UK Virtual Currency Obligations

You might be wondering if residents have to pay on blockchain assets. The short and sweet answer is that it does.

As mentioned earlier, His Majesty's Revenue and Customs, also known as the HMRC, is the government body in charge of fiscal administration. They see virtual cash as a digital asset that must be paid on and have established two main taxes, with the first being capital gains.

Capital Gains

If you profit from selling digital assets, you'll owe for capital gains, not the total value of the sale.

A few common events that trigger this are:

- Trading digital assets: Think of it this way: if you swap BTC for ETH, DeFi tokens, and stablecoins, you owe the government.

- Trading digital assets for fiat currencies like GBP, USD, JPY, EUR, etc.

- Using digital coins to pay for anything.

Since you’re probably curious about it, you should expect to pay 10% to 24% as capital gains obligation. Mind you, these figures are for the 2025 to 2026 fiscal year.

Income tax is the second type that the UK government applies to virtual coins.

Income

Do you mine, earn rewards from staking, or accept digital assets as payment? If you do, guess what? You may owe the government.

Actions known to bring about income duties include:

- Wages paid in blockchain securities.

- Events that generate new tokens from mining and earning rewards from staking.

- Generating new virtual assets or gains from hard forks or airdrops.

The rate ranges from 20% to 45% in the current year (2025/2026).

Legality of Obligation Reduction

This is totally legal in most countries, Britain being no exception. In fact, HMRC has relief guidelines that can lower how much you owe. What’s illegal is evasion; it could land you in big trouble with the law.

Evasion consequences are stiff; you might get seven years in jail or fines that would make your eyes pop out of their sockets. Those are the key matters you ought to know about in British fiscal obligations for digital assets. Since tax evasion is illegal, we’ll only discuss strategic ways to reduce your debt.

7 Ways to Decrease Your Obligation to the State

Let’s jump right in:

1. HODL

Although it has now become a meme, hold on for dear life (HODL) is the most overlooked but effective reduction method.

The strategy is straightforward. Trading, selling, or swapping coins for GBP, USD, JPY, and other virtual coins, or using them to pay for anything, attracts either of the two taxes we highlighted above. Because of this rule, guess what? You should continue HODLing to ensure your wallet doesn’t trigger an obligation to pay the British government.

And if you’re thinking, “Since I’m clever, I’ll hide my transaction data,” woe unto you because guess what? Come January 2026, the HMRC will have full access to all transaction data, so there goes that plan.

Back to HODLing. Think about it this way: if your Bitcoin value skyrockets, but you keep HODLing, your history won’t have a record triggering state debt.

Do you want to know the beauty of this strategy? When your Bitcoins appreciate, you’re likely to net and keep more, especially because you can wait for a low-income or loss-setting year to sell.

2. Exploit annual deductions

Imagine you’ve HODL-ed digital assets all year long, and they’ve appreciated by £4,500; now you’re freaking out and scratching your head for ways to ensure the government doesn’t get its hands on all your hard-won gains. What do you do?

Since we don’t want all that head scratching to leave a bald spot, we’ll tell you what to do: utilize every deduction available to you! For context, the state authorities give every payer an annual write-off. £3K is the current year’s capital gains deductible.

In other words, if your annual capital gains, including from blockchain dealings, fall below £3K, you’ll pay a big fat £0 for capital gains.

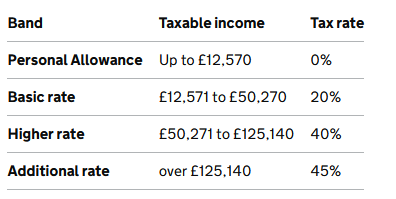

Check out the table below that shows the current income brackets.

If all your net income, including from virtual money, is below £12,570, you’ll owe the government a whopping £0. How nice is that?

3. Try loss harvesting tactics

Here’s a fun fact that remains unknown to most traders and investors: Strategically selling unprofitable coins can reduce your debt since you can claim and use those to offset capital gains made by your best-performing virtual cash.

Practically, this may look like taking a loss on your Bitcoin Diamond to balance out the capital gains made from selling other top-performing digital currencies. The catch? Well, you actually have to take a loss on depreciating or loss-making bitcoin or altcoins.

