The Deceptive Simplicity of France's Basic Profit Formula

It is not uncommon for a blockchain investor to be easily misled by the seemingly simple format of the French tax system. Frankly, this Profit = Sale Proceeds - Acquisition Cost – Transaction cost equation masks some intricate complexities that are only uncovered in real-world applications.

In reality, the actual equation looks like: (Selling Price – Overall Portfolio Cost Basis) × (Sale Amount / Overall Portfolio Value). This is because the republic has a holdings-based approach to computing gains.

This investments-based approach makes France’s system different from most countries' formulas, where they track individual sales rather than the entire portfolio. This fact alone threatens to have a significant impact on how much tax you pay.

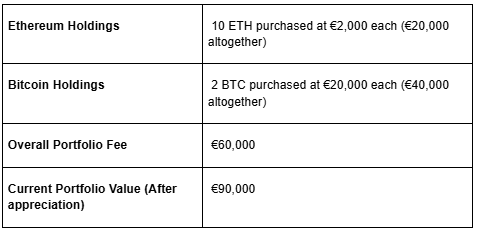

For investors, this means that a single virtual cash sale triggers a portfolio-wide computation. For instance, a portfolio holding with the following virtual currencies has an overall holdings value of €90K.

From this portfolio, if 1 Bitcoin is sold at €35K, instead of computing the revenue based on the profit made on that 1 satoshi, the computation considers the overall value of the holdings using this equation: Cost Basis (EUR) = Sale price – (total acquisition costs × [sale price/total investments value]).

What you then have is €35,000 - (€60,000 × [€35,000/€90,000]) = €35,000 - €23,333 = €11,667.

The aggregate gain for that operation subject to government payment then becomes €11,667, reflecting your entire holdings performance rather than your individual exchange.

FIFO Implementation: A Chronological Approach

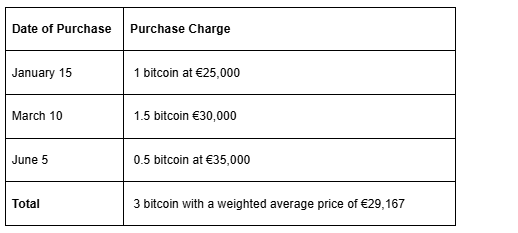

Another important consideration in the French budgetary computation is the First-in-First-Out (FIFO) concept. This assumes that every blockchain sale follows a chronological order based on its purchase date and time. This is applied when selling the same type of virtual cash.

Let’s take the table of purchase below, for example,

When you eventually sell 2 satoshis at €40,000 each on September 20th, the equation using the FIFO concept becomes:

The balance of crypto purchased on March 10 and June 5 retains their value, which will be used when computing government dues in the future.

The remaining 1 satoshi (purchased March 10 at €30K) and 0.5 satoshi (purchased June 5 at €35K) maintain their original toll basis for future computations.

Duties Integration

Another nuanced consideration that may bring about additional dues to the state if not put into consideration is operation tolls. However, if tracked properly and according to set DGFiP guidelines, transaction tolls could help reduce state debt on your gains.

Here are two important categories of tolls that you must not overlook in your computation of government debt.

To apply these tolls, use this equation:

Profit = Sale Proceeds - (Acquisition Cost + Acquisition Charges) - (Sale Charges + Transfer Charges)

For instance, if you’ve made a bitcoin transaction as follows:

- Purchases: €30,000 + €150 transaction fee + €25 network fee = €30,175 sum charges.

- Vending: €45,000 - €225 transaction fee - €30 network fee = €44,745 net proceeds

Hence, your yield will be €14,570 (€44,745 - €30,175). Using the right equation will save you from overstating your yield by €430. This would have resulted in €129 excess tax using the 30% flat rate option.

Accuracy is everything when computing virtual money returns in the republic. One overlooked conversion rate or untracked charge might change your liability more than you think.

That’s why many investors and professionals trust 8lends. As a global compliance and risk management provider, 8lends helps users document, compute, and audit their digital asset operations with precision. With its automated record-keeping and compliance monitoring tools, it’s a certainty that every tariff, purchase, and conversion is accounted for correctly.

