At-a-glance: Austria vs. Germany comparison

Austria and Germany apply two fundamentally different philosophies to crypto. Austria treats crypto income like other capital income — a single flat rate, simple to calculate, and broadly the same for everyone. Germany treats most crypto as private speculation — heavily taxed in the short term, completely tax-free after 12 months. The headline differences sit in the table below; every row is unpacked in the sections that follow.

Headline tax rates: flat 27.5% vs progressive 0–45%

Since the 2022 Eco-Social Tax Reform, Austria taxes virtually all crypto disposals at a single special rate of 27.5%, the same Sondersteuersatz that applies to dividends and listed-share gains. The rate does not depend on how much the investor earns elsewhere, how long the assets were held, or whether the activity is occasional or systematic. The Austrian Federal Ministry of Finance (BMF) sets out the framework on its tax-treatment-of-crypto-assets page, and individual investors file via the FinanzOnline E1kv form.

Germany has no special crypto rate. Crypto is taxed as either "other income" (§ 22 EStG, for staking and similar yield) or "private sales" (§ 23 EStG, for capital gains). Both flow into the investor's general income-tax bracket. Bracket rates run from 0% on the basic allowance through 14%, 24%, 42% and a top marginal of 45%. Solidarity surcharge and church tax may apply on top.

How Austria and Germany compare across Europe

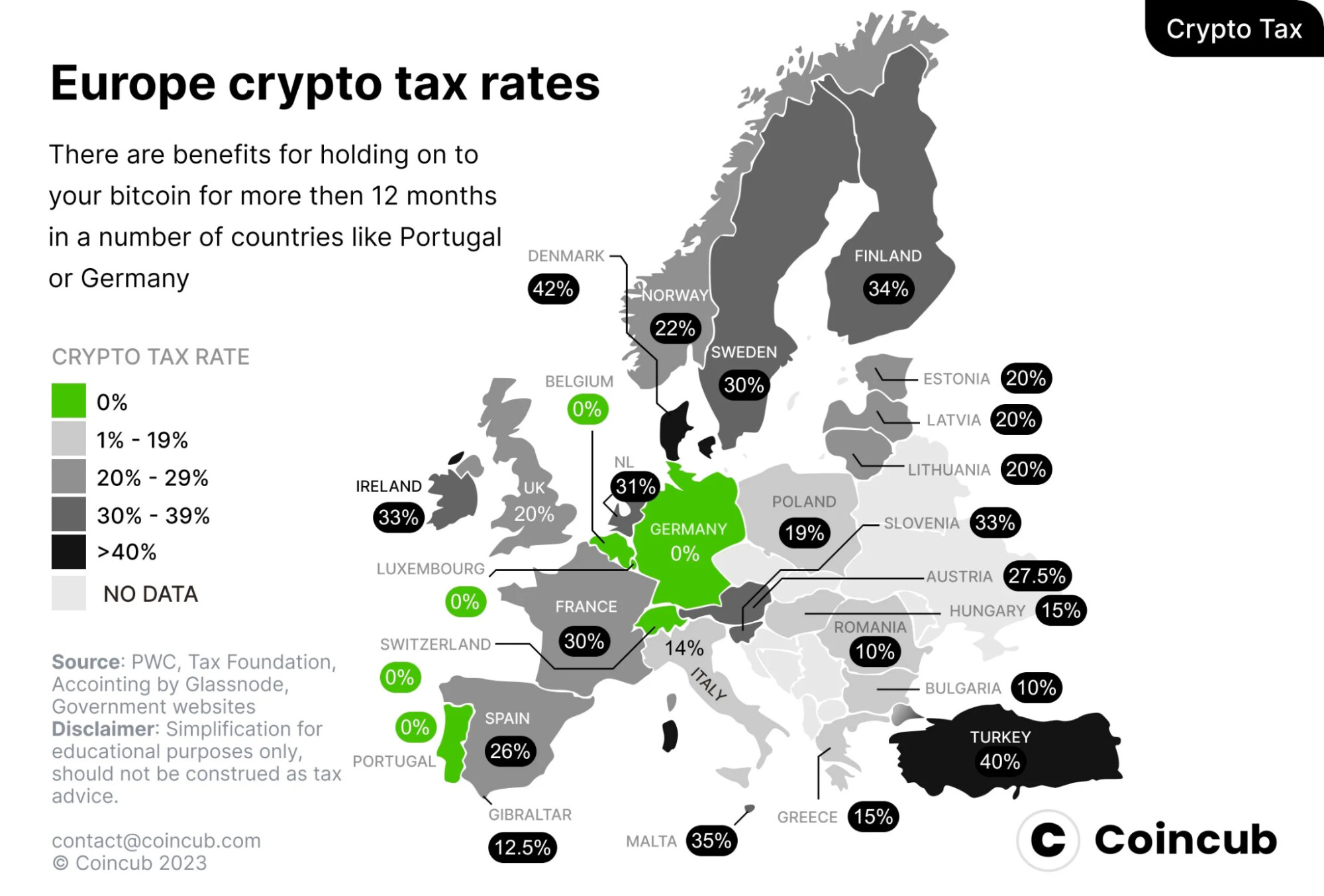

In the broader European landscape, Austria's 27.5% flat rate sits in the middle of the pack. Germany scores 0% on long-held crypto, but its short-term rate is among the highest in Europe — Coincub data places effective German rates close to Spain's and Sweden's when the 1-year exemption is missed. Portugal (0% on personal long-held crypto) and Switzerland (0% on private capital gains) remain the standout exceptions; full-tax jurisdictions like Denmark (up to 42%), Finland (34%) and Ireland (33%) sit at the other end.

