Financial Surveillance Mechanism

Calculating debt to the state is not the primary function of the document. Rather, it is designed to help the nation monitor residents' offshore digital holdings. It also helps France track money laundering compliance and transparency, ensuring complete visibility into overseas virtual currency activities for the authorities.

On the other hand, blockchain investors use it as an annual reporting requirement, though it carries equally serious consequences for non-compliance, it operates entirely separately from income tax calculations.

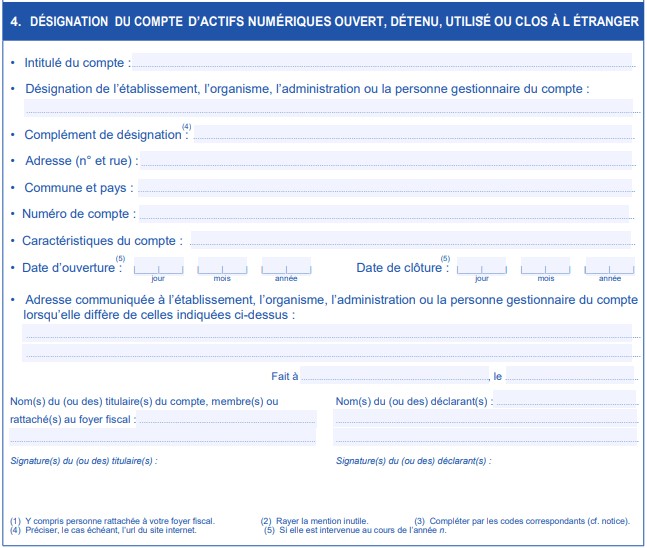

According to the Tax Code requirement, Article 1649 AA mandates that tax residents declare all foreign financial profiles. Furthermore, DGFiP recently ended years of regulatory uncertainty with its inclusion of digital possessions within this framework. Here are the official objectives of Form 3916-bis:

- Ensure anti-money laundering regulations compliance

- Visibility of a comprehensive financial portrait of residents

- Cross-border virtual cash movements monitoring

- Automatic information exchange support

Who Must File: The Scope is Broader Than You Think

Regardless of profile activity level or size, all tax residents holding virtual money on offshore platforms are required to file, provided you own an offshore virtual cash account. More importantly, some mandatory filing criteria apply.

Tax residents, including French citizens living abroad who maintain tax residency, must file if they hold blockchain assets on apps not established in France. This also applies to offshore nationals residing in the country.

Platforms, including exchanges, custodial platforms, or wallet services, are classified as "foreign" as long as they are not regulated by the authorities. By this definition, nearly all major sources fall into this classification. Also, mandatorily, all foreign crypto accounts must be declared regardless of value. This is because the doc has no minimum value threshold, and DGFiP guidelines stipulate declaring even trader wallets with €50 in assets.

Still, apps such as hosted wallet services, margin trading wallets, traditional exchange accounts, and staking-as-a-service resources where control of private keys is maintained by a third party requires declaration. However, there are exceptions, and they include personal software and hardware wallets controlled by individuals. These don’t require any declaration.

Filing is often more complex than it appears. Many digital asset holders struggle to organize offshore exchange profiles, determine which wallets qualify, and maintain verifiable transaction records. 8lends simplifies this process by centralizing all your crypto wallet data into a single, compliant system. With automated monitoring, documentation, and verification tools, you can ensure your declarations meet every French reporting standard without manual effort.

Filing Deadlines

Separate from standard income tax deadlines, Form 3916-bis operates on its own. This can create possible timing traps for unprepared investors. Consequently, you will need to understand the annual reporting schedule and prepare appropriately to avoid penalties.

The primary deadline is usually June 30th following the fiscal year. This means you must declare 2024 activities by June 30, 2025, and 2025 activities by June 30, 2026. This deadline is also accompanied by rules that must be included in your considerations when preparing your declarations.

- Profiles open during the fiscal year must be declared.

- Extensions are not granted automatically.

- Reporting requirements still apply for holdings closed during the year.

- Immediate penalty assessment is triggered for late filing.

Investors who assume all digital currency-related filings occur simultaneously stand the risk of non-compliance. Hence, you should take cognizance that the June 30th deadline for the document comes many weeks after income tax filing deadlines.

Required Information: Documentation That Determines Success or Failure

The information required to be included is specific to ensuring financial monitoring and, as such, demands careful documentation of year-round transactions. Required information includes profile identification requirements (platform details and account-specific information) and value calculation requirements. The table below lists the information under each requirement.

