Por qué los listados de prestatarios merecen toda su atención

Prácticamente puede entender las finanzas de una persona consultando sus listas de prestatarios. Esto refleja su deseo y confiabilidad; por lo tanto, te ayuda a evaluar el riesgo en las plataformas de préstamos entre pares, financiación privada o financiación colectiva.

Es fundamental preguntar si el prestatario puede devolver lo que quiere. Si el anuncio no lo deja claro, es hora de analizarlo más detenidamente. Un solo error podría costarte dinero, pero una revisión diligente podría generar una asociación rentable y confiable.

Las 5 C del crédito

Las «5 C del crédito» son un conjunto de criterios que los prestamistas profesionales suelen utilizar para determinar si un prestatario es digno de confianza.

- Carácter: «¿Puede el prestatario pagar sus deudas?» No siempre puede reunirse con ellos en persona, pero puede consultar su historial crediticio, historial de pagos e historial laboral. No debes confiarle tu dinero a alguien si tiene un historial de pagos atrasados, problemas legales o malas críticas. Mientras tanto, una persona con un historial limpio parece confiable.

- Capacidad: «¿Pueden pagar el préstamo?» Debe conocer sus ingresos, deudas y flujo de caja para tomar una decisión informada. Si alguien tiene poco dinero, puede tener problemas aunque tenga buenas intenciones.

- Capital: «¿Qué tiene ya el prestatario?» Pueden ser ahorros, capital en bienes raíces u otros tipos de activos. Las personas que piden dinero prestado para invertir en un proyecto suelen estar más comprometidas y preparadas para afrontar los desafíos.

- Garantías: Este es el activo que respalda el préstamo, como una propiedad o un equipo. Si algo sale mal, la garantía puede ayudar. La inversión suele ser más segura si la garantía es más sólida y fácil de verificar.

- Por último, Considera: las condiciones del préstamo y el estado de la economía o el mercado. Incluso un prestatario excelente puede tener problemas en un mercado débil. Además, las condiciones ambiguas de los préstamos o las metas poco claras pueden ser señales de problemas más importantes en el futuro.

Detectar las señales de alerta antes de que le cuesten

Las publicaciones de los prestatarios a veces tienen señales rojas que no siempre son obvias, pero por lo general son suficientes para evitar malas ofertas. Uno de los principales síntomas de los problemas es tener registros financieros desordenados o inadecuados. Si las cifras no cuadran o faltan documentos esenciales, es posible que el prestatario esté desorganizado u oculte algo.

Si una empresa o una persona gana menos dinero, es razonable averiguar por qué y si esa tendencia continuará. También puede ser un problema si un prestatario depende demasiado de un cliente o fuente de ingresos. Si esa conexión se interrumpe, es posible que no puedan pagar el dinero que deben.

Proyecciones poco realistas

Si un anuncio promete grandes beneficios sin riesgo o muestra un futuro prometedor demasiado bueno para ser verdad, confía en tu instinto. Cuando se trata de sus planes, los prestatarios confiables suelen ser honestos acerca de los problemas a los que podrían enfrentarse.

Actividad sospechosa

Toma pistas de cómo actúan las personas. Si un prestatario parece tener prisa por terminar un contrato, no responde a las preguntas con claridad o espera demasiado para entregar documentos importantes, es posible que esté intentando evitar el escrutinio. Si un prestatario nunca ha trabajado en el campo para el que está pidiendo un préstamo, como un inversor inmobiliario que invierte por primera vez y comienza un gran proyecto de reparación y cambio, también es algo en lo que hay que pensar.

Otro conjunto de señales de advertencia incluye los problemas con la ley y la forma en que funcionan las cosas. Las demandas pendientes, las licencias vencidas o las prácticas comerciales extrañas pueden indicar que una empresa es inestable o que tendrá problemas en el futuro. Y cuando consultes los anuncios de bienes raíces, ten cuidado con la información poco clara sobre la propiedad, los conflictos de zonificación o las casas con problemas estructurales que no se hayan solucionado.

En algunas circunstancias extremas, los anuncios pueden ser falsos. Algunas señales de fraude son los precios demasiado altos de las propiedades, el papeleo que no coincide o los historiales laborales incompletos. Si el prestatario no confirma la información básica ni proporciona una identificación, aléjese, sin importar lo buena que parezca la transacción.

