Denmark crypto tax — at-a-glance

The Danish system is unusual in that it does not have a dedicated capital-gains tax for cryptocurrency. Skattestyrelsen instead routes crypto disposals through one of two existing regimes: most coins are treated as speculation property taxed as personal income, and a smaller class (stablecoins, futures, options, certain DeFi positions) sits under the Kursgevinstloven as financial contracts taxed as capital income. Both regimes use FIFO and require granular per-transaction records.

How SKAT classifies crypto: speculation, not capital gains

Denmark does not treat Bitcoin or Ether as currency, securities, or investment property. Skattestyrelsen treats them as speculation assets (spekulationsaktiver) under the general income provisions of Statsskatteloven § 5, stk. 1, litra a. The legal consequence is that gains are taxed as personal income at full progressive rates, and losses are deducted as a ligningsmæssigt fradrag — a less valuable deduction.

The classification turns on intent. SKAT presumes speculation whenever the buyer's purpose was to profit from price changes. Because virtually every retail Bitcoin or Ether purchase fits that description, the speculation presumption is the default outcome of any audit. The Danish National Bank's 2024 paper Crypto Assets — Risks, Regulation and Usage in Denmark confirms there is no statutory bright-line test; the classification is fact-specific.

A small minority of investors who can demonstrate non-speculative purpose — for example, a long-term holder who genuinely uses Bitcoin as a payment medium and never trades — may avoid the speculation classification and remain untaxed on disposal. In practice this argument almost always fails on audit, and tax advisers in Denmark generally treat all retail crypto as speculation by default.

The Danish income-tax stack — building up to 52.07%

Danish personal income tax is built from four layers: a fixed bottom-bracket state tax (bundskat), a top-bracket state tax (topskat) on income above a threshold, a municipal tax that varies by where the taxpayer lives, and the optional church tax. The total combined rate is capped by the skatteloft — the constitutional tax ceiling — at 52.07% for personal income in 2025.

One quirk works in the crypto investor's favour: the 8% labour-market contribution (AM-bidrag) that applies to wages does not apply to crypto speculation gains. Without that 8% wedge, the effective rate on a top-bracket Danish crypto investor is ~52% rather than the ~56% that applies to wages above the topskat threshold.

