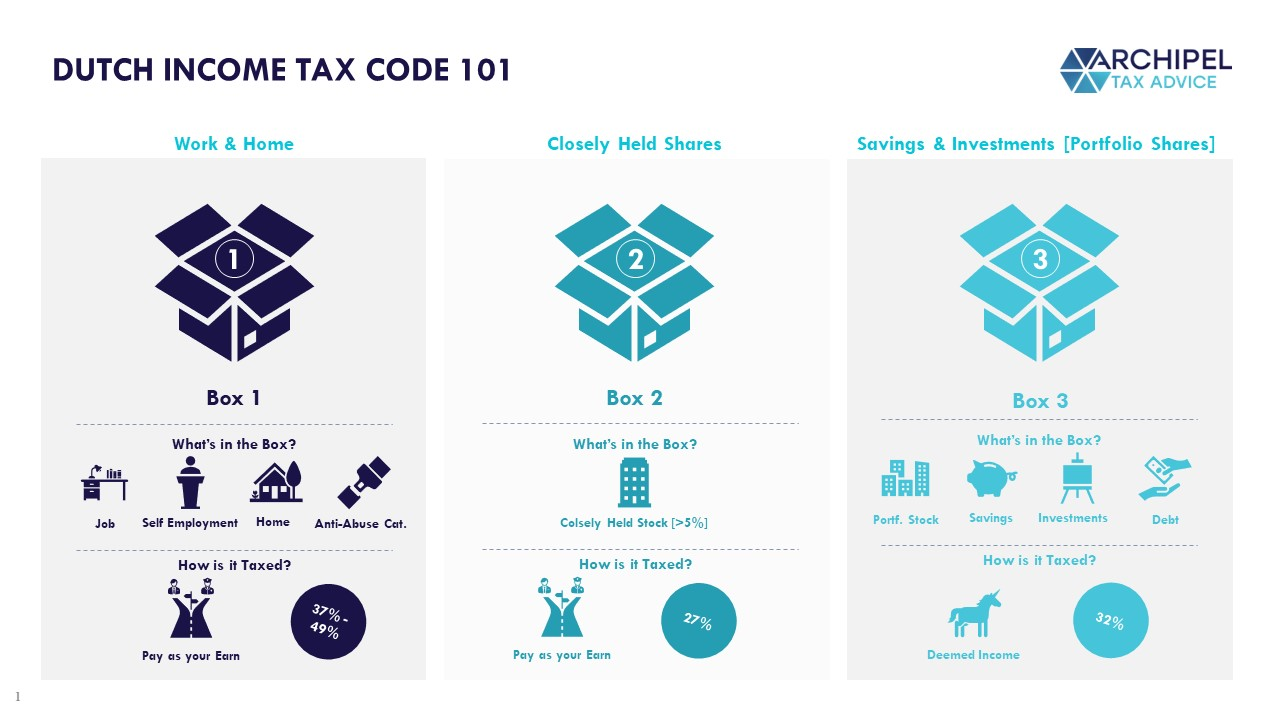

How to Pay Tax on Crypto: Box 1 vs 3

Before you can understand which crypto deductions you can claim when you declare crypto with the Belastingdienst, you first need to know how your crypto activity is classified for tax purposes. Dutch tax law separates crypto into two main buckets: Box 1 (income from work and business) and Box 3 (wealth and investment income). The difference isn’t just academic – it determines whether you can claim deductions at all, and which ones apply. If you have a non-crypto day job, you put that in Box 1 anyway though.

Net Worth

If you’re just an ordinary investor and not somebody who does it as one of their primary professions, Box 3 is going to be where you pretty much put all your crypto income sources. This is the same place you’d insert stocks, bonds, condos or homes you own, as well as dividends.

You also put your deductions here, which would be either the 57,000-euro standard deduction if you opt for the presumed wealth calculation, or it can be any form of debt or liabilities you’re paying for. These will both reduce your gains, fictitious or not. If you had less than the standard deduction in capital appreciation, that means you pay nothing at all.

