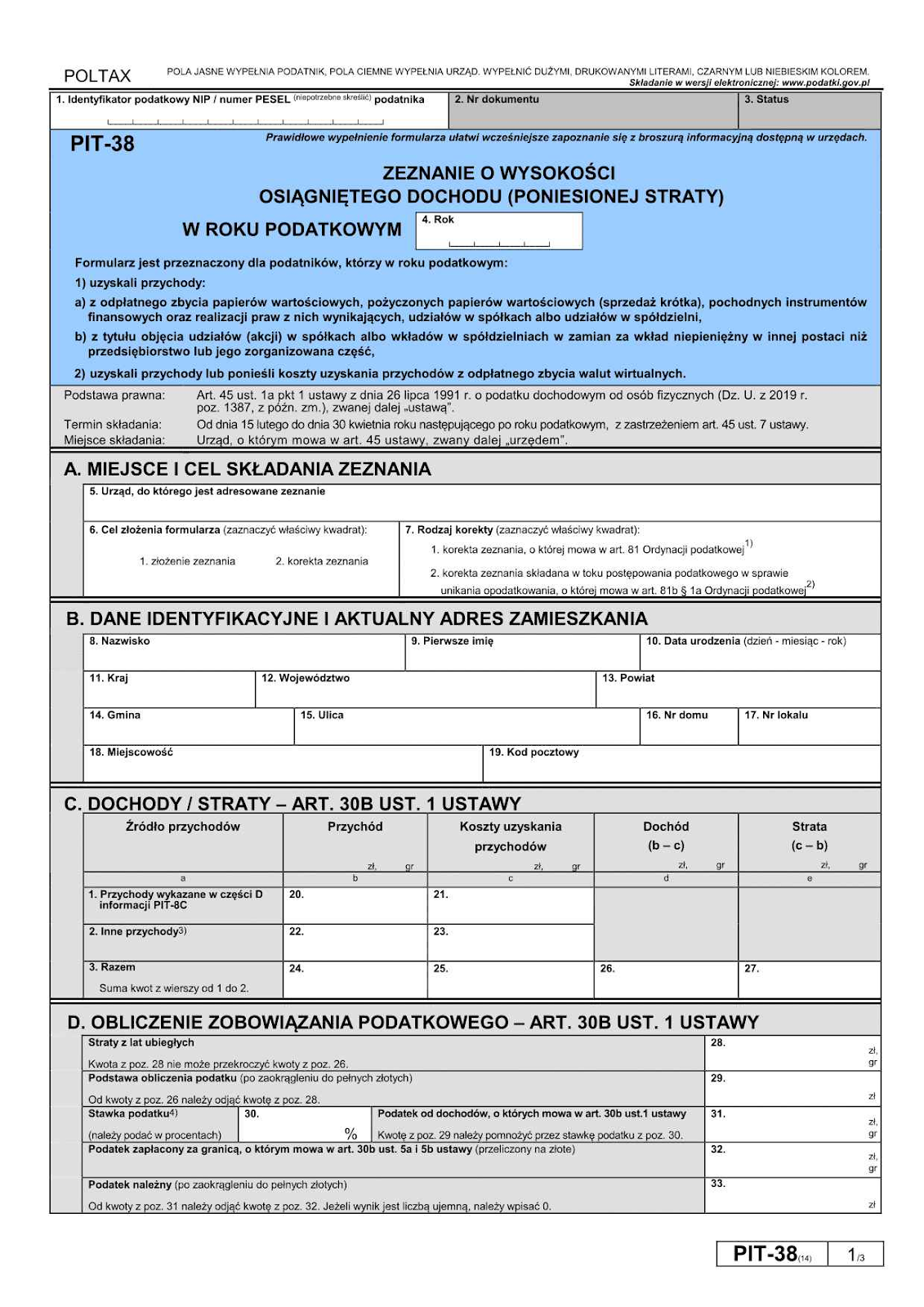

The PIT-38 and Cryptocurrencies

This is the form traders will have to file between February 15th and April 30th every year which covers the entire previous year, from the 1st of January to December 31st, regardless of whether they made that income on a foreign platform. If they went into the red for the year, they will still have to file, and those losses will come in handy for the next filing period in reducing the amount they owe the 19% gains tax on.