For dual-citizenship holders or remote workers with flexibility over tax residency, the comparison matters in two scenarios: an active trader maximising annual realised gains, and a long-horizon investor accumulating Bitcoin or Ether through dollar-cost averaging. The first is taxed less in Austria; the second is taxed less — usually not at all — in Germany.

The 1-year HODL exemption — and Austria's "old tokens" rule

Germany's most distinctive feature is the 12-month holding rule under § 23 EStG: private cryptocurrency sales are entirely tax-free if the asset was held for more than 365 days before disposal. The rule survived a 2023 Federal Fiscal Court (Bundesfinanzhof) challenge and remains in force in 2026. Within the 12-month window, gains are taxable at the personal income-tax rate, with a €1,000 freigrenze (raised from €600 in 2024) below which no tax is owed.

Austria abolished the equivalent 1-year exemption for cryptocurrencies on 1 March 2022. The reform introduced two categories:

This bifurcation matters when calculating cost basis. An Austrian investor who began stacking Bitcoin in 2018 can sell those specific units today with no tax liability, while coins of the same ticker bought in 2022 are taxed in full. Most Austrian tax software treats old and new tokens as separate inventory pools — mixing them creates audit risk.

What is taxable in each country

The single biggest divergence is the treatment of crypto-to-crypto swaps. Austria explicitly does not recognise a swap as a realisation event: tax is triggered only when crypto is exchanged for fiat or used to pay for goods and services. Germany treats every swap as a disposal of the outgoing asset and an acquisition of the incoming asset, valued in euros at the moment of the trade.