It is essential to note that crypto accounts require a declaration of the yearly maximum balance attained, unlike conventional banking, which does not require such a declaration. For the example below, the peak value of €78K was recorded in May

Year-round Profile Activity:

- January: Total value = €32K (0.5 BTC + 10 ETH)

- May: Total value = €78K (1.2 BTC + 25 ETH) Profile peak

- September: Total value = €18K (0.3 BTC + 8 ETH) Profile drops

- December: Total value = €24K (0.4 BTC + 12 ETH) Year-end total value

Reportable Amount: €78K (May peak value)

Multiple Account Management: Navigating Complex Portfolio Declarations

It is instructive for French blockchain asset investors holding multiple holdings across different resources to ensure that each app is declared separately with a different 3916-bis Form. Consider the multi-platform portfolio example below, each app declares its peak balance on separate versions.

Multi-Platform Portfolio (all requiring separate 3916-bis forms):

- Binance: Peak €25K

- Crypto.com: Peak €8K

- Coinbase: Peak €15K

- Total Compliance Requirement: Three separate filings

Additionally, according to the tax rules, consolidated reporting across multiple resources is not permitted. Hence, every peak balance, platform-specific information, including supporting documents, must be documented individually for each customer file.

Record-Keeping Framework: Building Audit-Proof Documentation

Developing a systematic approach to keeping your yearly blockchain transactions records already sets you up for Form 3916-bis compliance. However, you’ll need an excellent grasp of all the essential documents you need and a proactive approach to a documentation scheduling framework.

Essential records are categorized as transaction and valuation documents, and each record should be collected and kept safely (see table below).

Also, it is recommended that you divide your documentation schedule into monthly and quarterly schedules for more effectiveness.

Statements are crucial records, and having evidence such as screenshots of transactions and profile statements, as well as downloading statements, is essential.

Every month, ensure to screenshot profile statements, download transaction statements, and document significant changes in statements.

Every quarter, you can verify active account status, update peak balance calculation, reconcile multi-platform records, and do a preliminary information preparation for Form 3926-bis.

Penalty Structure: The High Cost of Non-Compliance

While the process of keeping and documenting records of yearly bitcoin and altcoin transactions can cost you some effort and time, the effect of non-compliance can be far-reaching for your financial position. This is because France imposes severe penalties to defaulters of Form 3916-bis. For instance, it prescribes €750 fine for undeclared profiles below €50K and €1,500 fine for peak balances above €50K.

Say, you have three undeclared customer files: Coinbase €15,000, Binance €30,000, Crypto.com €8,000, your penalties will be calculated as €750 × 3 accounts = €2,250 (total penalty). However, a more severe sanction may apply to individuals with incomplete or falsified information.

Apart from these basic penalties, France also imposes penalties of up to €10,000 for accounts held in high-risk jurisdictions. These are countries without information exchange arrangements with the country. There are also criminal tax evasion charges that can be levied against individuals with serious violations, especially when there is a consistent pattern of non-compliance or when large balances are undeclared.

Common Pitfalls and Prevention Strategies

This post won’t be complete without highlighting the most common pitfalls you are likely to encounter in filling it out. They include:

- Thinking you don’t need to declare small balances

- Failing to file separate forms for each app

- Peak values and year-end balances errors

- Wrong categorization of resource locations

- Missing the June 30th deadline

These are preventable errors, and taking measures that include automated reminder systems and taking a comprehensive inventory of your holdings can save you from unnecessary fines.

Conclusion

Finally, paying penalties is often more than the gain that non-compliant crypto traders are trying to preserve. Therefore, it is more beneficial to build a system that helps stay compliant when dealing with offshore blockchain holdings and filing Form 3916-bis.

Additionally, a thorough understanding of the requirements of this Form will serve as a foundation for future financial security and long-term compliance. Still, future changes to the document are inevitable considering the nation’s dynamic tax regulatory landscape. What will help you as an investor is to position for any changes by adopting a transparent approach and meticulous record-keeping, as this will be central to any future policy change.

Form 3916-bis is one of the most overlooked yet financially consequential parts of crypto compliance in France. Staying ahead of reporting deadlines and maintaining error-free records requires more than discipline – it demands the right tools. 8lends’ compliance automation solutions help you prepare, organize, and file with confidence, no matter how many accounts or platforms you manage. From crypto balance tracking to foreign account declarations, 8lends makes regulatory compliance effortless.