What Are Loan Grades in P2P Lending?

LGs can be described as risk scores given and used by P2P lending websites to classify debtor credit profiles. Most of these platforms use proprietary algorithms to give individual loan applications a credit rating based on a series of standards, such as:

- credit history

- income levels at application

- debt-to-income proportion

- alternative data like employment and education.

An advanced grade (e.g., "A" or "1") usually indicates a credit-worthy debtor with favorable financial circumstances and minimal default risk. Lower scores (e.g., "F" or "G") can be used to signify higher risk, perhaps because of lower credit scores, unstable incomes, or a heavy debt burden. LGs give stakeholders an at-a-glance risk summary of significant value, which helps with portfolio balancing and estimating future profits.

Over the last few years, the grading mechanism has evolved from traditional credit scoring methods to sophisticated techniques that use machine learning and unconventional data sources.

Sophisticated algorithms often go beyond historical past performance data. They also absorb the most recent borrower behavior. This longer-term approach enables frequent assessment updates on the basis of the newest financial scenario of each debtor.

Crowdlending platforms like 8lends present loan grades with clear, grade‑level risk/return context and portfolio filters, helping investors compare listings and build allocations that align with their risk tolerance—without turning the article into a product pitch.

The Gears That Determine Loan Grades in P2P Crowdfunding

Behind each evaluation is a thorough assessment process that blends automated data analysis and human judgment. Most of these sites use vast data sets of financial metrics to assign LGs.

Although many platforms don’t openly disclose all the metrics they use to assess loans, here’s a brief overview of some of the data points crowdlending platforms typically use to determine and assign LG:

- Credit score and history: Historical payment behavior, utilization, and default history are vital in the initial assessment.

- Income and work metrics: Regular income streams and long-term employment are likely to result in higher grades because they’re stellar indicators of the ability to repay any advanced credit facility.

- Debt-to-income ratio: Cross-referencing debt obligations against disposable income helps P2P lending platforms quantify global financial health and risk exposure.

- Alternative data: Some platforms also improve their loan grading models by using non-traditional data from sources as diverse as social media behaviors, digital payment history, and even geospatial patterns.

These platforms input these and other signals into machine learning models that can scour through and learn from large datasets in record time. For example, research and industry tests have confirmed that models developed using methods like LightGBM and feature selection techniques can perform default forecasting actions at a super-accurate level.

Such models continuously update their forecasts as more borrower performance data becomes available. This real-time data exchange leads to dynamic grading systems that evolve as they learn from data about evolving economics and changing debtor profiles.

Underwriters generally perform a secondary check to uncover nuances that automated tools may otherwise miss. The human touch places outlier events, such as the temporary loss of a job or a single financial setback, into context to ensure they don’t lead to unintended data distortion. A combination of quantitative and qualitative analysis is at the heart of what makes LG accurate and timely throughout a loan's term.

The Art of Using P2P Lending Loan Grades to Balance Risk and Return

P2P lending is mostly a risk-return trade-off. Loan grades clarify the risk-to-return reward. Here’s a simple way to understand the grades and the inherent risk-reward trade-offs to each grade:

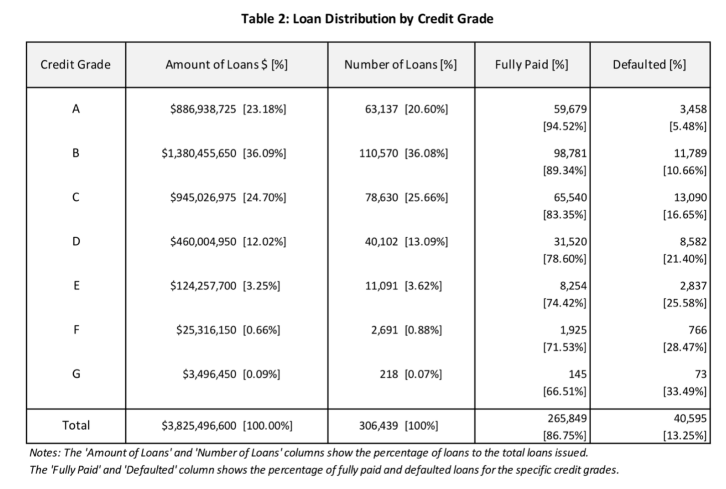

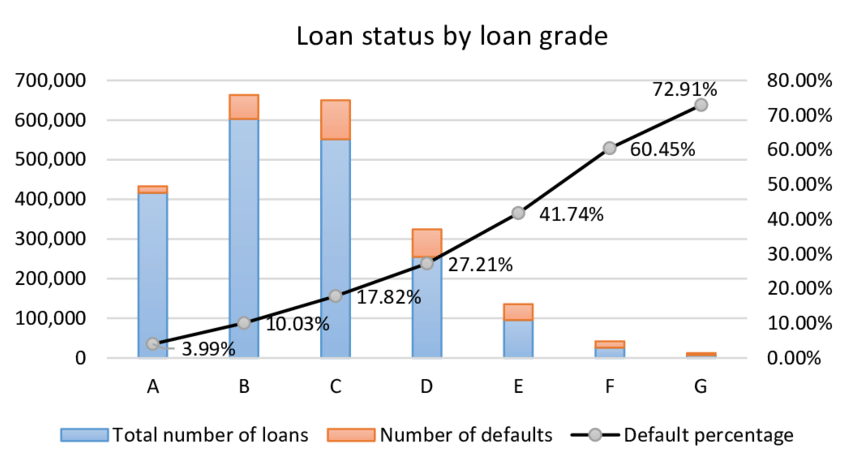

- More grades = less default, less return: High-grade loans (grades A or 1) have lower default rates, typically below 3%. Because borrowers in this classification are highly creditworthy, the interest rate quoted is comparatively low. Stakeholders on these loans will receive more stable and secure returns, but the trade-off is reduced yield due to the lower risk premium.

- Lower grades = higher risk, higher return: On the other side of the spectrum are lower-score loans (e.g., F or G) that carry greater defaults. Historically, default rates on such loans can be 10% or higher. In return for the greater liability, these loans typically yield significantly higher interest and good profits when a debtor repays the loan in full. While the higher yields may be extremely tempting, the trade-off is a higher potential for losses should a debtor default.

LG's default predictability comes from an expanding body of evidence that has consistently demonstrated a connection between lower scores and a higher incidence of default.

Stakeholders should know about this spectrum because it's essential to building a diversified portfolio that matches a well-considered risk tolerance. Diversifying investments across various grades is another outstanding way to defray the effects of defaults while maximizing the overall yield potential.

Advantages and Limitations of Loan Grades

Like most things, loan scoring has inherent pros and cons.

Benefits

Loan scoring simplifies the advanced task of risk evaluation by condensing varied financial data into a single, straightforward, and understandable measure. These grades are invaluable to retail investors who do not have the time or expertise to examine every feature of a debtor's profile. Loan grading ensures stakeholders can tailor their investment portfolio to match their risk-profit appetite based on investment goals.

Limitations

Although none of us should undervalue their informative usefulness, scoring is only a snapshot, not the complete picture!

Since loan grading models are proprietary and every platform is free to use custom models and datasets, scoring may vary from platform to platform. For example, an ‘A grade’ on one P2P lending platform may differ from an “A grade’ on a competing platform.

Since loan grading also relies on historical financial data and algorithmic projects, an evaluation may fail to capture sudden market shifts or surprise personal financial shocks. Thus, investors should not rely on scoring only. Instead, they should consider it a foundation they can supplement with personal due diligence.

Using Loan Grades in Real-Life P2P Lending Applications

Let’s turn our attention to a few key ways to use loan grades as part of an informed P2P lending strategy:

- Diversification by loan grades: Instead of investing everything in prime-rated loans, diversify across a portfolio of grades to achieve a balanced return profile. The stable, lower-risk loans can provide stability, while selectively investing a portion of your capital in riskier loans can add to overall portfolio return.

- Periodic portfolio rebalancing and review: Since most P2P crowdfunding platforms periodically update loan grades to match a borrower’s evolving financial situation, portfolio reviews are non-negotiable. Rebalancing investments according to grade changes can mitigate risks and losses by rebalancing a portfolio to match risk tolerance.

- Augmenting loan grades with additional research: While loan grades are a good lift-off step, it pays to look beyond the grade. Considering in-depth credit reports, borrower accounts, and even broader macroeconomic trends can be a step-above-the-norm way to determine the accuracy of an assigned loan grade. Conducting additional research could involve tracking sector news, assessing platform performance over time, and using qualitative metrics to quantify borrower sentiment.

- Taking advantage of sophisticated tools and analytics: Some third-party research companies and platforms offer analytical dashboards that overlay loan grades over portfolio-level risk metrics, such as estimated default probabilities, Loss Given Default (LGD), and recovery rates. These tools may offer a better picture of the overall portfolio's risk-return profile.

Conclusion

Evaluations are a valuable asset in P2P lending because they give investors a vital and usable snapshot of profit and liability. Understanding how these lending platforms assign these assessments, from well-established credit measurements to cutting-edge machine learning, can make it easier to create a sustainably profitable investment portfolio.

Platforms like 8lends are already putting these principles into action—offering real-time grading models, transparent borrower data, and tools that help investors diversify intelligently across risk tiers. Whether you're a first-time lender or refining a seasoned portfolio, having access to grade-aware tools makes all the difference.