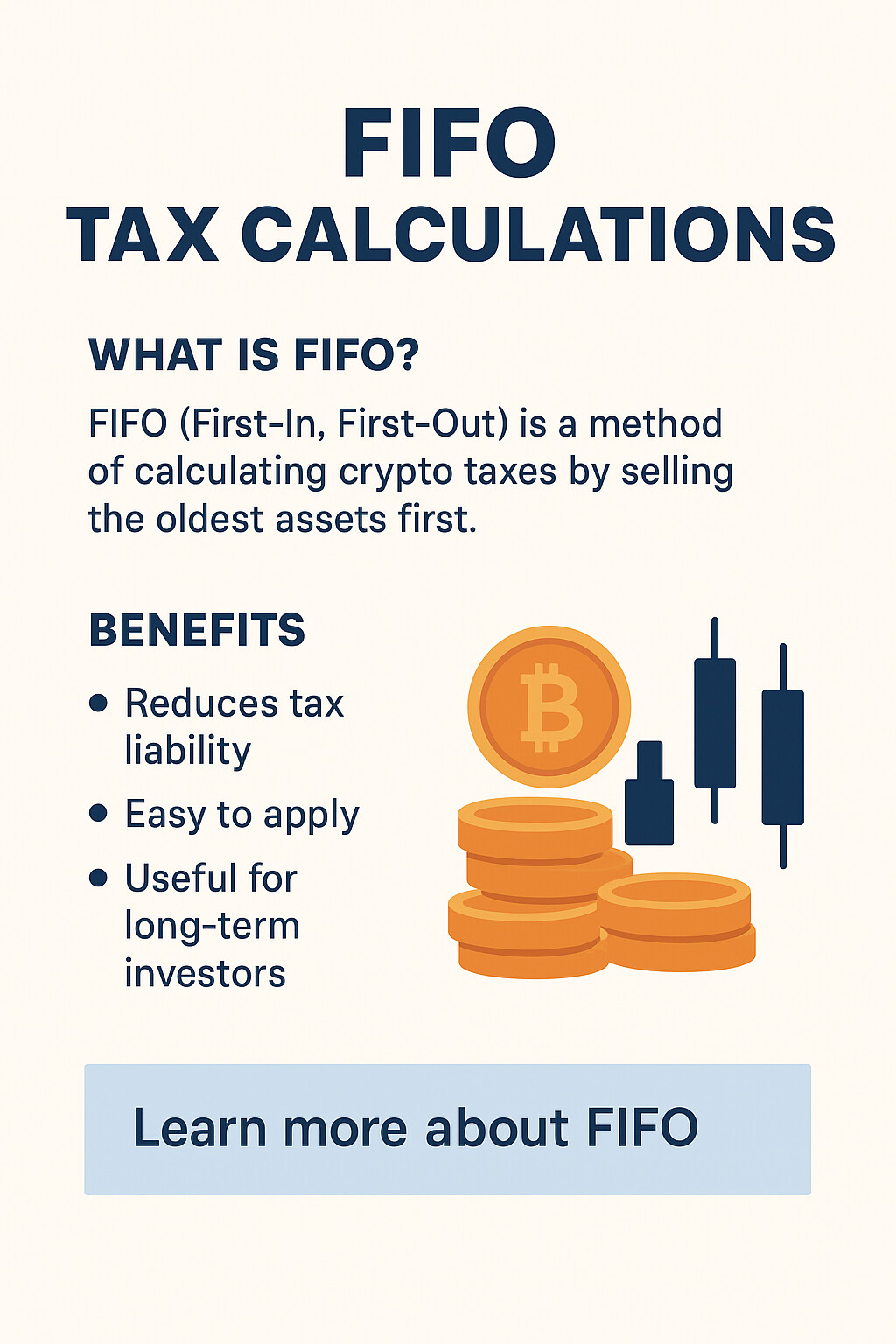

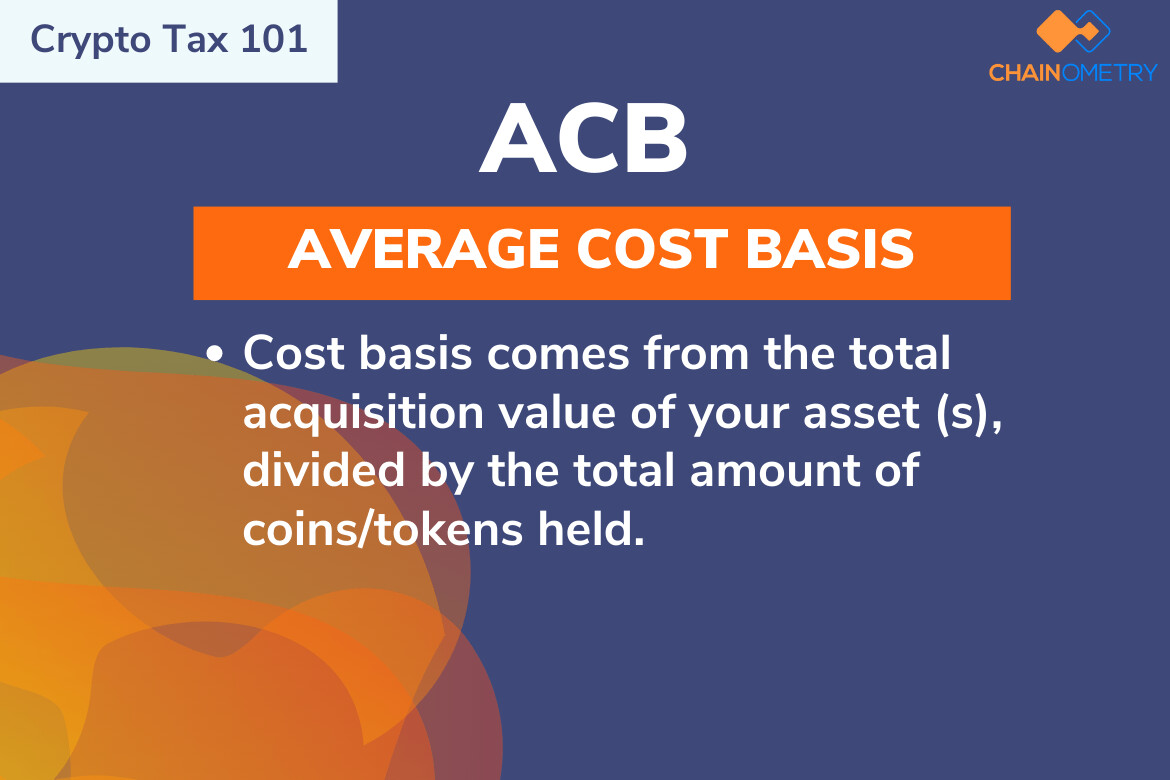

Cost basis methods: FIFO (Germany) vs moving average (Austria)

Cost basis is the rule that decides which "lot" of crypto an investor is deemed to have sold when disposing of part of a holding. The choice of method can change the calculated gain by tens of percent in volatile markets, so the rule matters in practice.

Germany uses FIFO (first-in, first-out) per wallet by default. The earliest coins acquired are deemed sold first. For an investor whose first purchase was the cheapest, FIFO maximises taxable gain — but it also makes the 12-month exemption easier to claim, because the oldest coins (which clear the 365-day threshold first) are also the first to be sold. LIFO (last-in, first-out) is permitted in narrow cases but rarely beneficial.

Austria uses the moving-average cost method (Gleitender Durchschnittspreis) for "new tokens" held in the same wallet. Every fresh acquisition recalculates the weighted-average cost per unit; every disposal uses that running average. The method removes the FIFO/LIFO selection problem and smooths reported gains during volatile periods.

Both methods require complete, timestamped transaction records. Austrian investors must additionally segregate "old tokens" from "new tokens" — the moving average applies only to the post-Feb 2021 pool.

Mining, staking, DeFi and airdrops

The flat-vs-progressive divide reverses for many income-style crypto activities. Austria's 27.5% applies once, at the moment of profitable disposal. Germany taxes these flows twice in many cases — first as ordinary income at receipt, then again as a private sale if disposed of within 12 months.

For yield-farming and staking, this means a German investor active in DeFi must value every reward at its euro market price on the second it lands in the wallet — a record-keeping burden that quickly becomes unmanageable without crypto tax software. Austrian DeFi investors only need to track disposal events.

NFTs — when they are not "crypto"

Austria does not classify NFTs as cryptocurrency. Under § 27b EStG, only fungible crypto-assets that function as a medium of exchange or store of value qualify for the 27.5% rate. NFTs are treated as private speculation income under § 31 EStG: tax-free if held more than one year, and taxable at the investor's progressive marginal rate (up to 55%) if sold within 365 days.

Germany applies § 23 EStG uniformly. NFTs are subject to the same 12-month rule as Bitcoin: held longer than a year, the disposal is tax-free; held shorter, the gain is taxed at the personal income-tax rate. The €1,000 freigrenze applies.

