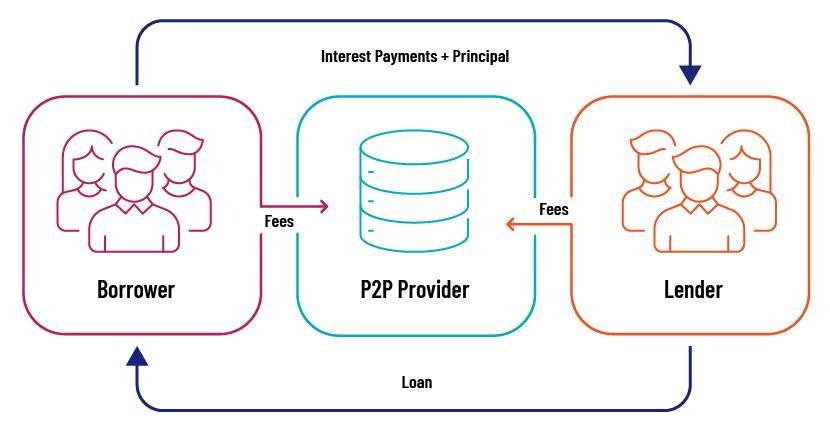

How It Works the P2P Context

This is the process of changing the terms of existing credit to accommodate a shift in the borrower’s financial condition or to react to external economic developments. It’s usually a last resort when defaulting on credit seems inevitable. Unlike a typical default, which may lead to a complete loss of capital, agreement do-overs help borrowers avoid default, thereby limiting losses for the platform and its investors.

Restructuring in P2P lending can take many forms. These include extending the repayment period, reducing the interest rate, deferring payment, or even waiving part of the principal in some cases.

We can consider loan redo’s a positive thing because when default is inevitable, new agreements ensure that instead of losing the entire pie, the lender loses just a piece of it. This usually aims to align the repayment cycle with the borrower’s current cash flow to create some breathing room under challenging financial times.

Why Restructuring Occurs in P2P

As we’ve discussed, many diverse and valid reasons can trigger the need to restructure a P2P debt contract.

Some of the key reasons are:

Borrower Financial Distress

Unexpected personal or business financial setbacks are among the most common reasons for having to resign the repayments schedule. When a borrower’s earnings decrease, perhaps due to unforeseen medical expenses or lower business income, it impairs their ability to satisfy the original terms.

Instead of letting the debt go to default, where both the resource and the investor risk losing the full amount, most P2P apps give borrowers a chance to renegotiate. By renegotiating the plan, platforms attempt to create a sustainable path for recovery that is beneficial for all parties in the long run.

Economic and Market Conditions

Shifts in economic conditions, like recessions, acute industry turnarounds, or broad financial crises, may increase default risks indiscriminately. Individual applicants who earlier appeared creditworthy might experience financial difficulties that may make them unable to meet their repayment obligations.

Crowdlending apps anticipate these systemic patterns, which is why many of them proactively offer new plans to mitigate systemic risk. By adjusting terms before a loan goes into default, crowdlending platforms can preserve a portfolio’s balance and stabilize investor returns.

Risk Management

P2P lending platforms are not passive intermediaries; they proactively monitor applicants’ performance and overall portfolio risk. Advanced analytics and credit scoring models help identify impending distress before it gets severe. When the initial warnings indicate a borrower has a high chance of defaulting soon, apps can initiate new negotiations.

Not only does it save the loan taker from defaulting, but it also preserves the investors' capital by getting back a portion of the guaranteed returns instead of suffering a complete loss. Overall, a new deal is a risk management tool that increases the overall portfolio tenacity.

A platform like 8lends uses real-time analytics and borrower monitoring tools to detect early signs of financial distress—triggering timely interventions such as redoing contracts before default becomes likely. The emphasis is on preserving long-term value and maintaining portfolio stability with collateral-backed loans and high commissions for investors while giving reliable credit candidates an opportunity to show their promise.

