Is This Platform Playing by the Rulebook?

You never drive without brakes. So why would you invest through a P2P platform that isn't licensed or regulated?

There's no guarantee that the platform follows any legal or ethical standards without financial oversight. Your money could be exposed to mismanagement, and there's often little recourse if things go wrong in the absence of regulation.

That's why checking a platform's regulatory status should be your first step. Don't invest if the platform doesn't have this checkmark. In many regions, financial authorities or self-regulatory organizations are tasked with monitoring P2P platforms to ensure they operate fairly and transparently. In Switzerland, for instance,

The PolyReg Services GmbH member upholds top-tier financial standards and undergoes regular audits. This platform follows Anti-Money Laundering (AML) and data protection laws. All these credentials give you peace of mind that you are dealing with a company that prioritizes transparency and accountability.

How Many Loans Go Belly-Up on This Platform?

You want to keep the risk level as low as possible. That's why you must find out the default rate.

A high default rate is a red flag. It often reflects poor borrower screening or an unstable lending environment. Your expected returns can quickly shrink or even turn into losses if too many borrowers default.

An investor spread €5,000 across 10 loans on a platform with a 10% default rate. This means one borrower may not repay, and you could lose €500. The amount may wipe out much of the interest you've earned on the other loans. That's why you should invest through platforms with strict vetting procedures and a proven repayment history.

A lower default rate will leave you more confident about protecting your principal and earning consistent returns.

Who Gets Past the Platform's Velvet Rope?

This is obvious, but most investors still miss out. The platform's screening process determines how well it can filter out risky applicants and protect your investment.

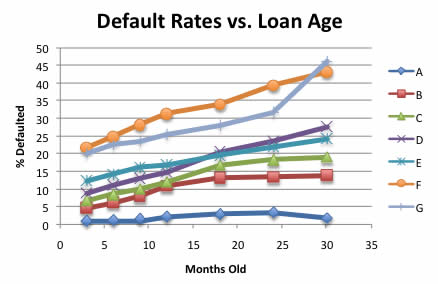

Default rates versus loan age

A reliable platform will assess borrowers based on credit history and income verification. Some go as far as checking employment stability and past repayment behavior. Your chances of facing defaults increase significantly if there's no rigorous vetting system.

Be sure to verify transparency levels. A trustworthy platform should give investors access to borrower profiles and risk scores based on historical loan performance. These insights eliminate blind guesses. You'll see who you're lending to and how loans similar to theirs have performed.

Many platforms rank loan quality using risk grades or borrower categories. A Grade A borrower might offer 8% annual returns with minimal risk, while a Grade D borrower could promise 18% returns but with a much higher chance of default. You must know how to balance potential returns against acceptable risk.

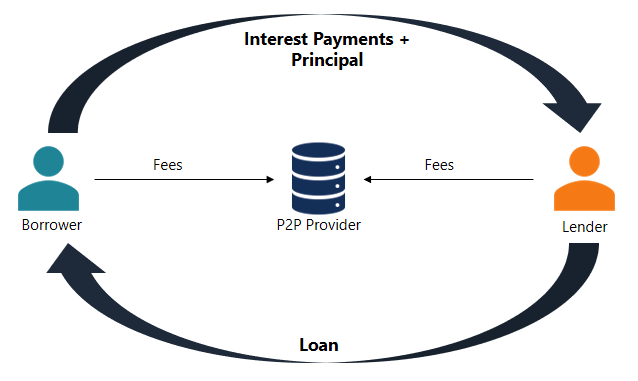

How Does the Platform Turn Risk into Reward on Paper?

You need to understand what kind of returns to expect before putting your money into a P2P lending platform. Savvy investors also find out how they're calculated.

How lenders earn

Some crowdlending platforms offer fixed interest rates, while others provide estimates that can fluctuate based on borrower performance. Fixed returns give more predictability and are often paid monthly. Investors get a steady stream of passive income. If you invest €1,000 in a loan offering 14% annual interest, you could earn around €140 over 12 months. Moreover, you'll start receiving interest in just 30 days.

What's the Backup Plan If a Borrower Stops Paying?

This is an obvious question that every smart investor should ask before jumping into P2P lending. The best platforms have real recovery systems in place. These range from chasing payments to using legal action or third-party collectors. They don't leave you hanging.

Be sure to ask whether the loans are backed by built-in safety nets like insurance or reserve funds. Peace of mind is part of the return. Therefore, always opt for platforms that are transparent about their default process.

Is My Investment Stored Separately or Combined with Everyone Else's?

The answer to this question will tell you whether a platform values investor trust and takes risk seriously. A segregated account essentially means your funds are kept separate from the platform's operational accounts. Your investments will be fortified if the platform faces financial trouble.

Also, inquire whether the platform has a reserve or protection fund. Some sites set aside a pool of money to partially cover lender losses when borrowers default. This safety net cushions the blow of missed repayments.