Where Denmark sits in Europe

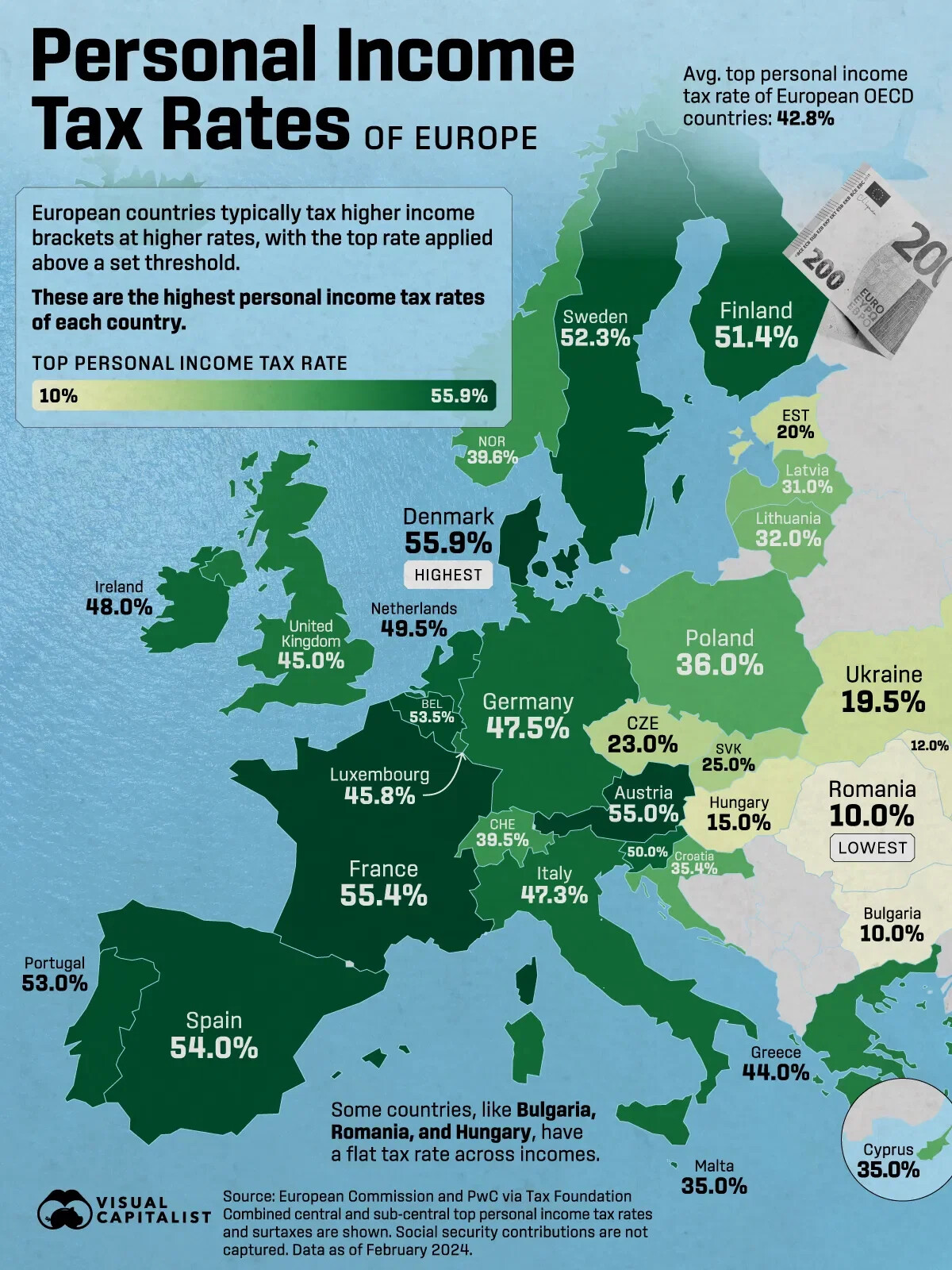

At the personal-income headline rate of 55.9%, Denmark holds the highest top marginal rate of any European OECD country. For crypto specifically, the absence of AM-bidrag drops the effective ceiling to 52.07% — still firmly in the upper quartile, comparable to Sweden (52.3%) and Finland (51.4%) and well above Germany's 47.5% or Austria's 55%. Lower-tax EU jurisdictions like Bulgaria (10%), Romania (10%) and Hungary (15%) sit at the opposite extreme.

For Danish residents who work remotely or hold dual EU citizenship, jurisdiction-shopping is a real lever — particularly given the 12-month holding exemption in Germany and Belgium, and the 0% personal long-term rate in Portugal. Denmark, however, taxes worldwide income for residents, so the exit must be a genuine change of tax residency under the rules of the Source Tax Act (Kildeskatteloven) — not a paper relocation.

The capital-income track: stablecoins, futures, financial contracts

A subset of crypto positions is excluded from the speculation classification and routed instead through Denmark's financial-contracts regime. Skattestyrelsen treats stablecoins, crypto futures, crypto options, and certain DeFi derivatives as finansielle kontrakter under Kursgevinstloven § 29. Gains and losses are taxed as kapitalindkomst (capital income) at progressive rates rather than as personal income.

The capital-income rate is itself progressive but caps lower than the personal-income ceiling. For positive net capital income above the bottom threshold, the combined rate runs roughly 37–42% depending on the municipality and the size of the income. This is meaningfully lower than the 52.07% ceiling on speculation property, which is why many active stablecoin traders pay materially less than equivalent Bitcoin traders despite identical transaction volume.

Cost basis: FIFO per asset

Skattestyrelsen mandates the FIFO (first-in, first-out) method on a per-asset basis for cryptocurrency, as set out in section C.A.5.13.7 of the official tax-administration manual Den juridiske vejledning. The earliest acquired units of any given asset are deemed sold first, regardless of which wallet they sit in. HIFO (highest-in, first-out), LIFO, and weighted-average methods are not accepted for Danish crypto reporting.

The FIFO rule is unforgiving when applied to long-term Danish holders who accumulated through dollar-cost averaging in 2017–2020. The earliest lots are also the cheapest, so partial sales realise the largest possible gain. There is no Danish equivalent of the German 12-month exemption that lets old coins exit tax-free, so FIFO directly increases the tax bill year after year for any investor who is reducing position size.

How does the FIFO calculation work in practice?

Consider an investor who bought 1 BTC at DKK 300,000 in January and another 1 BTC at DKK 330,000 in March. In June, they sell 0.5 BTC for DKK 170,000. Under FIFO, that 0.5 BTC is drawn from the January lot. The proportional cost basis is DKK 150,000 (½ of 300,000). The reportable gain is DKK 20,000 — taxed in rubrik 20 at the personal-income rate.

Activity-by-activity tax treatment

Danish crypto tax produces different outcomes for each on-chain action. The table below maps every common activity to its specific SKAT treatment.

Two activities deserve specific attention. Paying transaction fees in crypto is itself a disposal — every gas fee paid in ETH triggers a micro-realisation event against that ETH's FIFO cost basis. Hard forks are exceptionally punitive: SKAT assigns the new fork-coin a cost basis of zero, so the entire disposal proceeds become taxable gain.

The asymmetric loss-offset rule

The single most important nuance of Danish crypto taxation is the asymmetry between gain and loss treatment. Speculation gains are taxed at the full personal income rate up to 52.07%. Speculation losses are only deductible as a ligningsmæssigt fradrag — a deduction that reduces tax at the municipal rate of roughly 25–26%, not the marginal rate at which the corresponding gain would be taxed.

The practical consequences are large. Traders cannot offset crypto losses against crypto gains at the same rate, cannot use crypto losses to reduce wage income, and cannot carry forward unused speculation losses. The deduction either applies in the year the loss is realised or it disappears. KGL §29 capital-income losses are slightly more flexible — they offset capital-income gains symmetrically — but cannot cross over into the speculation regime.

