What is P2P Lending?

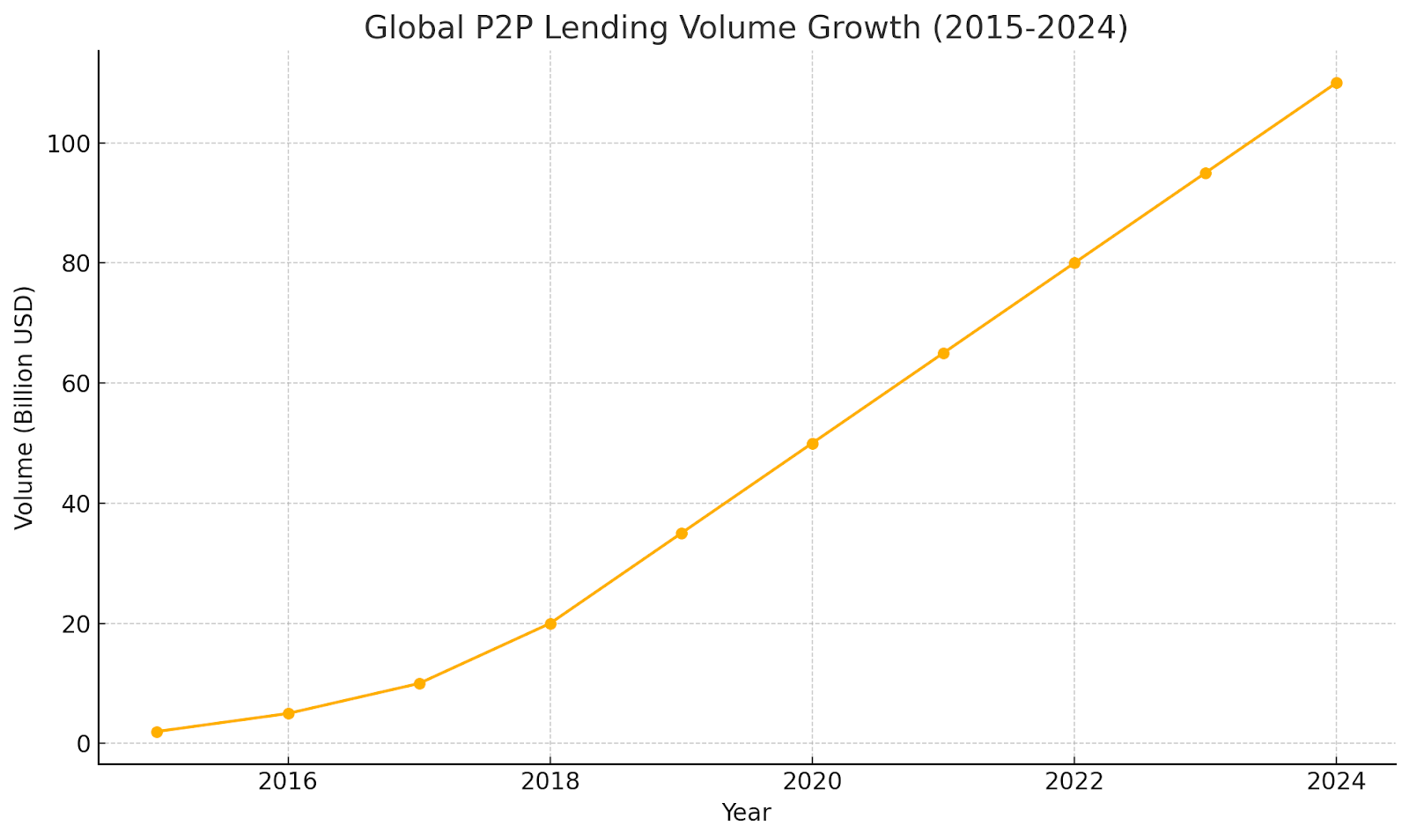

Peer-to-peer lending began as a new choice beyond banks so that lenders could earn more and borrowers could get money faster. Yet the risks are often missed. Borrowers can default, and platforms have the possibility of failing. P2P lending grew out of crowdfunding and expanded fast when fintech took off, bringing many new users on board. Yet some ideas about its dangers are off the mark, and that can lead to choices that cost people.

