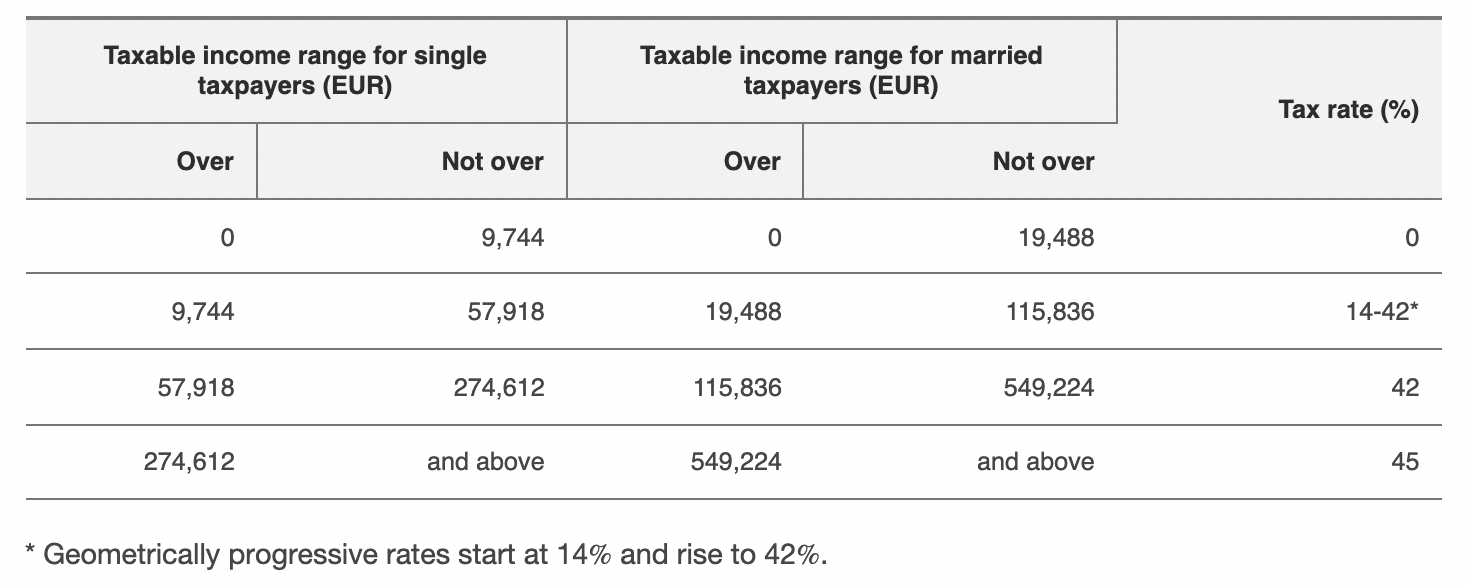

The Cornerstone: Master the One-Year Hold (§23 EStG)

HODLing is your best weapon and the cornerstone of effective planning.

The Plan

Hold for over 365 days. Once that period has passed, profits on its sale entail no duties for privatvermögen, independent traders. This is the central provision under §23 EStG.

Why it Works

Legislation distinguishes among quick speculation, who pay up, and long-term private sales who don’t pay duties.

The holding period works on a per-unit/lot tracking system where each purchase starts its own clock. Use portfolio tracking software to know when specific lots become tax-free.

The Active Trader's Shield: Know the Two Different Allowances (and Use Them)

There are two different, commonly confused allowances; once you know which one applies to what, you’ll stop leaving easy savings on the table.

Freigrenze for Private Sales (§23 EStG)

For sales to private persons (crypto sold in less than one year), Germany has a Freigrenze (threshold level) of €1,000 per calendar year for each person as of the 2024/2025 reforms.

If your total brief wins off private yearly sales are under €1,000, there’s no tax. Above it – there are. This Freigrenze used to be €600 and is now higher under recent legislation.

Sparer-Pauschbetrag (Capital Income)

Otherwise, capital income (Kapitalerträge) rules utilize the Sparer-Pauschbetrag, €1,000 single / €2,000 married (starting in 2023). It is used for traditional capital income and kicks in if crypto is treated as capital income in some cases (or if dealing with banks/brokers that have Abgeltungsteuer regulations imposed on them).

Why it Works

Apply the correct allowance for the correct occasion; the Freigrenze is the applicable guideline for normal short-term crypto private-sales; the Sparer-Pauschbetrag will pay capital off takings.

Run a year-end review in November/December. If you're below the Freigrenze and you'd like to realise a little short-term profit, you can harvest that unused exemption, but be careful: once you cross the Freigrenze, the whole amount becomes taxable.

The Portfolio Optimizer: Smart Loss Harvesting (Verlustverrechnung)

Realise losses on underperforming positions to offset gains realised in the same tax year. Losses from private sales are one of, if not the best, ways to offset gains from other private sales transactions subject to the rules of §23 EStG.