Want some other harvesting tips? Here you go:

- Sell loss-making coins before April 5th: Curious about the importance of this date? Simple: that’s when the British fiscal year ends.

- Use the bed and breakfast rule: to offload and take a loss on unprofitable assets, but rebuy them after 30 days to cut your bill.

- Try lots of tools: the best ones can unearth hidden losses (more on this later).

4. Gifting

Do you have an officially recognized spouse, with a marriage certificate and all that? Feeling charitable and you’re 100% certain that your favorite charity is legally registered? If so, you might want to consider giving your wife, husband, or charity of choice some of your gains.

Care to guess why and how that works to your advantage come filing time? The answer is the no gain/no loss disposals rule. This little-known rule receives accolades as a reduction strategy because, according to the HMRC, transferring assets to your civil partner or a registered charity attracts zero capital gains debt.

The catch? The gift has to be real and genuinely transferred to your partner or preferred charity. That act permits you to deduct the asset’s fair market value at the time of gifting it.

The annual tax-free gifting exemption is £3K. Want to see how effective this strategy is? Let’s look at a hypothetical example.

Let’s assume you bought Ethereum at £3,000 and it has appreciated to £6,000 within the same year. In this example, you can give your civil partner £3,000, who can then claim it as part of their annual exemption.

As for bequeathing virtual cash to charity, ensure you get nothing for donating; that’s the legit way to ensure the HMRC doesn’t consider the donation as something that has to be paid on.

5. Use software tools

Virtual money platforms have tools that keep your investing endeavors compliant. Besides literally dumbing down policy on virtual asset ownership, some of these platforms have ‘hidden gem’ loss harvesting tools that can reveal overlooked deductions.

Managing virtual coin obligation effectively isn’t only about finding deductions — it’s also about maintaining accurate records, demonstrating compliance, and preparing for audits. At 8lends, we help organizations simplify governance, risk, and compliance through intelligent automation and transparent oversight. Explore how we can help.

6. Deduct transaction fees and costs

So, you’ve sold some Bitcoins and netted a good profit (kudos for that). Everything we’ve discussed so far should tell you that the British fiscal department expects you to remit capital gains on the amount.

Since we’re sure you’d rather keep most of those profits, why not use the government’s rules against it by using cost deductions to reduce how much you owe? Legally, you can write off contract, valuation, and advertising costs, not to mention transaction/transfer fees, and any other expense related to closing the asset sale.

While such deductions probably won’t reduce your debt by a whole lot, look into them because every deducted cost leads to what? You guessed it: more of your earnings and gains remaining in your pockets (where they belong).

7. Consider trading as a business

If you’re a professional blockchain investor who trades consistently, formalizing your activities and operating under the umbrella of an LLC or another legally recognized business entity can cut your digital coin burden.

However, since the government can use the CARF framework to access transaction data, only business-related costs count here. Such costs include:

- Those who engage in high-frequency trading.

- Mining operations.

- Accepting coins in exchange for goods and services.

- Offering coins-based services like marketplaces and tools.

Operating a digital money venture under a legal business structure is advantageous for savings because it allows you to deduct expenses you otherwise wouldn’t under the personal regime.

For instance, as a business, you can deduct costs like:

- Wallets, analytics, software tools, and other subscriptions related to running your business.

- Transaction fees, accounting, legal, and other fees for professional services.

- Rent and other utilities related to running your business.

- Coins-related training, rigs, laptops, servers, and other things used by the business.

Deducting such expenses can significantly lower your capital gains and business-related bill.

Conclusion

There you have it: seven legal steps you can take to reduce your virtual cash debt as a UK investor. While these strategies are practical and easy to apply, it would be remiss not to mention that consulting a registered professional is the ultimate way to find deductions that can lower how much you pay the government.

Staying compliant with evolving crypto tax laws doesn’t have to be complicated. 8lends’ GRC solutions give businesses the structure and visibility they need to stay compliant while minimizing operational risks. It also provides revolutionary credit-scoring methods based on the leading agencies to help investors profit handsomely from crowdlending backed by collateral.