Multi-Currency Conversion Complexities

When dealing with multicurrency situations, especially with international wallets that require rate conversions, it is always advisable to document the current exchange rate at the time of the transaction. It is important to consider these critical requirements in these situations.

- Always keep a consistent rate source all year round

- Account for currency conversion spread expenses.

- Use the transaction rates at the exact operation timestamps

- Document all the rate sources used in your calculation

For instance, if the conversion rate was EUR/USD = 0.85 when you purchased $3K worth for 2ETH on Coinbase, your computation should be as follows:

Virtual-for-Virtual Mathematics

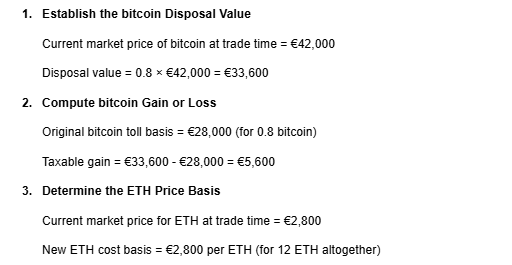

Another complex situation often arises for active traders who engage in significant virtual-to-virtual trades. This is because of the government’s categorization of these deals as disposal events relevant to state revenue, which requires traders to declare the yield or loss status of these operations.

For instance, if you’ve traded 0.8 satoshi for 12 ETH, here is a stepwise method for counting your gains out of which you’ll have to pay the state.

The gain generated is €5,600 satoshi on which duties must be paid, regardless of future ETH performance.

Partial Disposal Precision

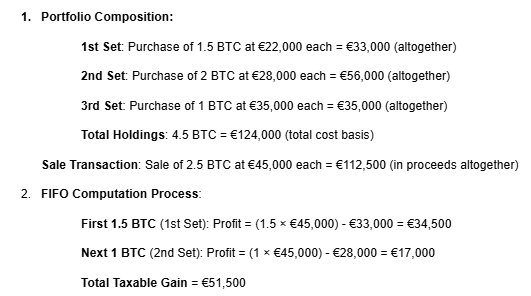

The fiscal system combines the FIFO principle and the portfolio approach to create another challenge when owners sell a portion of their virtual wallet holdings. This requires some complex methods to compute precisely. Here is how to determine your total holdings and overall gains you’ll have to pay on.

Your remaining holdings is now 1 BTC from 2nd Set (charge basis €28K) + 1 BTC from 3rd Set (charge basis €35K)

Professional Trading Classification Impact

Wallet owners with a significant portion of their income coming from blockchain trading are often categorized as professional traders under the French revenue system. These traders are also classified under France’s BNC (Bénéfices Non Commerciaux) tax system, where a different computation of duties applies. This number crunching may substantially alter their fiscal obligation if not done with the carefulness it deserves.

Under the BNC regime, professional traders determine the gains they’ll have to pay on using the equation:

Taxable gains = Total Trading Revenues – Business Expenses – BNC Allowance

This means that they subtract their business expenses, such as equipment, education expenses, and software, along with BNC allowance (may be as much as 34% under the micro-BNC regime), from all virtual cash purchases.

This often proves advantageous for professional traders with significant monetary benefits relative to capital gain computation.

Conclusion

In all, the French government’s crypto yield arithmetic might look elementary at first glance, but a closer look at its application opens up some complex nuances that investors should thoroughly understand. Its First-in-first-out digital currency debt concept added to its portfolio can result in significantly piling on obligation if not considered critically.

Also, situations like multicurrency transactions with exchange implications present some pitfalls if the exact currency conversion rate at the transaction timestamp is not used in the math. However, it does offer some state debt benefits to professional traders under the BNC regime, where traders subtract business expenses and up to 34% BNC allowance from total digital currency revenues.

Ultimately, you need a detailed knowledge of the crypto formula and calculation to successfully execute your strategies and avoid unnecessary mistakes in calculating their monetary obligations to the state.

France’s virtual cash profit calculation system may look simple, but its portfolio-based and FIFO mechanisms can easily lead to errors that cost you real money. 8lends helps investors, traders, and organizations simplify this complexity with automated compliance solutions that turn detailed reporting into a seamless process. From transaction tracking to holdings reconciliation, 8lends makes accuracy effortless.