The biggest problems though are the myths that grew with the popularity of P2P lending. Let’s tackle eight of these myths while backing up our stand with up-to-date data and expert insights.

Detailed Misconceptions and Realities

Many investors put all their faith in broad claims about peer-to-peer lending without reading the fine print. Digging into the real rules, tools, and safeguards gives a clearer view of what lies ahead. Some stories make P2P lending sound like a free-for-all. Others make it seem safer than it truly is.

We will cut through the hype and show the frameworks and practices that shape real outcomes. This close look explains how regulation, credit checks, default handling, and market shifts work together so that your choices rest on solid ground. With that settled, we can tackle the first big myth.

Misconception #1: P2P Lending is Unregulated and Unsafe

Myth: Many investors think P2P lending runs without rules like the Wild West and is very risky.

Reality: P2P lending faces rules in many places. In the UK, the Financial Conduct Authority (FCA) has overseen it since 2014 so that platforms follow clear standards and protect users. In India, the Reserve Bank of India (RBI) set rules in 2017 requiring clear disclosures, escrow accounts, and risk warnings. Rules cut some risk, but defaults and platform failures still happen, so investors need to stay alert.

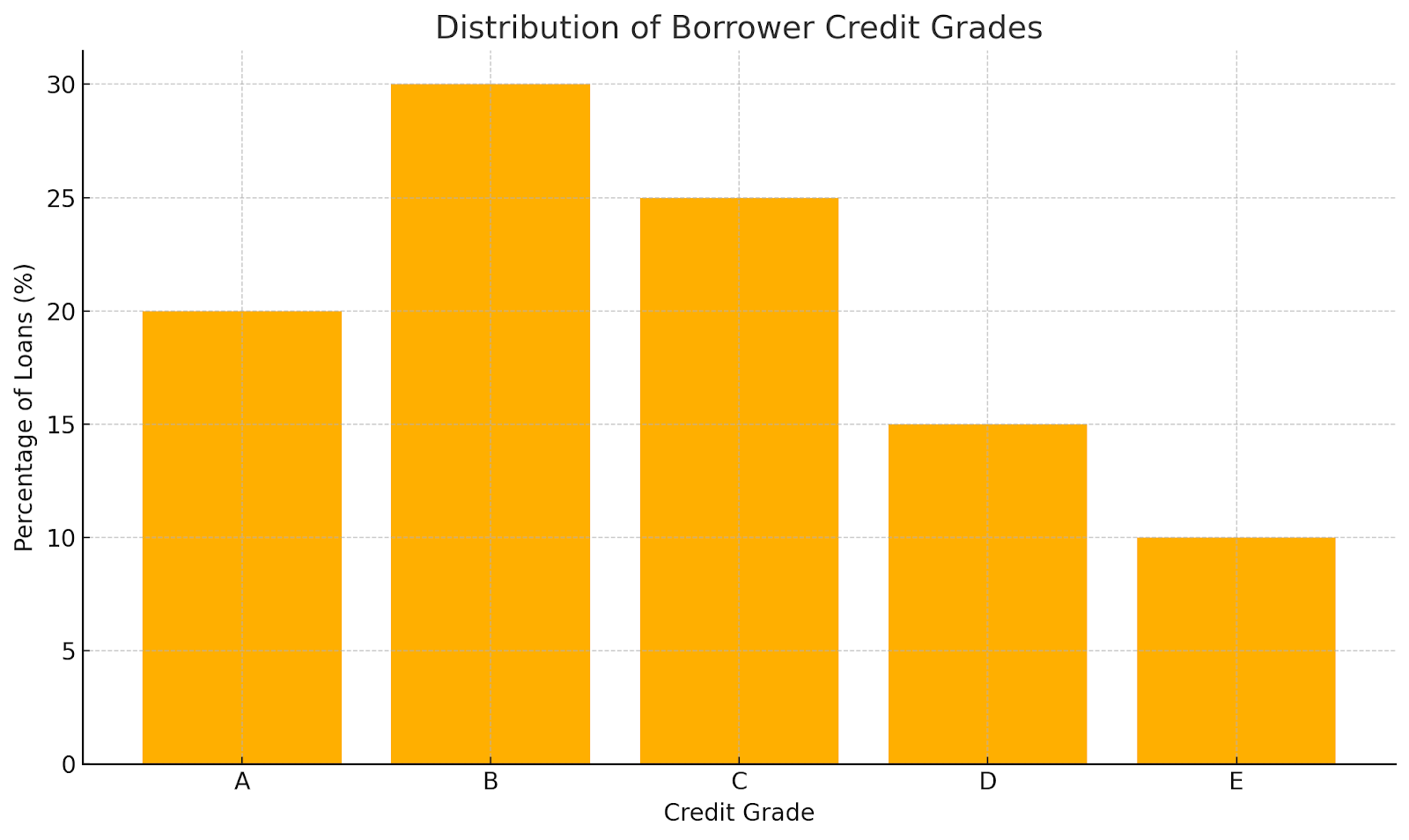

Misconception #2: All Borrowers on P2P Platforms Are High-Risk

Myth: People assume P2P only serves borrowers that banks reject.

Reality: Platforms use tools and data to check credit. 8lends, for example, shows detailed borrower stats so lenders can judge risk for themselves. In Switzerland, rules force platforms to match lenders with a mix of credit grades, from top to lower scores. Investors choose loans by score, which cuts the sense that all borrowers are risky.

Misconception #3: P2P Lending Platforms Guarantee Loans

Myth: Some believe platforms insure loans like banks do with deposits.

Reality: Most P2P sites only connect lenders and borrowers. Lenders bear all the credit risk if a borrower can’t pay. Investopedia warns that lenders must plan for defaults. RBI rules in India bar platforms from promising repayment support. A few platforms offer “provision funds,” but these vary in scope and do not guarantee full repayment.

Misconception 4: Diversification Eliminates All Risk in P2P Lending

Myth: Spreading money across many loans eliminates all risk.

Reality: Putting money into many loans cuts the hit if one fails, but it does not remove other risks. Experts note risks like too much exposure on one platform or a broad market downturn. A study shows that lending too much to any one borrower still raises default probability. Diversification helps, but it is not a complete shield.

