Unpacking the Scam: The Anatomy of a P2P Lending Scam

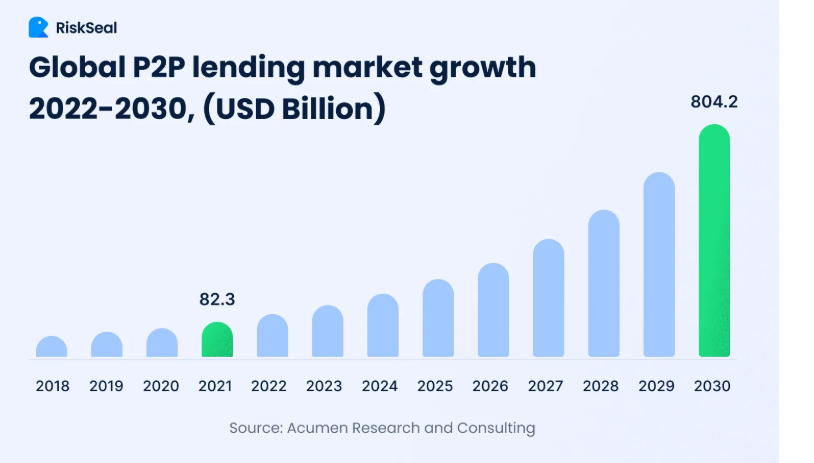

The global P2P crowdlending market will be worth a mind-boggling $804.2 billion by 2030.

A P2P lending scam at its core is an impersonator: it's a spotless digital platform built to lure you into a trap. Let's dissect the most salient components of a P2P lending scam.

The Bait: Seductive Offers

P2P lending scams often use inordinately high rates of return or very enticing loan descriptions as bait. Promises of instant finance and risk-free returns are commonly used to attract prospective victims.

However, real financial markets usually don't offer mouthwatering returns without implied risks. If an offer seems too good to be true, it should immediately earn an extra layer of scrutiny. If you suspect a platform is not as legit as it claims, always proceed with a high degree of caution, hyper-awareness, and scrutiny.

The Disguise: Spoofed Platforms and Credentials

Fake P2P lending platforms are usually very professional and well-designed. They include fake social proof, regulatory credentials, and certificates. Such advanced sites use false security seals and smooth interfaces to mimic legitimate financial services.

Healthy skepticism and verification with regulatory bodies are the secret to peeling away the facade. Always confirm with the regulatory and accrediting bodies whether a P2P lender's credentials are indeed real and not fabricated.

Remember that not everything on the internet is factual, so you mustn't take things at face value, especially where money is involved.

The Social Engineering Techniques

Scammers also apply pressure strategies, threatening action in the present using limited-time opportunities or a perception of urgency. This crosses over into the psychological domain, utilizing our natural willingness to trust and act when presented with apparently dwindling opportunities.

Behavioral finance research and scholarly writing consistently show that such urgency is a characteristic of fraudulent communications. It is one of the oldest tricks in the book and applies to scams that cut across all industries. If someone is rushing you, they are most likely trying to scam you.

The Lethal Misstep: Misuse of Funds and Data

As the scam continues, it will eventually try to trick you into wiring money or sharing sensitive personal information. Once you wire the money or share private information, the site may vanish, leaving you with nothing but promises and potential identity theft repercussions.

Always do a background check before sharing sensitive information online, regardless of how good the platform looks. Remember, recent statistics show that most online scammers may never be caught.

A Deep Dive into Scam Phases: Baiting, Engagement, and Exploitation

Besides the glaring red flags, P2P lending scams typically unfold in three phases: baiting, engagement, and exploitation.

1. Baiting

During the baiting phase, fraudsters craft a message that is both appealing and urgent-sounding.

They employ a persuasive tone coupled with sales copy that typically promises high returns and immediate approval. This attraction is crafted with behavioral finance studies that show how the promise of easy money can overwhelm our otherwise wise instincts.

Research among academics reveals that even experienced P2P investors can fall into these scams if a fake platform uses sleek graphics, social endorsement, and emotional manipulation.

2. Involvement

In the involvement stage, fraudsters have mastered the art of developing trust. They can monitor the signs of a real platform by installing customer support chatbots or even using actors to fake having responsive support.

They use emails, social media messages, and even personalized phone calls to build a veneer of credibility. Authorities from some financial magazines have noted that at this phase, they combine different communication approaches with technical jargon that prospective investors find confusing and intimidating.

The scammers masterfully combine carefully chosen statistics and pure white lies in the form of testimonials, which kills off all initial skepticism and makes the mark feel like they belong to a thriving financial group.

3. Exploitation

The final stage of exploitation is where things get permanently ugly. After the victim fully commits, typically under the threatened "limited-time" deals, the scammer subsequently requests direct payment through untraceable means.

Here, the scammer is no longer interested in maintaining a cover of legitimacy but in moving funds beyond reach as quickly as possible. Scammers have also employed sophisticated networks of numerous intermediaries or cryptocurrencies to make payments, such that once the loot leaves a victim's account, it is literally out of reach.

Fortifying Your Defenses: How to Avoid A P2P Lending Scam

Besides following conventional wisdom like verifying credentials, keeping your passwords and sensitive data secret, and resisting aggressive sales tactics, try these advanced techniques:

- Peer intelligence: Verify investor forums where users post experiences and warn each other of new scams. These communities are usually the first to detect new tactics and to provide live alerts and best practices.

- Advanced digital mechanisms: Implement financial software that alerts you to unusual transaction requests and transactions. You can also try scam detection algorithms that compare behavioral patterns and financial anomalies.

- Ongoing learning: Subscribe to notifications and alerts from reputable financial watchdogs and regulatory bodies. Journals such as the Journal of Financial Crime and other scholarly journals provide detailed analyses of new scams. That way, you're not just reacting to scams as they occur – you are one step ahead.

By understanding these phases and equipping yourself with both social support and sophisticated digital tools, you create a robust shield against manipulative tactics. The key is to be inquisitive, well-educated, and watchful.

Even as technology and communication mediums evolve, the basic lessons in skepticism and verification do not change. With a mix of prudence and intellectual restraint, you can safely ride the potential of P2P lending without falling prey to its dark side.

Thinking Ahead of the Landscape

The virtual financial revolution has tremendous potential, but with that progress comes inherent danger. While the potential of P2P lending is enticing, the ever-changing tactics of those who want to exploit it for nefarious purposes remind us to be watchful, questioning, and well-informed. Your financial existence should blend thoughtful prudence with critical thinking, avoiding deceit while grasping legitimate opportunities.

Any decision in P2P lending is not merely a matter of anticipated gain; it's a matter of safeguarding your wealth. Trust but verify, and never let the hope of high returns get you to act in haste. A combination of scholarly insight, advanced digital competencies, and collective wisdom can guide you through the complicated landscape of P2P lending with safety and confidence.

When it comes to P2P crowdlending transactions, one of the most vigilant platforms in assessing counterparties and bringing all details to light for total transparency is 8lends. Each side is allowed the time that they need without having to provide irrelevant information. Smart contracts execute agreements automatically, giving access to loans controlled only by transparent, readable blockchain. Whether you’re a lender or a loan applicant, you get to monitor absolutely everything that’s going on.