Loss offsetting and gifting

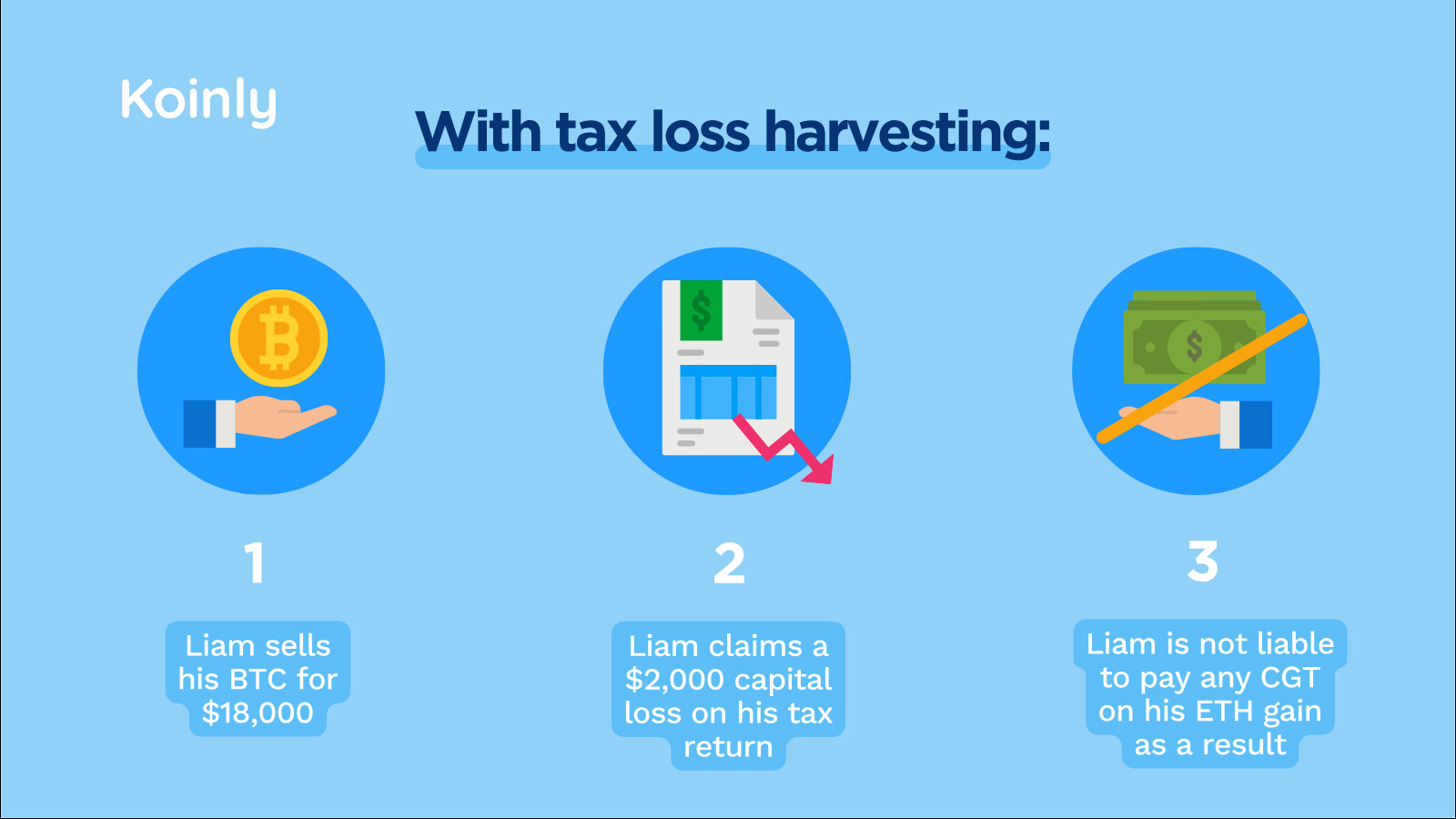

Austria allows losses on one capital asset to offset gains on another in the same calendar year — crypto losses can wipe out gains on listed shares, ETFs or other Sondersteuersatz instruments. Unused losses cannot be carried forward and expire at year-end. Germany ring-fences crypto losses inside § 23: they can offset other private-sale gains (within or across years) but cannot be set against employment income, dividends, or staking income. Carry-forward is indefinite — but only useful if other § 23 gains arise in future years.

Both jurisdictions allow transaction fees, gas costs and platform commissions to be deducted from the disposal value. Both require the deduction to be evidenced by exchange statements or on-chain proof.

How are crypto gifts and inheritance taxed?

Austria abolished its gift and inheritance tax in 2008. Crypto gifts and bequests are unlimited and tax-free, though gifts above €15,000 to non-relatives (and €50,000 to relatives) within five years must be declared via the Schenkungsmeldung notification. Germany taxes gifts and inheritances on a sliding scale: a spouse can receive €500,000 tax-free per ten-year period, children €400,000, and unrelated parties only €20,000 — anything above triggers gift tax of 7–50%.