The only legitimate planning response is timing: realise gains and losses in the same calendar year so that at least the municipal-tax asymmetry is the only friction, rather than the full marginal asymmetry. Tax-loss harvesting in Denmark is best done during a single tax year, with full attention to FIFO ordering across wallets.

Gifting and inheritance

Crypto gifts to close family in Denmark are subject to a separate gift tax (boafgift) of 15%, applied above an annual bundfradrag of DKK 76,900 in 2025 for gifts to children, grandchildren, and parents. Gifts to siblings or unrelated parties fall outside the boafgift regime entirely and are instead taxed as personal income to the recipient — typically at significantly higher effective rates.

- Children, stepchildren, grandchildren

- Parents and stepparents

- Cohabiting partner (after 2 years of shared residence)

- Spouse — fully exempt regardless of amount

- Siblings, nieces, nephews

- Friends and unrelated parties

- Distant relatives outside the boafgift list

- Charitable organisations — separate exemption rules

Modest occasional gifts at customary thresholds — birthdays, Christmas, weddings — are exempt from gift tax under the customary-gifts exception, provided the value is appropriate to the giver's economic standing and the relationship. There is no statutory DKK figure; SKAT applies a reasonableness test on a case-by-case basis.

Worked examples

The same DKK 100,000 of crypto activity can produce dramatically different tax outcomes depending on the regime that applies. The four cases below use realistic 2025 numbers and each country-specific rule from the table above.

Filing: Box 20, kapitalindkomst, Form 04.003

Most crypto income lands in rubrik 20 (Box 20 — anden personlig indkomst) of the Danish oplysningsskema. Capital-income items from KGL §29 — stablecoins, futures, derivatives — are reported separately in the relevant kapitalindkomst rubrik. International filers without TastSelv access use the Form 04.003 EN paper return.

Skattestyrelsen has been actively requesting transaction data from Danish and EU exchanges since 2018, and DAC8 reporting from 2026 will close most remaining information gaps. Audit triggers include unreported wallet activity flagged by exchange data, mismatches between declared income and observed lifestyle, and pattern-matching on stablecoin flows. The retention requirement for crypto records is five years from the end of the tax year, in line with the general bookkeeping law.

Crowdlending as a cleaner reporting profile

The combination of FIFO per-asset reporting, asymmetric loss treatment, and the silo between speculation income and KGL §29 capital income makes Danish DeFi tax reporting unusually complex. Each yield-farming claim, each LP rebalance, each protocol migration creates a separate disposal event that must be priced in DKK at the precise moment of the transaction. The fixed-income structure of regulated crowdlending offers a meaningfully cleaner alternative.

Predictable on-chain income, in a wrapper SKAT can read directly

8lends is the Web3 expansion of Maclear AG, a Swiss-based P2P crowdlending platform operating under Swiss financial regulations as a member of PolyReg SRO. Where Maclear funds SME loans in EUR through traditional banking, 8lends funds equivalent projects in USDC on the Base blockchain — same diligence, same collateral, on-chain settlement, full audit trail.

For Danish reporting, the wrapper matters. Each loan disburses on a known date for a known principal at a known fixed interest rate. Monthly interest payments arrive at consistent DKK-equivalent values. Every transaction — investment, interest payment, principal return — is timestamped on Base and exportable as CSV. There are no impermanent-loss reconciliations to perform, no oracle prices to interpolate, no nested protocol positions to unwind. The interest stream maps cleanly to rubrik 20 personal income; the underlying USDC sits in the KGL §29 capital-income silo.

Each borrower passes 40+ due diligence criteria assessed by Maclear AG, with a 1–10 internal risk score. Loans are collateral-backed, monitored continuously, and supported by Maclear's Provision Fund — a reserve formed from a portion of platform commissions used to cover temporary borrower repayment difficulties.

Crowdlending does not change which Danish tax regime applies — it changes how easy it is to comply. A regulated platform with on-chain settlement produces the kind of granular, timestamped, counterparty-identified record that Skattestyrelsen explicitly asks for. For investors already filing rubrik 20 on Bitcoin or Ethereum disposals, adding a structured income stream on 8lends adds yield without adding reporting complexity.

Conclusion

Denmark's crypto tax system is predictable but punishing. Most disposals run through the personal-income stack at rates capped by the skatteloft at 52.07% in 2025; stablecoins and financial contracts route through the parallel KGL §29 capital-income regime at roughly 37–42%. There is no holding-period exemption, FIFO is mandatory, and the asymmetric loss-offset rule means break-even years still produce real tax bills.

Strategic planning in this environment focuses on three levers: timing gains and losses in the same year to limit the asymmetry, classifying positions correctly between the speculation and capital-income silos, and selecting income structures — like fixed-rate crowdlending — whose reporting profile is easier to manage than open-ended DeFi yield. With DAC8 reporting going live in 2026, the cost of getting any of these wrong is rising fast.