What Determines Income vs Capital Treatment Under Irish Crypto Tax Rules

Beyond actively earned income, which is universally going to be collected as ordinary income regardless, crypto Revenue looks at the nature of your activity to determine whether rises are charged state obligation as income or capital.

Revenue generally considers the following.

Intention and Purpose

If you acquire virtual currency with the intention of holding it as an investment and profiting from long-term appreciation, it is more likely to be treated as a capital asset, or, in other words, be taxed at the flat 33% capital gains rate. CAT features the same rate, if you are sending digital assets as a gift or giving them up for inheritance.

Organisation and Commerciality

It’s important on your Form 11 whether transactions are organised, structured, and conducted professionally. If you run a platform, provide crypto-related services, or actively manage multiple investments in a coordinated way, your digital currency appreciations will be deemed trading income rather than rising-value assets.

Nature of Rewards or Compensation

Digital money received as a reward, payment for services, or yield from protocols such as staking, lending, or liquidity provision is generally treated as income. The date of receipt and fair market value in euros at that time are critical for calculating relevant amounts. Later disposal may trigger a second layer of asset appreciation debt if the asset has appreciated further.

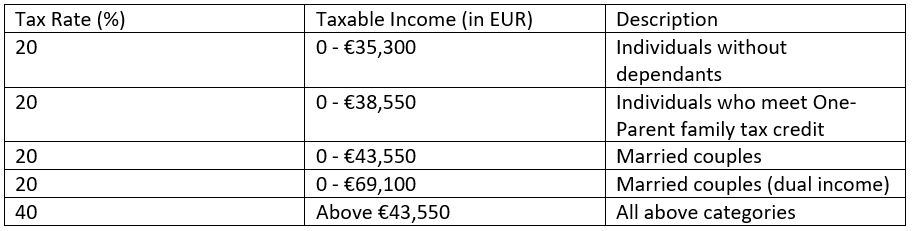

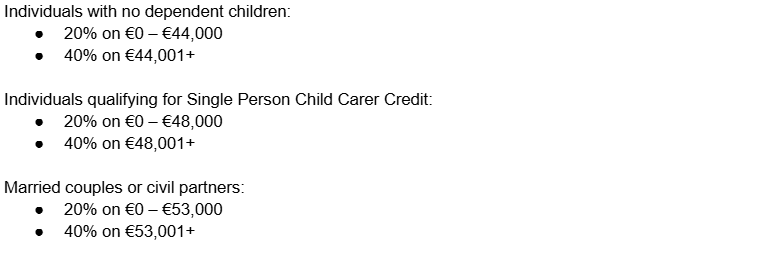

Income Tax Rates

For digital cash, the applicable income rates depend on your total annual earnings and personal circumstances:

Crypto Under Capital Gains Tax

When crypto Revenue classifies virtual currency activity as passive investment, or when you dispose of digital coins priorly obtained as income, CGT comes into play for a flat 33%.

What counts as a disposal:

- Selling virtual cash for euros

- Swapping one virtual currency for another

- Use virtual cash to buy goods or services

- You give up virtual coins in a fork

Each of these events may trigger capital gains tax on crypto, provided the disposal results in a net rise.

Calculate CGT as follows:

- Determine the acquisition cost in euros as of the precise date you acquired that virtual cash.

- Calculate euro value at the time of disposal.

- Subtract the acquisition cost from the disposal value to find the increase.

- Apply associated fees and allowable losses from other disposals to reduce the net increase.

In Ireland, the first €1,270 is exempt from. Only beyond that does the 33% flat rate kick in.

The following do NOT trigger debt to Revenue:

- Moving virtual cash between your wallets

- When the coin type sitting in your wallet rises in value, but you have not yet sold it

- You buy virtual cash with euros or another fiat

- Holding digital cash long term

DeFi, Crowdlending, and Income vs. Capital Classification

Most DeFi protocols involve liquidity pools, whether for decentralized exchanges, lending, or staking platforms. Fiscal treatment depends on the type of transaction:

- Swapping tokens or selling LP tokens triggers capital gains tax on crypto if the value has increased.

- New token rewards are deemed as new income, with fiscal debt calculated based on market value in euros.

- NFTs are regarded as the same as virtual money.

Crowdlending and Structured Returns

Crowdlending platforms, such as 8lends, offer a slightly different approach. Here, you contribute to loans pooled with other investors, spreading risk while earning interest-like returns. These returns are generally treated closer to income rather than capital gains because they resemble interest payments rather than speculative appreciations.

Benefits of crowdlending through platforms like 8lends include:

- Risk diversification by participating in multiple loans rather than relying on a single borrower

- Sophisticated credit scoring models for projects that might not qualify for traditional bank financing

- Predictable, potentially lucrative returns that can be easier to plan for from a tax perspective

- Loans are backed by collateral.