What Traders Owe Taxes On

Traders do not have to pay tax on crypto that they currently hold or virtual cash that they acquired for rendering particular services or mined. It only applies when digital assets have to be converted to fiat, primarily when it is:

- sold for fiat currency

- used to pay for goods or services: paying with virtual cash for products, subscriptions, travel, or services triggers a tax obligation

- otherwise exchanged in a way that produces measurable value in PLN

Costs related to acquiring digital coins, such as purchase price and transaction fees, may be deducted, and unused costs may be carried forward to future years if no debt-incurring disposal occurred in a given year.

Other Forms

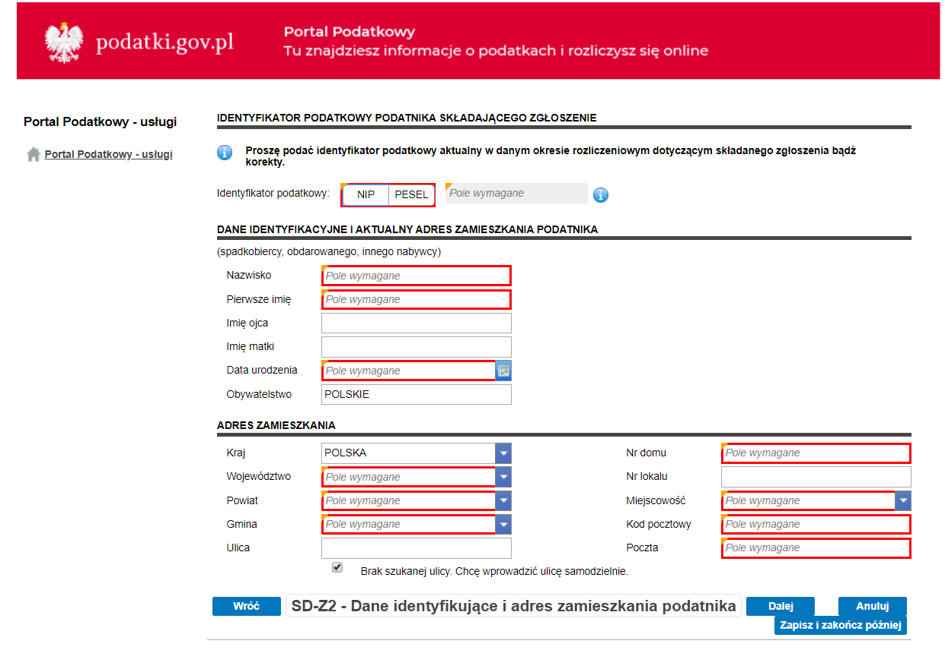

Users may also need to file additional forms depending on how the virtual cash was acquired or used. One important example is the inheritance and donation return (SD-Z2 or SD-3). If digital coins are received as a gift or through inheritance, they are not reported in PIT-38 at the moment of receipt.

Instead, it falls under inheritance and donation tax regulations. Close family members who qualify for full exemption must file SD-Z2 within 6 months of receiving the digital assets to preserve that exemption.

Taxable vs Non-Taxable Scenarios

When Bitcoin, Ether, or another token is sold for PLN or another fiat currency, the resulting gain must be reported in PIT-38 and charged the flat 19% rate.

Important free situations:

- Just buying digital coins using fiat, like zloty or euros

- Receiving coins in any form, whether paid for or not.

- Swapping one virtual asset for another

However, these transactions still matter for record-keeping purposes, as they affect how acquisition costs are tracked and later allocated when a debt-incurring disposal eventually occurs, since the original amount paid for the digital cash is taken as the cost basis from which any gains are measured. Payers should also be aware that partial disposals can occur. If only part of a holding is sold or used, debts incurred only for the portion disposed of, with costs allocated proportionally.

