Plot twist, your friend vanishes into thin air without paying back.

P2P lending is rising as a compelling competitor to the banking system of old, by connecting individual parties directly, usually through an online platform. But when a credit holder fails to make good on the loan as agreed, it triggers a chain of recovery efforts. Here, we explore what happens when a person defaults in such a scenario, what lenders can expect, and how the host typically handles recovery.

P2P Lending Defaults

A default means the P2P borrower either missed payments or was unable to pay off the loan altogether. Each platform has its own way of defining when a loan goes into default.

- Late Payment: 1-30 days overdue

- Delinquent: 30 days overdue

- Default: More than 90 days without resolution

Handling Early Warning Signs

Before a loan reaches the default stage, most platforms take proactive steps such as:

- Payment Reminders: Borrowers receive automated and manual reminders, emails, texts, or app notifications once a payment is missed.

- Grace Periods: Many platforms offer a grace period where the borrower can pay without penalty.

- Re-negotiation Attempts: Some platforms may reach out to discuss restructuring or repayment plans, especially if the credit holder established a reputable track record.

During this period, they gain the opportunity to redeem themselves and propose alternative arrangements.

How Recovery Works

When a default declaration is posted on the app, it triggers the recovery protocol, which usually goes like so.

A. Collections Process

Once they fail to respond or resolve the delinquency, the app initiates in-house recovery measures or passes the case to an outside debt collection agency, like a bloodhound to sniff out that defaulter.

Collectors are responsible for:

- Contacting the party.

- Attempting to negotiate a settlement or repayment plan.

- Sending reports to the bureaus.

In some cases, borrowers become responsive during this phase and begin repaying either partially or in full.

B. Legal Action

If the collection process doesn’t yield results, the app can entertain legal proceedings, which is mostly common for large loan amounts or repeat defaulters. Lawsuits may involve securing a judgment to garnish wages or seize assets, as well as seeking repayment through collateral if any was involved.

This process is time-consuming and costly, which is why many platforms only take this route in high-value defaults.

Not The Return You Expected

As recovery efforts are underway and hopes are held up for a good outcome, that begs the question of what the creditor deals with and how they are affected by such defaults. Here is what a P2P default on P2P means for creditors.

No More Regular Returns

Monthly payments from the borrower stop, that’s a no-brainer, and the expected interest payments cease along with it. This affects cash flow and projected investment returns.

Updates from the Platform

While the whole situation might be unpleasant, one silver lining in that cloud is that the lender is not kept in the dark, confused as to how they will get their money back. Platforms usually provide a dashboard or loan status tracker showing updates like:

- Late payment

- In collections

- Partial recovery

- Write-off

Potential Recovery

The situation is not completely hopeless because some amount of your money may still be recovered. This, however, depends on numerous contingencies, chief among them the measures for recovery put in place by the app. A lot of apps report recovery rates between 20-80% based on the loan type and recovery procedure.

