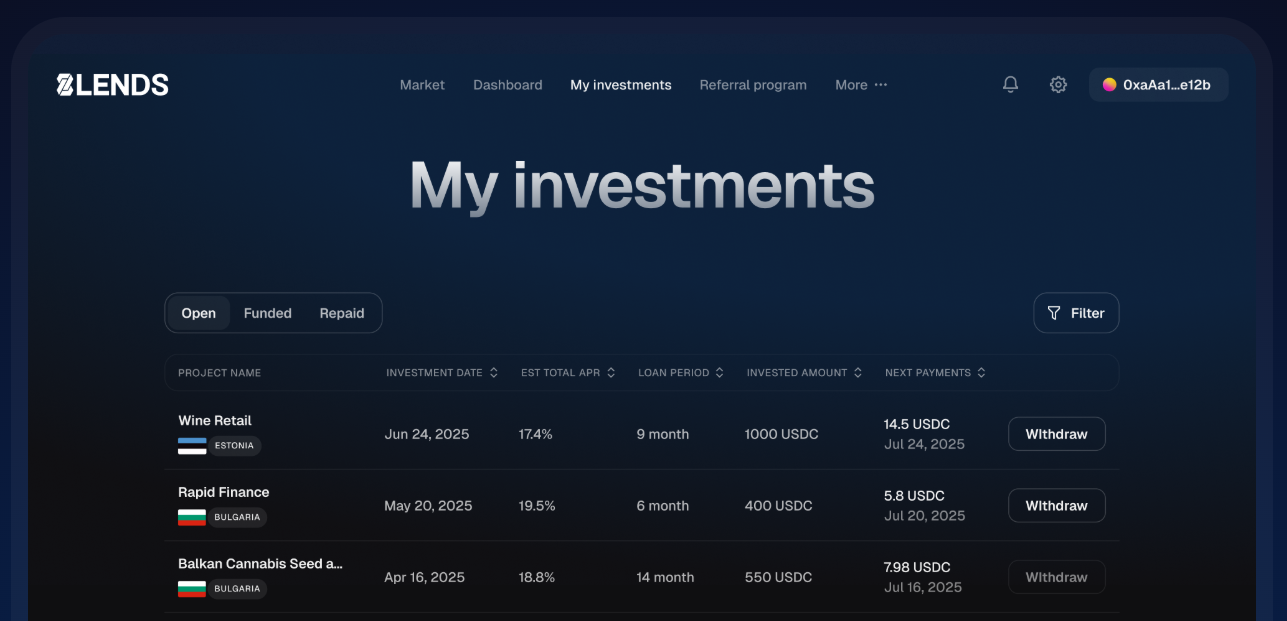

If you’re looking for a way to earn interest on your crypto while staying compliant with Belgian tax rules, 8lends offers a straightforward solution. By lending your digital assets through their platform, you can generate steady, collateral-backed returns without having to navigate complex DeFi protocols on your own. It’s a practical option for both casual investors and professionals who want to put their crypto to work safely and efficiently.

Yield Farming

Yield farming and providing liquidity involve depositing crypto into decentralized exchanges or liquidity pools to earn trading fees and additional reward tokens. Each type of reward—fees, bonus tokens, or other incentives—is taxable at the moment it is received. Suppose you provide liquidity to a pool and earn 100 UNI tokens plus €20 in trading fees. Both the UNI tokens and the fees must be declared at their euro value on the day of receipt.

Corporate Tax

It’s important to also note that if you’re running a corporation, the income tax is 25%.

How to Calculate Crypto Tax

There are specific formulas that the SPF gives to calculate crypto tax that you’re supposed to use.

Capital Gains for Speculators

This goes in Section II of the tax form. Gains from short-term or high-frequency trading are considered capital gains for speculators and taxed at a flat 33% rate. Expenses are not deductible for these people. The way the amount taxable by 33% is produced is by taking the amount or value of the asset they paid when they first acquired it and subtracting that from the sale price of the asset. That amount is then taxed by 33%.

Maxime, a Belgian software engineer, trades NFTs on weekends. In March, he bought digital monkey artwork for €2,000 and sold it two weeks later for €3,500. As a speculator, the SPF taxes him at 33 percent. His taxable gain is €1,500, so he owes €495. When Maxime also quickly lent ETH for €1,200 in interest, this short-term profit is also taxed at 33 percent, adding €396 to his tax bill.

Capital Gains for Prudent Investors

Historically, Belgian residents who are steeped in crypto have always longed to land in this category with the SPF. It’s what anyone tries to angle for when considering taxes. That’s because for their long-term, “responsible” approach, they have previously been exempt from taxes, which is a kind of treatment that few EU member states have afforded.

New 10% Solidarity Tax in 2026

However, that’s all changing now with the 10% solidarity tax that’s just around the corner, beginning on January 1, 2025. An important aspect of this that will appear in such people’s minds who, in the past, never even had to file crypto taxes is “What about my Bitcoin that I bought in 2013 for a rock-bottom price, which has since skyrocketed?”

Positive Notes

Not to worry, because the SPF does not set the actual reference cost for crypto acquisitions that existed prior to 2026. Instead, their value will be taken as of December 31, 2025. Regarding this new reference value at a date after the fact, you also need not worry if your original purchase date was higher than on December 31, 2025, since in such a case, your actual original reference cost can be used.

Another silver lining to this new tax is that you will get a 10,000-euro allowance, which will be tax-free. By the way, this new tax and allowance apply to all your assets, not just “miscellaneous” crypto assets. If you are also an extremely principled person and want to avoid paying any tax, if you change residency to another country and wait 24 months before selling an asset, it will no longer evoke tax obligation to the Belgian government.

Maude, a French expat and casual investor in Antwerp, bought two Bitcoins in 2013 for €500 each and held them long-term. By December 31, 2025, they’re reference cost is reset to the Bitcoin rate as of that date, which is around €105,000. Then in 2030, she resells her BTC for 200,000 each. With the new 10 percent solidarity tax and the €10,000 allowance, her taxable gain is €85,000, resulting in €8,500 owed.

Ordinary Income Tax for Professionals and Employees

Normal employees in Belgium use the same income tax structure as crypto professionals are required to use, with brackets from 25% to 50%; however, the way it’s calculated differs from most countries, in a way that works out cheaper than it sounds. Expenses related to the activity (hardware, electricity, platform fees) can usually be deducted as well.

Lars, a Dutch mining entrepreneur living in Belgium, runs five mining rigs and actively participates in yield farming and lending on DeFi platforms. Over the year, he earns €15,000 from yield farming, €3,000 from lending interest, and €25,000 from mining, for a total of €43,000. Deducting €6,500 in business-related expenses such as hardware, electricity, and platform fees, his taxable income is €36,500.

Using Belgium’s progressive income tax brackets:

- Lars pays 25% on the first €13,870 (€3,467.50);

- 40% on the next €10,610 (€4,244);

- 45% on the remaining €12,020 (€5,409)

This brings his total tax owed to €13,120.50. His activity qualifies as professional because it is systematic, large-scale, and profit-oriented.

Conclusion

Navigating how airdrops, NFTs, and DeFi are taxed by the SPF can feel complex, especially with distinctions between speculators, prudent investors, and professionals. The key is understanding how your activity is classified and keeping accurate records to stay compliant. Whether you’re holding long-term, trading actively, or running a professional crypto business, being informed helps you plan smarter and minimize surprises.

For those looking to make their crypto work while keeping things simple, 8lends offers a secure, collateral-backed way to earn interest on your assets. By lending through their platform, you can generate returns efficiently, giving you more time to focus on strategy rather than complicated protocols or tax uncertainty.