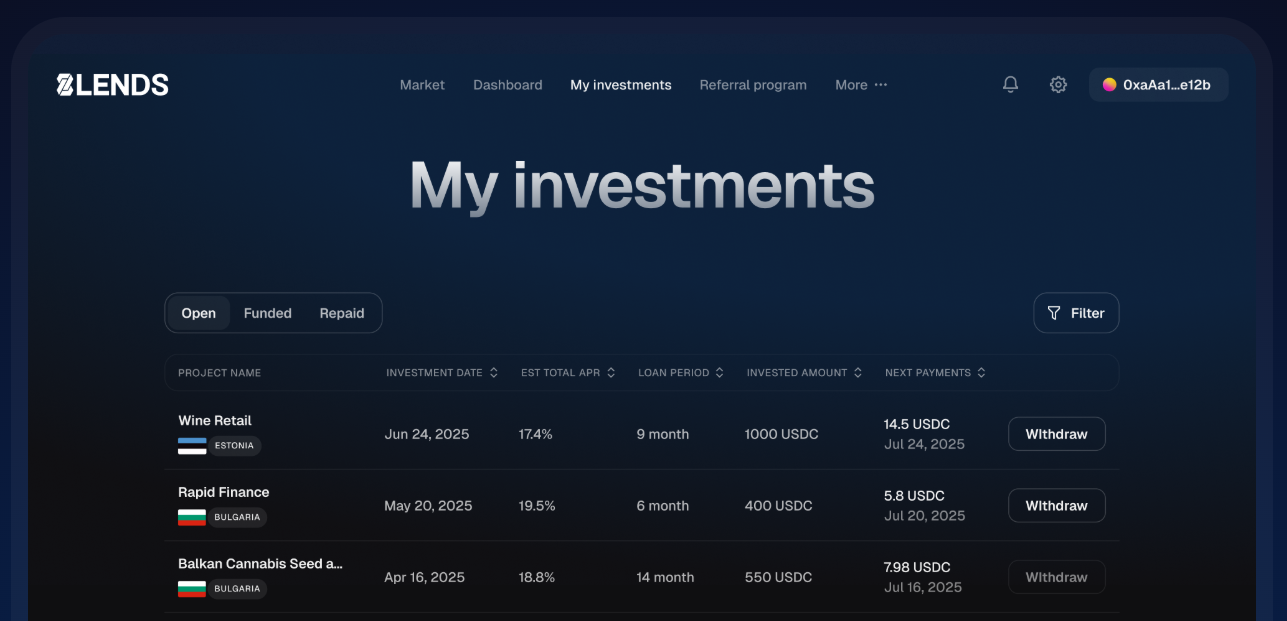

Crowdlending

In the fast-moving world of crypto accounting, organization and clear documentation can make the difference between a smooth tax season and a stressful audit. If you’re looking to simplify how you track returns, funding sources, and digital-asset activity, especially across multiple platforms, you may want a smarter system to manage it all.

Platforms like 8lends offer automated tracking, lending tools, and wallet-level clarity so you always know where you stand financially. Smooth reporting starts with clean data — and systems like this can give you a real edge.

Business Deductions

That’s not to say by any means that deductions only belong in Box 3. Business deductions also help professionals and dedicated crypto freelancers reduce their levy obligation as well. These are everyday expenses like:

- office rent, supplies, and utilities

- inventory purchased

- website development

- hosting and domain expenses

Specifically crypto-oriented ventures

Active traders, miners, staking operators, arbitrage participants, or people running automated strategies include costs directly tied to earning crypto income. Trading fees and exchange commissions are a clear example: if you're executing high-volume transactions to generate profit, those fees count as operational expenses rather than incidental investment costs.

The same logic applies to software subscriptions, trading bots, algorithmic systems, premium analysis platforms, and VPS hosting used for automated strategies. Equipment expenses can also be eligible when they are used exclusively for crypto activity, what that’s servers, high-performance computers, or mining rigs. And these can be depreciated over their useful life rather than deducted all at once.

Liquidity providers on decentralized platforms may also incur fees or costs, such as gas fees for Ethereum-based pools, or platform subscription costs for tracking and analytics.

Professional Services

On top of that, if you hire an accountant familiar with crypto or a tax attorney for compliance consultation, those can be written off as well.