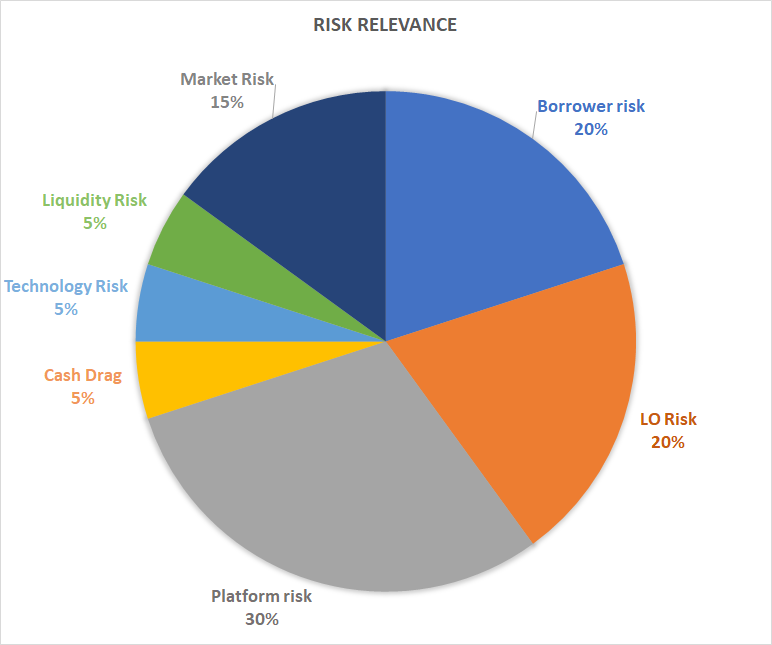

Not all platforms are created equal when it comes to handling risk. 8lends, a Swiss-based crowdlending platform, stands out by combining strong borrower screening, collateral-backed loans, and forward-thinking recovery strategies. 8lends’ progressive credit modeling and risk-spreading mechanisms give lenders more confidence by backing loans shrewdly with collateral and spreading out risk between investors commission-free.

The End Of The Road

When all measures fail though, and the money isn’t recoverable, the apps eventually write it off as a bad loan. In other words, they officially recognize it as uncollectible. For creditors, that means you lose. Essentially, the money is removed from your account and marked as a capital loss.

In some countries, loan losses may be claimed as capital losses or bad debts in taxes. Apps often issue tax statements at the end of the year, indicating which loans were written off. Write-offs are the worst possible outcome, and while these hurt, such risks are part of the game that comes with such investment.

A Lender’s Guide To Managing Risk

After pondering all these circumstances, when it comes to issuing P2P credit, here are some proven strategies for mitigating default losses and possibilities, foolproof means to secure your money.

- Spread out money among credit and applicant types. In classic terms, do not put all your eggs in one basket.

- Study applicants’ backgrounds, their ratings, and past transactions before lending.

- Opt for apps with active collection policies and transparent reporting. We will analyse this a little more later on.

- Don’t invest more than you can afford to lose.

- Re-invest returns into a mix of low and medium-risk loans.

Numbers Don’t Lie

Consider the track record of platforms before choosing one.