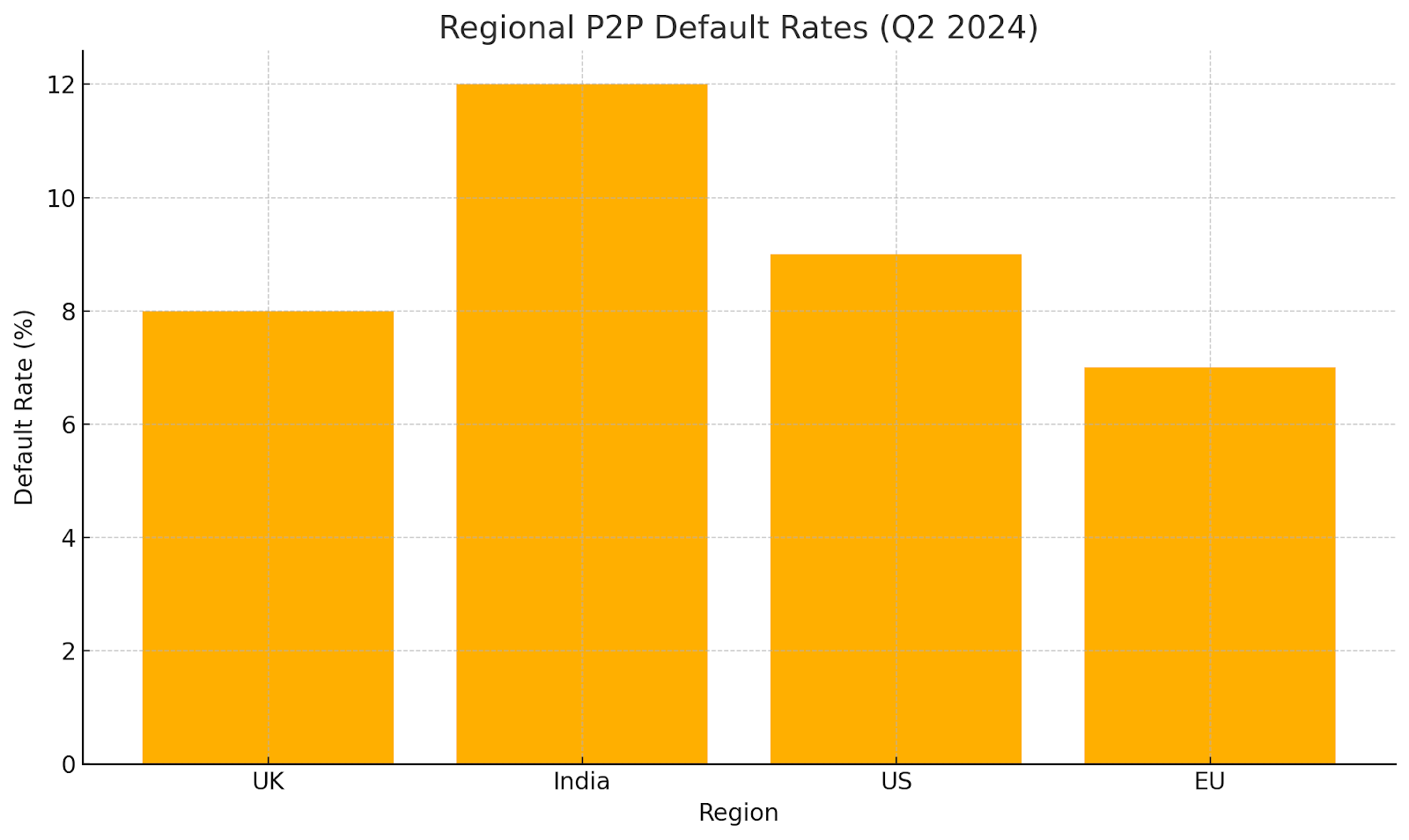

Misconception #5: P2P Lending is as Safe as Bank Deposits

Myth: Some compare P2P safety with bank savings accounts.

Reality: Bank deposits often carry government insurance, but P2P loans do not. Individual investors take all the risk. P2P default rates can top 10 percent, while bank delinquency sits near 1.4 percent as of Q2 2024. Higher returns reflect higher risk, making P2P very different from a savings account.

Misconception #6: It’s Impossible to Assess Risk in P2P Lending

Myth: Many assume risk checks are too complex or that data is lacking.

Reality: Platforms give plenty of tools: credit scores, loan grades, and past performance charts. Third-party services like Orchard and dv01 add more layers of risk analysis. Investors use these details to match loans to their own comfort level.

Misconception #7: P2P Lending Investments Are Highly Liquid

Myth: Investors often think they can pull out money anytime.

Reality: Liquidity depends on the platform. Some run a secondary market for loan sales, but that can dry up in tough times. Experts warn that if loans can’t be sold early, cash stays locked up, and you may miss other chances. Planning for possible delays is key, especially without a firm secondary market.