Financing

So can interest you pay on your loans used to finance your crypto activity, including margin trading or borrowed capital for yield-generating strategies.

The key, however, is proof of intent. It must be documented to show that this was spent for the sake of your business, not just casually.

Tax on Crypto Profit: 2 Paths

You have two options for determining what you owe under the wealth tax, a.k.a. the Box 3 taxes in your crypto declaration.

Presumed return method

Suppose an investor holds €40,000 in savings and €20,000 in cryptocurrency, with €10,000 in outstanding debts. First, calculate a fixed gain for each asset class. Savings are multiplied by 0.92%, resulting in €368, and crypto by 6.17%, giving €1,234. Adding these produces a total preliminary gain of €1,602. Next, you reduce this by 2.61% of debts, which is €261, leaving a taxable sum of €1,341. Subtract the standard deduction of €57,000 if applicable, and then multiply the remaining amount by the Box 3 tax rate of 32% to determine the tax owed.

Actual gains method

Total your real-world profits and losses for the year. If the savings earned €100 in interest and the crypto actually appreciated by €500, the total actual gain is €600. Subtract 2.61% of debts (€261) to adjust, resulting in €339, which is then taxed at 32%, yielding roughly €108 in liability. This approach reflects the true performance of assets rather than a fixed presumption.

Exempt When You Calculate Tax on Crypto

There also remain operations in crypto tax 2025 you can execute free of Belastingdienst charges. One is if you decided to give crypto for nothing in return as a gift. If you give up to 3,244 euros, there’s no tax, or if you give that to your parents or your children – 6,604 euros. As for charity, you can give a donation tax-free if it’s worth between 1-10% of your net worth.

Then there are NFTs. If you buy this because you appreciate it as a work of art and aren’t continually reselling NFTs, you won’t be charged this on your tax form. It’s all about what the tax office considers to be your intent.

Records for Tax on Crypto 2025

Whether you fall under Box 1 or Box 3, meticulous record-keeping is essential to ensure that any deductions you claim are accepted in your crypto declaration. For professional or business-level crypto activity in Box 1, this means maintaining transaction logs, receipts for hardware and software, invoices for professional services, and records of interest or loans used for trading purposes.

Every expense claimed should be directly linked to income-generating activity and backed by verifiable documentation. Even for passive investors in Box 3, keeping a clear record of your assets, debts, and any donations is critical. Crypto wallets, exchange statements, screenshots, and even blockchain transaction IDs can serve as proof of holdings, gains, and transfers.

For debt deductions, maintain official loan statements or repayment schedules to substantiate the 2.61% reduction. Good record-keeping not only protects you during audits but also allows you to take full advantage of legitimate deductions, whether for business expenses, debt adjustments, or charitable contributions.

Don’t Overdo Signal Red Flags When You Pay Tax on Crypto

Saving on crypto profit tax and being resourceful about deductions works well in your favor, but it also can attract the wrong kind of attention if you goof. The Belastingdienst monitors for patterns that suggest misclassification of activity, inflated expenses, or omitted income. Always be sure to separate professional trading from personal investing, that any expenses claimed are directly linked to income generation, and document everything thoroughly.

Be mindful of the distinction between Box 1 and Box 3: claiming business deductions while your activity is considered passive can trigger audits or penalties. Similarly, attempting to deduct personal costs as business expenses or neglecting the 2.61% debt adjustment in Box 3 can draw attention.

Another key point is timely and accurate reporting. File your tax return by the May 1st deadline or request an extension in advance if needed. Voluntary disclosure of previously unreported income or corrections to deductions is looked upon favorably and can mitigate fines.

Conclusion

Crypto taxation in the Netherlands has evolved into a detailed and closely monitored system, but investors still have legitimate ways to reduce what they owe — whether through debt deductions in Box 3, business-related expenses in Box 1, or charitable and gifting allowances. The rules may feel restrictive, yet they still reward organized and compliant investors who track their activity properly.

As reporting requirements tighten and regulations like DAC8 increase transparency, staying structured and keeping clean records is no longer optional. The simplest way to protect yourself — and avoid missing deductions — is to use tools that help you document lending activity, interest earned, and crypto flows throughout the year.