What We Mean by “Borrower Education”

We’re not talking about making people sit through boring lectures or take exams. Borrower education can be as simple as helping someone understand how interest works, what happens if they miss a payment, or how to spot a loan scam. It’s about giving people the tools and knowledge to borrow responsibly.

Think financial literacy, but with a lending twist. It might be delivered through blog posts, in-app explainers, interactive guides, and short videos – you name it. It’s not about making borrowers into finance experts. It’s about making sure they know enough to make good choices, and not end up in hot water.

The Problem With Uninformed Borrowers

When people don’t fully understand what they’re signing up for, things tend to go wrong. And it happens quickly. When borrowers do not have enough education on loans, they sometimes end up taking loans they can't actually afford. They might also miss payments because they didn’t understand the due dates and then they get hit with fees and penalties they didn’t even know existed.

Unfortunately, some of them end up damaging their credit without realizing how long it takes to rebuild. And when this happens, it’s not just the borrower who suffers. The platform takes a hit too. Defaults go up. Recovery gets messier. Customer service lines start blowing up. And worst of all, trust in the platform takes a nosedive. Education upfront could’ve prevented that.

There are currently platforms where people have more opportunities than ever before to prove they are creditworthy, in particular the modern-day crowdlending platforms, where people who never could’ve gotten a loan before now have opportunities. One such platform is 8lends.

Education Builds trust

Here’s a truth bomb: most people are naturally suspicious when it comes to borrowing money online. And can you blame them? Between sketchy lenders, hidden fees, and fine print nightmares, the average person is right to be cautious.

So, if a platform actually takes the time to educate its users? That stands out. It tells borrowers, “Hey, we’re not just here to make a quick buck. We actually want you to succeed.” It makes users more likely to come back. And it even turns them into advocates who recommend your platform to friends. Trust isn’t something you can hack. You earn it. And borrower education is one of the best ways to do just that.

Better Education Means Fewer Defaults

Let’s talk about the money side of this for a second. Default rates are like the blood pressure of any lending platform. If they’re too high, it means something’s not right. Well, guess what? Educated borrowers default less. Why? Because they understand what they’re agreeing to and they are able to plan better for repayments. They are also able to avoid borrowing more than they need.

Most of them also have the tendency to reach out for help when they hit trouble instead of ghosting the lender. Platforms that invest in borrower education often see steadier repayment behavior. That means lower risk for investors or balance sheet managers, and better long-term viability. There’s actually data to back this up, too. The World Bank has highlighted that financial education programs in lending environments lead to improved repayment rates and lower delinquency.

Regulatory Compliance

Depending on where your platform operates, rules may exist to disclose matters. Interest rates, total loan costs, risk warnings, and things like that. But going above the bare minimum? That’s where smart platforms stand out. By offering solid borrower education, you’re less likely to get caught in legal grey zones. You gain better defense if a borrower ever complains or tries to challenge the fairness of their loan terms.

In some regions, regulators are even starting to require borrower education for certain types of products. Getting ahead of that curve isn’t just smart, it could save you a ton of trouble down the line.

Borrowers Become Smarter Users Over Time

Imagine this: a first-time borrower comes to your platform. Maybe they’re nervous. Maybe they don’t even know what an APR is. But they read your explainer, watch a short video, and they get it. Next time they borrow, they make smarter choices. They borrow just what they need. They pick better terms. They repay on time.

Eventually, they might even start investing on your platform too. That’s how education creates power users, people who stick with your product and use it more responsibly. If you want a loyal customer base, start by teaching people how to use your product well.

It Doesn’t Have to Be Complicated or Boring

When we talk about education, people think it means school-style lectures and long paragraphs of text. But that’s not what we’re going for here.

Modern borrower education can be fun, quick, and visual:

- Use short videos that explain key concepts in under 2 minutes

- Break things down with simple graphics and examples

- Add tooltips in your app that pop up when users hover over confusing terms

- Send out helpful reminders before payments are due

A little creativity goes a long way. You don’t need a PhD to help people understand loans. You just need to speak their language.

Borrower Education Translates to Better Platform Reputation

Ever read online reviews of lending platforms? They can be brutal. But when borrowers feel informed and respected, they’re more likely to leave good reviews. That builds your reputation and makes customer acquisition cheaper. It’s basically free marketing. A well-educated borrower is less likely to call your platform “a scam” on social media. And in this day and age, that’s priceless.