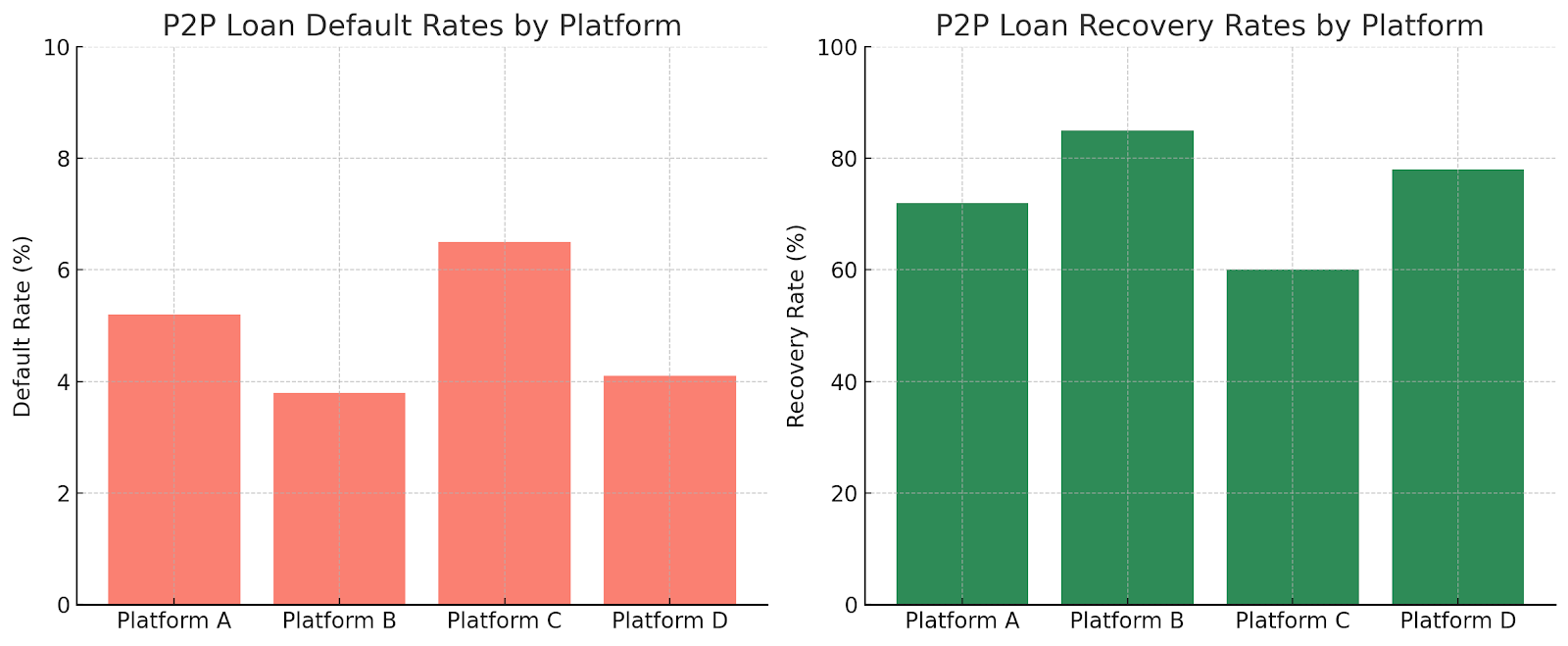

According to industry research, P2P defaults vary between 3.8% and 6.5% based on how the borrower screening process and loan structure go. From a brighter perspective, recovery rates can reach up to 85%, though some outfits recover a paltry 60%, especially in unsecured loan cases.

Platform B has a low default rate (3.8%) and a high recovery rate (85%), suggesting strong borrower screening and aggressive follow-up. In contrast, Platform C sees more frequent ones and weaker collections, often due to a lack of collateral or lax collection procedures.

Armed with the knowledge above, creditors can make shrewder choices.

How Platforms Minimize Defaults

Frequent gaffes like these undermine lender confidence, so having a platform with the necessary security measures and proactive procedures in place to handle them properly is the best way to make sure everyone involved ends up a winner. This is how platforms do that:

Screening

Applicants get vetted through credit checks, income statements, debt-to-income analysis, and bank account review usually. Only borrowers who meet certain criteria are approved.

Risk-Based Interest Sums

Those that are riskier have to pay a premium.

Loan Diversification Tools

Most platforms encourage lenders to spread funds across many loans (e.g. N5,000 across 100 borrowers instead of N500,000 to one). This cushions any borrower who fails to repay their debt.