How it Works

It limits your net taxable short-term gains before the Freigrenze or personal tax rate is applicable.

Example

€4,000 gains − €1,500 realised losses = €2,500 net gain, then apply the €1,000 Freigrenze/other allowances as relevant.

Remain tactical, not emotional: sell losers to offset winners, then consider re-buying if still bullish on the asset (but monitor transaction fees and wash-sale timing issues).

The Long Game: Staking, Lending & "Other Income"

The Reality (2025 BMF Guidance)

Rewards received from staking, lending, mining, airdrops, etc., are generally taxable as "other income" (§22 No. 3 EStG) as you receive them. Upon receiving these rewards, you must report them in their present euro market value.

Later sales of those received rewards then fall under the regular private sale rules (e.g., 1-year holding rule) for subsequent disposals. The 2025 update and the 2022 official guideline confirm the 1-year plan, but a blanket 10-year extension does not exist for private investors.

Minor Exception

Of the type covered in §22 No. 3 (not staking/mining/lending, etc.) is subject to a small yearly exemption (Freigrenze) of €256. If your occasional income under §22 No.3 is ≤ €256 in the calendar year, you don't have to declare it. If more than €256, all of it is taxable.

Store any staking/lending rewards you intend to long-hold in a separate wallet and record the euro value when you receive them. That price is the tax base applied to the income; future sales will use that purchase price for holding-period calculations.

The Organizer's Edge: Strategic Wallet Segregation & Lot-Level Monitoring

Your portfolio's not one giant pot for the taxman. Organization saves taxes and trouble.

The Strategy

Have distinct wallets (or exchange accounts) for distinct strategies: long-term HODL, day-trading, and staking/lending rewards.

Since tax regulations function per unit/lot and per buy time, and since exchanges' timestamps dictate holding durations for exchange trades, compartmentalizing strategies avoids older tax-free lots from being "eaten" by day-trades or platform accounting.

The BMF guidance encourages unit-by-unit tracking and dictates that the order of use is determined unit-by-unit; where not practicable, rules determine which units are considered sold.

- The "Long-Term HODL" Wallet: deposit and leave for >365 days.

- The "Active Trading" Wallet: short-term trades and tests.

- The "Rewards/Income" Wallet: receipts from staking/mining/lending (track EUR value on receipt).

Precision in record-keeping and compliance separates investors who react from those who plan. 8lends helps organizations manage complex reporting, audit, and governance requirements with the same discipline that successful crypto investors apply to their portfolios. Its GRC solutions bring structure, traceability, and regulatory confidence to every financial process – from digital asset tracking to enterprise-level compliance.

The Compliance Protection: Foreign Reporting & AWV (Not §138 AO with €15k)

Compliance protection is risk management, not tax avoidance. The old €15,000 claim is misleading and unsafe to rely on.

What is New

Germany foreign-payments/holdings reporting (AWV regulations to the Deutsche Bundesbank) and corresponding thresholds were updated effective 1 January 2025. The new regulations raised the standard reporting threshold for incoming/outgoing payments from €12,500 to €50,000; they also modified other asset-balance thresholds.

Reporting and fines continue for large transfers and unreported holdings. If you make foreign exchanges (or large cross-border transfers), you will need to be aware of AWV reporting and tax cooperation/declaring obligations. This is separate from criminal tax evasion laws; reporting is statistical/regulatory and can involve fines of up to tens of thousands in some cases.

In larger, long-term investments where regulatory clarity is a priority, use regulated German trading platforms or custodians (regulated EU/German platforms) to enable fiat rails and ease of reporting, but remember: the tax rules themselves (1-year holding, staking income treatment) are under statutory direction regardless of platform.

Your Most Crucial Tactic: Unbreakable Documentation (Ten-Year Habit)

It all depends on iron-clad record-keeping. The BMF guidance expressly requires closer documentation and retention rules.

Tools

Use reputable crypto tax software that pulls in exchange histories, chain information (if available), and calculates lot-level holding periods.

Save exchange statements, balance snapshots, wallet addresses, CSV exports, and the valuation of the euro at the time of each taxable event. The BMF circular and the practice of taxation require detailed transaction summaries and tax reports.

Remember the golden rule too: keep transaction records and annual tax reports for at least 10 years, the period used by German tax retention guidelines for these kinds of assets and BMF rules.

Conclusion

Cutting your crypto taxes in Germany is a testament to your maturity as a strategy creator. It's the final, crucial step in empowering yourself from the passive investor to the shrewd portfolio manager.

By these six legal moves of virtue, virtue of patience (one-year rule), effective use of allowances (Freigrenze vs Sparer-Pauschbetrag), smart loss harvesting, effective staking/lending income management, conscious wallet structuring, and following foreign-reporting rules religiously, you can build your wealth on a pillar of certainty.

German tax law rewards strategy, not luck — and structure is the difference. 8lends builds governance and compliance systems that help financial institutions, fintechs, and digital-asset players stay ahead of evolving regulation while keeping control of every detail.