Mining and Validator Income

In order for expenses on crypto gains to become deductible, they have to be directly associated with the transactions in which the gains materialized. The way mining works is, unlike trading fees, you cannot write off any expenses, such as electricity or hardware, that you spent in the process of pursuing that digital coin, nor do you owe taxes for acquiring it. However, later on, if you sell it and make a profit, you will owe 19% on that.

DeFi Lending and Yield Farming

Loans in cryptocurrency are not subject to PCC (tax on civil law transactions), since virtual money is considered a property right rather than traditional money or a tangible good, and PCC applies only to certain categories of property or cash loans. The KAS confirmed this in multiple interpretations. Nor are they generally subject to VAT. However, it is when you dispose of the additional digital assets acquired at a higher value than 19% is to be paid.

While cryptocurrency remains a popular way to seek higher returns, some investors look for alternatives that offer more predictable structures and clearer fiscal treatment. One option gaining attention in Europe is crowdlending, where individuals can earn returns by funding loans issued to vetted borrowers.

Platforms such as 8lends connect investors with credit-worthy borrowers who may not qualify for traditional bank financing. Instead of relying on a single lender, each loan is typically funded by many investors, which helps spread both cost and risk across the platform’s user base. This model allows participants to access relatively high interest rates while avoiding exposure to a single borrower.

Staking Rewards

Like mining, you do not create tax on crypto that you generate for yourself. That said, once you dispose of that crypto, the cost basis for what you acquired the virtual cash at will be 0, since you didn’t buy it, and the difference between 0 and what you disposed of the crypto at will be charged 19%.

Gifts & Inheritance

The act of receiving the gift does not create income relevant under PIT-38. Instead, it is subject to donation charges rules, to which airdrops, mining, and staking digital cash are also subject. Inheritance, on the other hand, features a broad range of situations that determine state debt, and it isn’t treated any differently for being virtual money.

In Poland, inheritance tax applies to assets located in the country and to assets abroad owned by Polish residents or nationals. Close relatives in bracket 1 — including spouses, children, grandchildren, grandparents, siblings, and step-relatives — are fully exempt from inheritance charges if the deceased passed away after 1 January 2007. To benefit from this exemption, you must submit the SD-Z2 form within 6 months of official confirmation of inheritance; missing this deadline triggers standard rates.

For other beneficiaries, the taxable net asset is calculated by subtracting debts from total inherited assets, and each heir pays tax on their share after applying any personal allowances. Non-exempt heirs must file the SD-3 declaration within one month of the court confirming the inheritance, plus provide proof of relationship, details of the inheritance, court confirmation, debts, and related costs such as funeral or medical expenses. If there are multiple heirs, an additional SD-3A form is required.

NFTs

These are like mining and staking where the same 19% rate applies if you sell them for fiat, but minting is not deductible.

Losses

Bad trades from cryptocurrency transactions may be carried forward and used to offset future crypto gains. They cannot, however, be used to reduce employment income or other categories of income. Declaring losses in PIT-38 is therefore important even in years when no debt is incurred.

Only losses arising from taxable disposals are relevant. Unrealized losses from holding depreciated crypto do not count. Though corporations enjoy much better privileges in the law.

Conclusion

Crypto taxation in Poland in 2025 is built around the principle that debt arises when value is actually realized, but the rules become more nuanced once real-life situations are involved. Inheritance, gifts, staking, NFTs, and DeFi activities can all trigger different reporting duties depending on how and when crypto is acquired or disposed of. Understanding the rules is major for staying compliant and avoiding costly mistakes.

For investors looking to diversify beyond crypto while maintaining a structured and transparent income model, crowdlending can be a practical alternative worth exploring. Platforms like 8lends allow investors to earn returns from high interest rates paid by creditworthy borrowers who were unable to access traditional bank financing. Risk and expenses are distributed across many investors, while a sophisticated credit-scoring system – built using data from leading credit agencies – helps assess borrower reliability before loans are funded.

If you’re exploring ways to balance higher-risk digital assets with more structured return opportunities from socially significant projects, 8lends offers a data-driven approach to investing through crowdlending.