Here’s What Good Borrower Education Might Cover

Wondering what topics to focus on? Here’s a quick list platforms include:

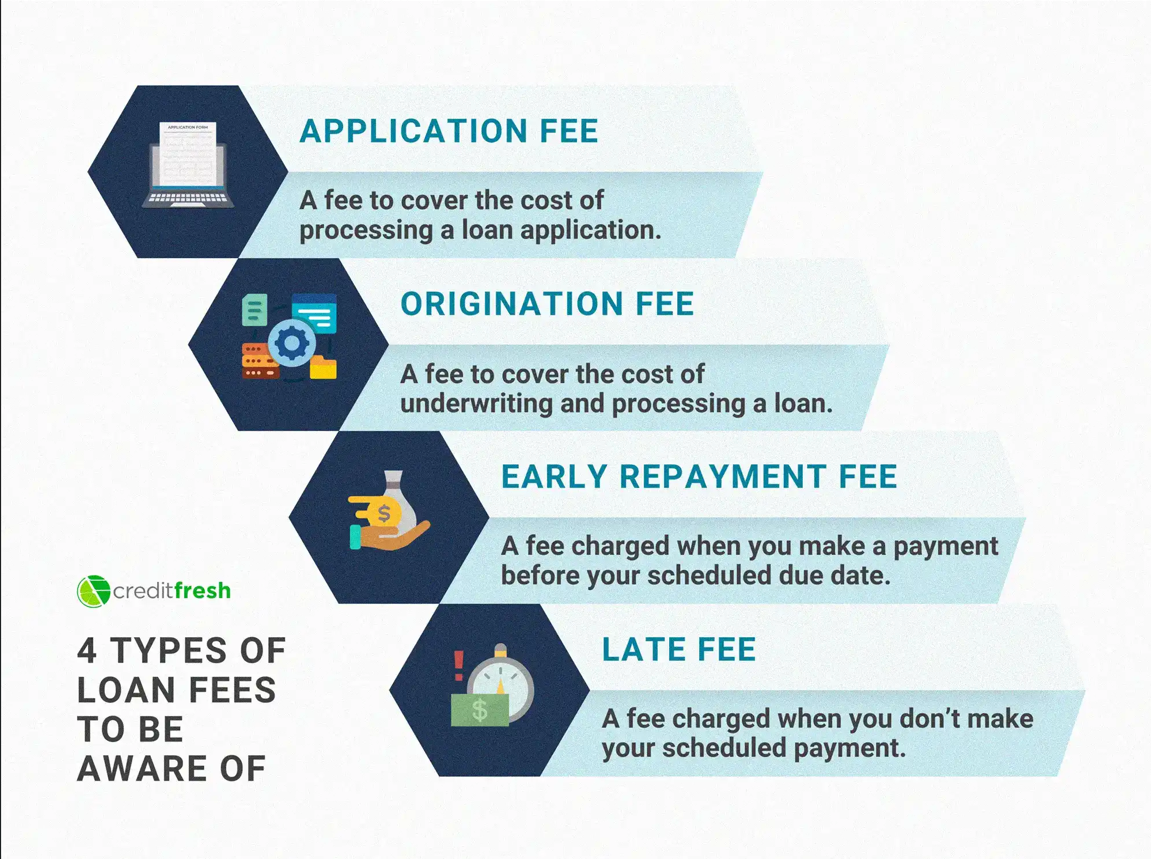

- Interest increases

- APR vs flat rates

- Missed payments

- Borrowing limits

- Loan terms and cost

- Fake lending offers or scams

If you can break these down in simple, relatable ways, you’re already miles ahead of many platforms out there.

The Human Side of Lending

People often forget: real people apply for loans, of all walks of life – whether they’re trying to fix their car so they can keep working, a parent paying school fees, or a young man chasing a dream. If we treat borrowers like they’re just numbers on a spreadsheet, we miss the point. Borrower education is one way to show respect and care and keep borrowers around longer.

Final Thoughts

Borrower education isn’t something that’s “nice to have.” It’s a need-to-have. It makes borrowing safer, smarter, and more sustainable for everyone involved.Platforms that invest in educating their users aren’t just doing a good thing; they’re building better businesses. Fewer defaults. Better reviews. Higher trust. It all adds up.

While participating in lending platforms, or thinking of building one, start putting borrower education front and center – teaching and empowering people. As an applicant, always keep learning. Even if the first step is just understanding your next loan a little better, that’s still a win.

If you are interested in educating yourself on the freshest opportunities the modern day has to offer, or you wish to profit off of the lucrative interest, 8lends goes out of its way to educate users on all the essentials of its crowdlending platform.