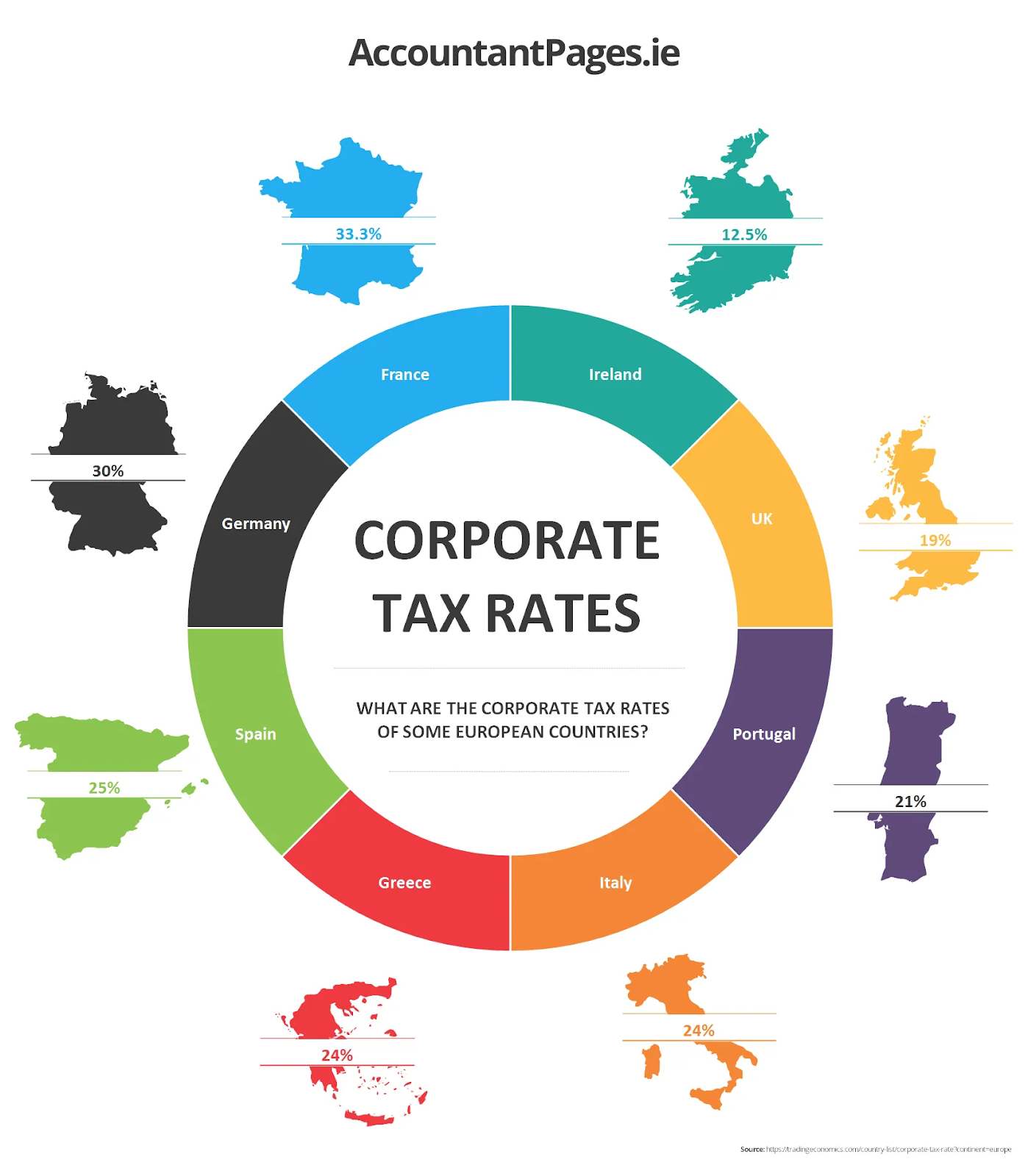

Corporation Tax in Ireland

If you are not quite fond of the income brackets in Ireland and you clearly recognize yourself as a business, there is another option you can go for. Corporation tax is applied to the profits a company earns during its accounting period. There are two main rates depending on the type of income:

If the rate changes partway through the company’s accounting period, profits are prorated over time, and each portion is charged according to the rate in effect during that part of the period. This ensures that all income is levied accurately, even if rates fluctuate during the year. For companies not incorporated in Ireland, residency is determined by a control test as well as a central management and control test.

Eligible Write-Offs for Tax on Crypto

These reduce debt burden in crypto tax returns:

- Purchase of goods or inventory for resale

- Utilities

- Machinery

- Lease payments

- Professional fees

- Loan financing

Also, some pre-trading expenses, such as preparing corporate plans before starting operations, may also be deductible. Only the net amount excluding VAT should be claimed. If expenditures are used for both personal and business purposes, like phone bills, motor costs, or rent, you can only claim the proportion specific to revenue creation.

VAT Considerations

VAT applies when a digital currency business is selling goods or providing services in exchange for payment. If a business takes cryptocurrency as payment for wares or digital products, the transaction is handled as a typical euro sale.

Revenue treats it as a means of exchange, without VAT, rather than a standard good or service. However, VAT may apply to any fees charged for facilitating trades or converting digital cash into fiat. For businesses registered for VAT, it is crucial to exclude VAT amounts from expenses claimed against profits.

Conclusion

By distinguishing between actively earned income, trading activity, and passive investment gains, you can better plan transactions, optimise your tax position, and avoid unexpected liabilities. For businesses, leveraging corporation rules, capital allowances, and deductible expenses can further reduce obligation, while VAT considerations must be managed carefully to remain compliant.

For investors seeking structured, lower-risk opportunities within the virtual currency ecosystem, 8lends’ crowdlending offers an attractive alternative. By pooling funds with other investors to finance vetted projects, you can enjoy risk diversification, predictable interest-like returns, and access to projects that traditional banks might overlook.