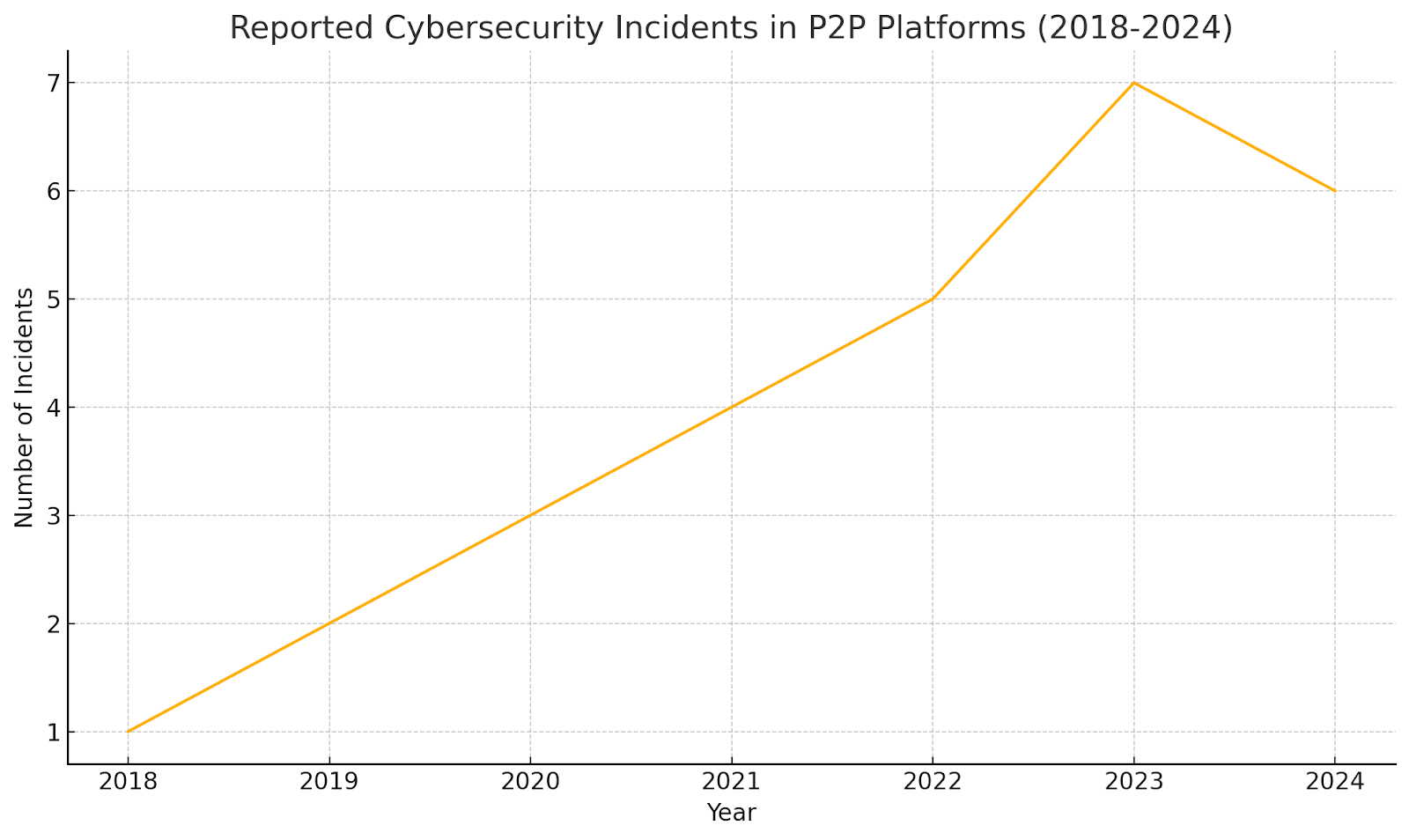

Misconception #8: P2P Platforms Are Immune to Cyber and Operational Risks

Myth: P2P sites never suffer hacks or outages. Lenders assume their data and money stay safe at all times.

Reality: Platforms face cyberattacks and system failures that can expose personal details or lock up funds during downtime. Breaches may lead to identity theft or fraud, while outages stop loan servicing and trading.

To guard against this, solid platforms like 8lends use encryption, multi-factor authentication, regular security audits, pen tests, and clear incident-response plans. Before you lend, check a site’s security certifications and published risk controls so that you know how it handles these hidden threats.

To further illustrate, here's a table summarizing the risks and corresponding misconceptions:

Cross-Border Lending and Regulatory Divergence

Cross-border P2P lending brings its own set of legal and regulatory headaches when money moves between countries. Each place has its own consumer safety rules, money controls, and tax laws that may hide extra fees or legal traps. Doing solid legal homework, picking platforms that lay out all their rules clearly, and learning how local fintech rules work are key steps to expand abroad safely.

Implications for Investors

Knowing these mistakes helps you handle risk better. Investors need to look into platform rules and review borrower backgrounds so that they understand who they are backing. Accept that loans can go bad. Spread your money around to lower risk.

Remember, it is riskier than banks. Use tools to check risk and plan for cash needs. The peer-to-peer lending market is growing, and AI credit scoring brings new help, but learning remains key.

Conclusion

Peer-to-peer lending provides good opportunities to earn returns. It requires a clear view of the possible downsides though so that you do not get caught off guard or take more risks than you want. Cutting out false beliefs lets investors make choices that fit their needs and what they can handle.

So far 8lends has yet to experience a default or a late payment and while risk can never be totally eliminated, it can be managed wisely and strategically. Collateral is used to back loans in case borrowers do default though and investors are charged zero commission on their earnings.