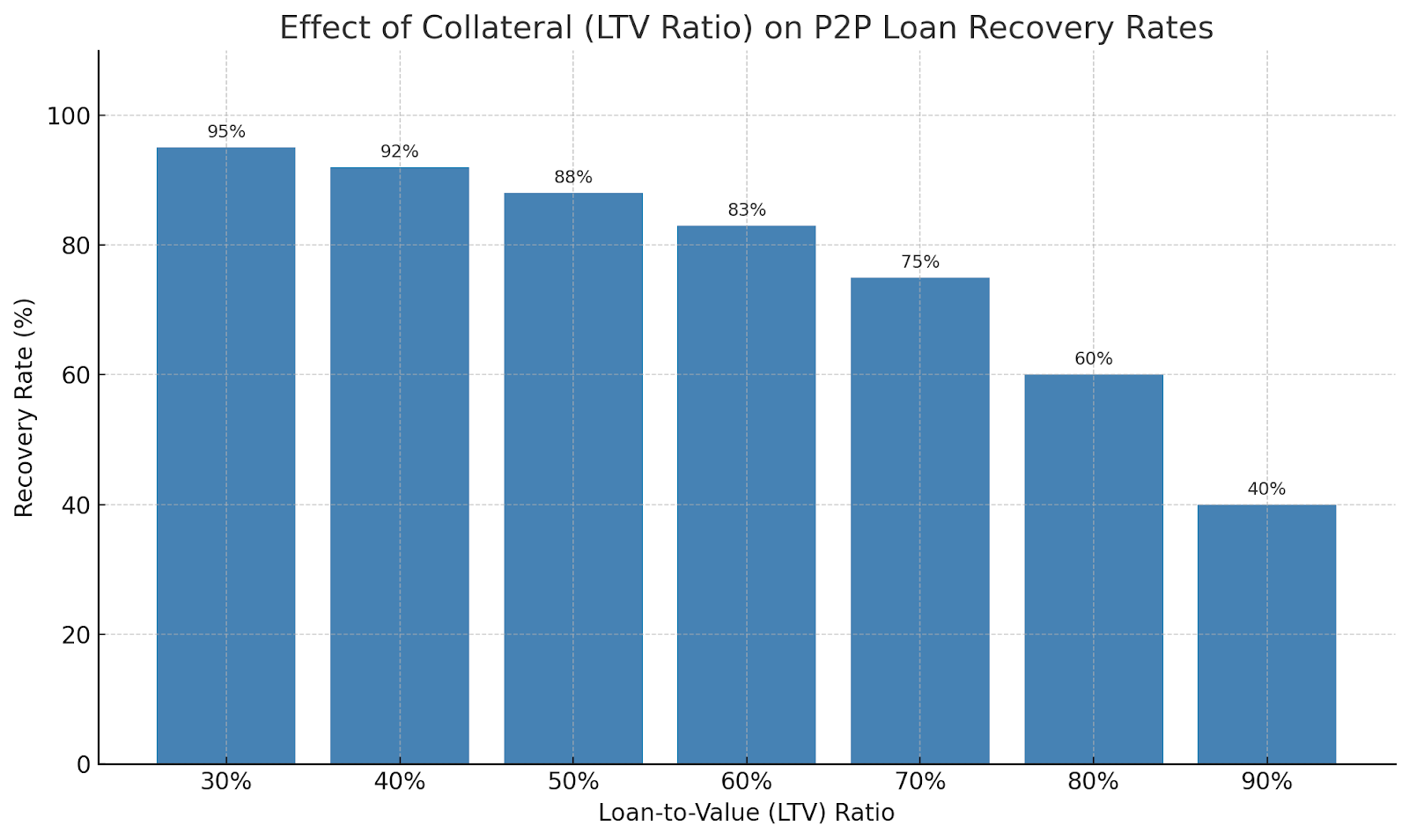

Collateral that could be physical assets like cars or houses or even savings and investments.

This chart illustrates how collateral enhances P2P loan recovery.

When a loan is secured with real-world assets, the platform can legally reclaim and liquidate the collateral in the event of default. LTV ratios typically hover around 60%, protecting lenders even in the case of moderate market fluctuations. The chart shows that recovery likelihood remains high until asset values decline beyond the LTV cushion.

Managing Risk, Maximizing Return

Defaults in P2P lending are inevitable, so it is important to understand the recovery process. Recovery is not guaranteed, but it is often possible, especially on platforms that are well-regulated and proactive.

For borrowers, defaulting may mean damaged credit, persistent collection efforts, and legal trouble. For lenders, it means reassessing strategies, trusting the platform’s recovery system, and being patient through the process. In the end, P2P lending is not just about high returns; it is about balancing opportunity and risk and being prepared for every possible outcome.

If you're looking for a crowdlending platform that takes risk seriously and treats your capital with the care it deserves, check out 8lends. You’ll join a community of smart investors funding real-world businesses with robust protections and powerful returns.