Contrarrestar

Plataformas como 8 préstamos elimine muchos de estos riesgos evaluando a los prestatarios mediante métodos rigurosos basados en datos. Desde acuerdos respaldados por garantías hasta documentación transparente y entrevistas con los prestatarios, 8lends hace que sea más fácil detectar tanto las señales de alerta como las oportunidades prometedoras, sin necesidad de ser un contador forense. Esa es una de las razones por las que los inversores confían en la plataforma para ofrecer opciones de préstamo consistentes y de alto rendimiento sin comisiones de plataforma.

Reconociendo las luces verdes de una cotización sólida

Por el contrario, no todos los anuncios son malas noticias. Algunos prestatarios son decentes, pero revisarlos requiere un poco de esfuerzo. ¿Qué aspecto tiene una buena lista de prestatarios? En primer lugar, los números se suman. Una cotización sólida tendrá una sólida documentación financiera, ingresos estables y un margen suficiente para pagar las cuotas del préstamo con facilidad. Las empresas deben tener ingresos constantes o crecientes, y el prestatario debe tener acceso a ahorros u otras fuentes de dinero.

El comportamiento del prestatario también es crucial. ¿Responden rápidamente? ¿Están dispuestos a responder a las consultas y dar más información? Para generar confianza, es esencial ser abierto y profesional. Un solicitante bien preparado también tendrá una justificación razonable para el préstamo. La meta debe ser justa, estar bien pensada y estar basada en hechos, ya sea para hacer crecer un negocio, comprar una casa o saldar una deuda. Deberías poder ver cómo encaja el préstamo en su plan general y cómo esperan devolverlo.

Además, compruebe si su entorno es estable. ¿Están haciendo negocios en un mercado saludable? ¿Tienen un buen equipo trabajando para ellos? ¿Están sus activos asegurados, documentados y tasados correctamente? Todas estas cosas aumentan las probabilidades de que su inversión se mantenga en el buen camino.

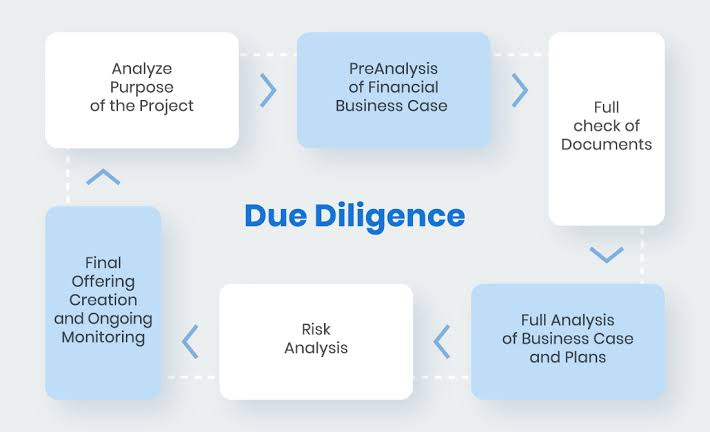

Cómo hacer la debida diligencia

Es hora de poner en práctica todo lo que ha aprendido ahora que sabe qué buscar y qué evitar. Lo que diferencia a los inversores inteligentes de los afortunados es que investigan.

Para empezar, revise cuidadosamente los documentos financieros del prestatario. Revisa sus registros tributarios, sus informes de ingresos, sus estados de cuenta bancarios y cualquier presupuesto o estimación de proyecto que te den. No tengas miedo de hacer más preguntas si algo no tiene sentido. También debes comprobar su historial crediticio, incluidos los préstamos personales. Con frecuencia, puedes comprobar el crédito de una empresa a través de vendedores, proveedores o servicios de informes crediticios.

También es esencial comprobar los ingresos de una persona. Busca talones de pago, contratos firmados o pruebas concretas que respalden sus afirmaciones. Si tienen una garantía, pídele a un tercero acreditado que la revise. No se limite a creer lo que dice el prestatario; asegúrese de que el activo sea absoluto, justificado y legal.

También puede ser beneficioso realizar una inspección de la propiedad o el proyecto. Una visita al sitio puede darte mucho más que las imágenes o los anuncios si estás haciendo un préstamo para la compra de un inmueble.

Por último, analice el pasado del prestatario. Revisa las reseñas, pide referencias y busca en las bases de datos legales los litigios en curso o los problemas del pasado.

Conclusión

Cada anuncio tiene algún riesgo. Pero puedes gestionar el riesgo con las herramientas, las preguntas y la actitud correctas. No necesita adivinar a ciegas; puede aprender de las situaciones con claridad, confianza y calma.

¿Quiere una plataforma de préstamos que respete su diligencia y la recompense? 8lends te da acceso a préstamos empresariales de alto rendimiento y con un control exhaustivo, sin comisiones ocultas, promesas exageradas ni papeleo impreciso.