Regulatory and Market Pressures

In a few instances, regulatory guidelines or investor demands might compel apps to adopt credit repayment practices. More stringent transparency standards and changing industry norms imply that resources need to have a proactive risk management approach to uphold trust and remain compliant.

By being willing to collaborate with borrowers and modify terms as and when required, P2P platforms align themselves with best practices becoming expected in the digital finance arena.

When Restructuring Takes Place

Loan restructuring isn't a common financial practice; it is the last option in instances where there is clear evidence of financial stress or market volatility. The following are some instances where redoing the contract may be necessary:

- Overdue payments: When a debtor fails to make payments as agreed, sites might view do-overs as a better option than delinquency. They thus avoid the domino effect of defaults that can derail the entire portfolio.

- Financial fall: Detection tools can spot dramatic declines in a borrower’s credit score, income, or debt-to-income ratio. As these indicators worsen, restructuring can be an optimal way to synchronize the debt with the debtor’s current financial condition.

- Economic recessions: In cases of macroeconomic distress, such as a recession or industry decline, websites can offer altering the debt payback to even non-defaulting debtors. Preventive action will avoid defaults bound to occur by altering terms before the borrower reaches a breaking point.

- Borrower request: In other cases, a borrower may take the initiative to request term renegotiation, anticipating future financial troubles. In such a scenario, reworking loan agreements can benefit both parties by allowing the debtor to stay in line while reducing the likelihood of default.

The System in P2P Lending: What Gets Restructured?

Platforms can use different approaches to redo the repayment plan before they default, but below here the main aspects resources adjust as they restructure a loan:

Extended Repayment Terms

Extending the repayment period is one of the most common restructuring measures. Extending the length of the contract lowers the monthly premium, which eases the burden on borrowers experiencing financial hardships like temporary liquidity shortages.

Although the total paid in interest over the long term may be higher, the smaller monthly obligation will lower the risk of default in the short term.

Interest Rate Adjustments

Decreasing the interest rate also provides great relief to the debtors. It lowers the monthly installment and reduces the cost of credit in the long run. However, it may also lead to lower returns for the investors. That’s why this option only comes into play when the other option is an outright default

Payment Deferrals

In particular circumstances, crowdlending platforms might opt for delayed payment for a short duration. Such relief from the short-term payment can be invaluable if the debtor is overcoming short-term adversity like an emergency medical or business expense.

The payment grace period gives the debtor the freedom to get back on track without any penalties.

Partial Principal Forgiveness

Although it’s less common, partial forgiveness of principal can be a solution where a debtor’s long-term financial condition looks grim.

Partially forgiving the principal amount creates room for a more sustainable loan repayment plan. However, this option is not that common, and platforms only use it in cases of extreme financial distress.

How Loan Restructuring Impacts Investors and P2P Lending Platforms

For investors, redoing debt payback is double-edged. While a replanned loan can rescue a portion of the expected returns that an investor would otherwise forfeit in the event of default, restructuring most likely involves a riskier profile. For example, investors may have to agree to lower interest rates or longer tenors that delay returns.

However, P2P platforms view restructuring as a risk-management tool that keeps their whole portfolio healthy. By renegotiating terms, platforms can prevent the domino effect of mass defaults, keep investors' faith, and shield their reputations in a competitive market.

Communication should occur during restructuring. Open reports on the altered terms and the repayer’s continued attempt at financial rehabilitation are crucial to maintaining investors' trust. In most cases, platforms also provide thorough documentation and examination of data to justify the adjustment.

Final Thoughts

P2P loan restructuring is an essential risk management technique during a time of rapid innovation and shifting economic hurdles. Whatever its cause, be it borrower crisis, economic slowdowns, or risk-conscious management efforts on the platform's part, restructuring is a lifeline that helps sustain investor value and allows financial recovery.

Platforms like 8lends are leading the way in responsible P2P lending by treating restructuring not as failure, but as strategy. Through early detection systems, transparent borrower communication, and flexible loan terms, 8lends helps minimize losses and preserve value—making it a smart choice for investors seeking resilience in unpredictable markets.