Worked examples for three investor profiles

The same trading behaviour can produce very different tax outcomes depending on residency. The three cases below use realistic 2025 numbers and apply each country's rules straight off the table above.

The active-trader pair (Markus and Anna) shows Austria's flat rate winning by roughly €2,200 on €18,000 of realised gains. The long-term pair (Lukas and Sophie) shows the German exemption saving Lukas €11,825 on the same €43,000 gain that Sophie has to pay in full. The break-even point depends on holding period, swap frequency, and personal income bracket.

Which country is better for whom

There is no single answer — the optimal jurisdiction depends on five variables: holding period, trading frequency, marginal income-tax bracket, the proportion of activity that is income-style (staking, DeFi, mining) versus capital-style (buy-and-sell), and exposure to NFTs.

When is Austria the better tax jurisdiction?

- Active traders making frequent crypto-to-crypto swaps — the swap exemption is a structural advantage worth several percentage points per year

- High-income earners (over ~€90,000 of taxable income) — the 27.5% flat rate beats the 42–45% top brackets

- Investors with diversified capital-asset losses — broader offsetting rules

- Investors who want to gift large amounts of crypto to family members

When does Germany give a better tax outcome?

- Long-term HODLers willing to hold any single position for more than 12 months — the exemption can mean 0% tax on the entire gain

- Low-to-moderate income investors with annual gains below €15,000 — bracket rates can fall under 27.5%

- NFT investors with patience — same 1-year exemption applies

- Investors with small total crypto income — the €1,000 + €256 freigrenzen wipe out small portfolios entirely

For investors who genuinely have a choice — dual citizens, remote workers, founders considering relocation — running both countries' calculations on the same trade history is the only honest test. Both jurisdictions also enforce DAC8 reporting from 2026, so cross-border concealment is not an option.

Crowdlending as a cleaner income profile

One reason DeFi tax is painful in both Austria and Germany is the irregularity of yield. Liquidity-pool fees, validator rewards, lending interest and impermanent-loss adjustments all arrive at unpredictable euro values, often dozens of times per month, and each must be priced and recorded. The structural fix is to swap unstructured DeFi yield for a fixed-rate, time-bounded income stream — the model used by regulated crowdlending platforms.

Predictable on-chain income, in a wrapper your tax accountant understands

8lends is the Web3 expansion of Maclear AG, a Swiss-based P2P crowdlending platform operating under Swiss financial regulations and as a member of PolyReg SRO. Where Maclear funds SME loans in euros through traditional banking, 8lends funds equivalent projects in USDC on the Base blockchain — same diligence, same collateral, faster settlement, full on-chain audit trail.

For tax purposes, that audit trail is the point. Every investment, monthly interest payment and principal return is timestamped on Base and exportable as a CSV. Each interest payment lands at a known rate on a known date — no oracle-dependent fair-value adjustments, no impermanent-loss reconciliation, no nested DeFi position to unwind. Austrian investors report it as § 27b investment income. German investors report it as § 22 income at the moment of receipt, with the disposal of the underlying USDC (a stablecoin pegged 1:1 to USD) producing minimal additional gain.

Each borrower passes 40+ due diligence criteria assessed by Maclear AG, with a 1–10 internal risk score. Loans are collateral-backed, monitored continuously, and supported by Maclear's Provision Fund — a reserve formed from a portion of platform commissions used to cover temporary borrower repayment difficulties.

Crowdlending does not change which country taxes the income — it changes how easily that income can be reported. A fixed-rate USDC loan with monthly distributions yields a clean income line in Austria's E1kv and Germany's Anlage SO; the same euro value chased across three DeFi protocols and two L2s typically requires a paid tax-software subscription just to reconcile.

Conclusion

Austria offers simplicity and a flat 27.5% rate, broader loss offsetting, untaxed crypto-to-crypto swaps, and unlimited tax-free gifting — features that suit active traders, high earners, and investors who recycle capital across many positions. Germany offers a complete tax exemption after 12 months, modest annual freigrenzen, and lower effective rates for low-to-moderate earners — features that reward patience and discourage churn.

The right answer for any individual investor depends on holding period, swap frequency, marginal bracket and the role of staking, DeFi or NFTs in the portfolio. For most active crypto users, the difference between the two regimes is large enough to be worth modelling on a real trade history before making decisions about residency, account structure, or which platform to use for yield.