How Far Can I Spread My Risk?

Nothing screams rookie than putting all your money into one loan. Smart investors spread their funds across multiple loans to reduce risk. One borrower's slip shouldn't sink the whole ship.

The best P2P platforms make this easy with auto-diversification tools. 8lends takes it a step further. It offers variety and thrives on it. You can invest across vast industries and back real SMEs across Europe.

Here are some of the projects:

- Consumer Loans: 8lends’ consumer loans project in Bulgaria offers a short 8-month term with returns of up to 21.5%. There's just €27,055 left to fund.

- Smart Italia: This project promises returns of 15.7%. It also boasts strong asset backing and a credit rating of 9/10.

- Wine Way Phase II: This almost fully subscribed project offers 14.7% returns over 16 months. It has a 56% loan-to-value (LTV) ratio and a 7/10 risk score.

- Wine Way Stage 4: Most investors opted for this program due to its 13.9% yield and monthly payouts. It also has wine stock as collateral and a flawless credit score of 10/10.

- Green Energy: This Italy-based project offers a 15.7% return (plus a 1% bonus) on a 12-month term. It's secured by assets and backed by a 9/10-rated company with a 36% LTV.

- eStock Projects: The eStock Projects in Austria guarantee 14.9% interest, 14-month terms, and heavy collateral backing. This investment also comes with the confidence of an 8/10 risk rating.

Who's Really In Charge?

P2P lending platforms are using AI to enable faster loan approvals and real-time risk assessments. This technology is also aiding smoother investor experiences. Unfortunately, algorithms can’t stand market turbulence. That’s why you have to look beyond the tech and examine who’s steering the platform.

Does the management team have experience in risk analysis or lending? Have they navigated volatile markets before? Also, verify whether the leadership team understands when to override algorithms and adapt to new market realities.

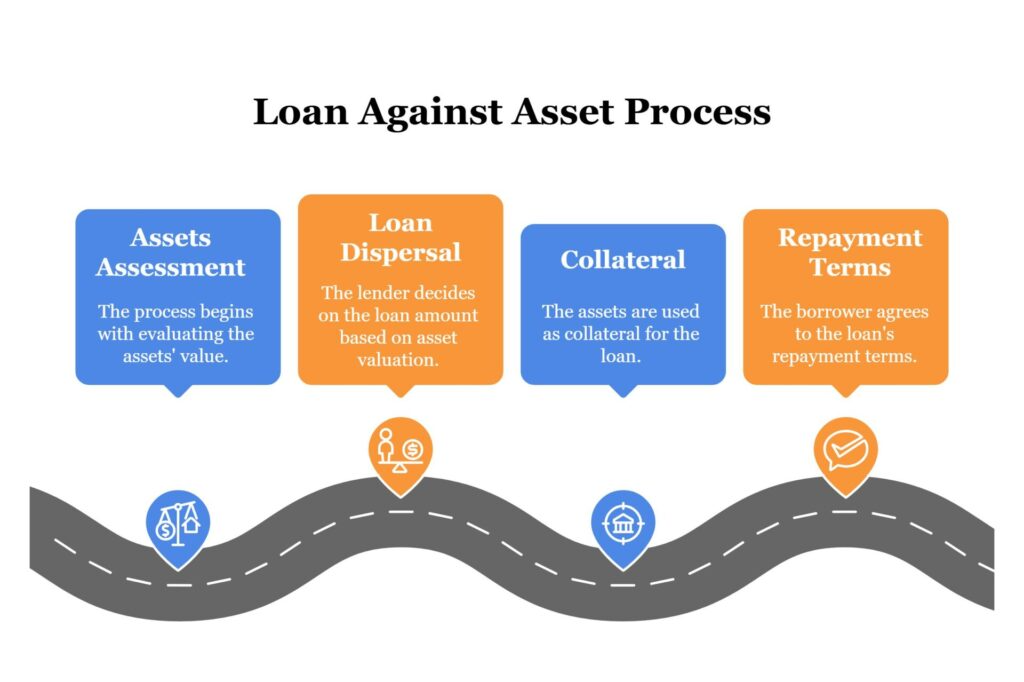

Is There Something Tangible to Recover If a Borrower Defaults?

Why would you skydive without a parachute? You're betting purely on trust if you don't have collateral to cushion a fall. So, verify whether the loans are backed by anything real before you invest in any P2P platform.

The collateral-based lending process

Secured loans use collateral as a safety net. The platform can seize and sell the asset to recover funds if the borrower defaults. It's one of the smartest ways to reduce risk and protect your money. Unsecured loans offer no such fallback. If the borrower disappears, so might your investment. That's why serious investors often lean toward platforms that prioritize asset-backed lending.

Want a platform that treats your money with the same caution and clarity you do? 8lends offers high-yield, commission-free, collateral-backed investment opportunities vetted by real experts – not just algorithms.