What Does 'Default Detection' Even Mean?

Let’s start simple. A default basically means the borrower didn’t pay back the loan as agreed. This could be a missed installment, a full-blown ghosting of the lender, or anything in between. Detecting and predicting these situations ahead of time is super valuable because it helps platforms avoid big losses and also offer better rates to reliable borrowers.

The Old School vs. The New School

Back in the day, lenders used to rely mostly on a handful of things: credit reports, employment history, and maybe a couple of references. That’s still part of the equation today, but it’s not the full picture anymore.

Technology has become a very big part of it now. Platforms now use machine learning models that can spot patterns most humans wouldn’t even notice. We’re talking things like:

- How often someone changes jobs

- How quickly they type in their application

- What time of day they usually pay their bills

- Their phone usage patterns

These tiny signals, when crunched together, can paint a surprisingly accurate picture of someone’s likelihood to repay.

For example, someone who changes jobs quickly and pays their bills later in the day may not be financially responsible. They are unable to commit to a job, and they are not intentional about paying their bills. To wit, they are likely to default on their loans.

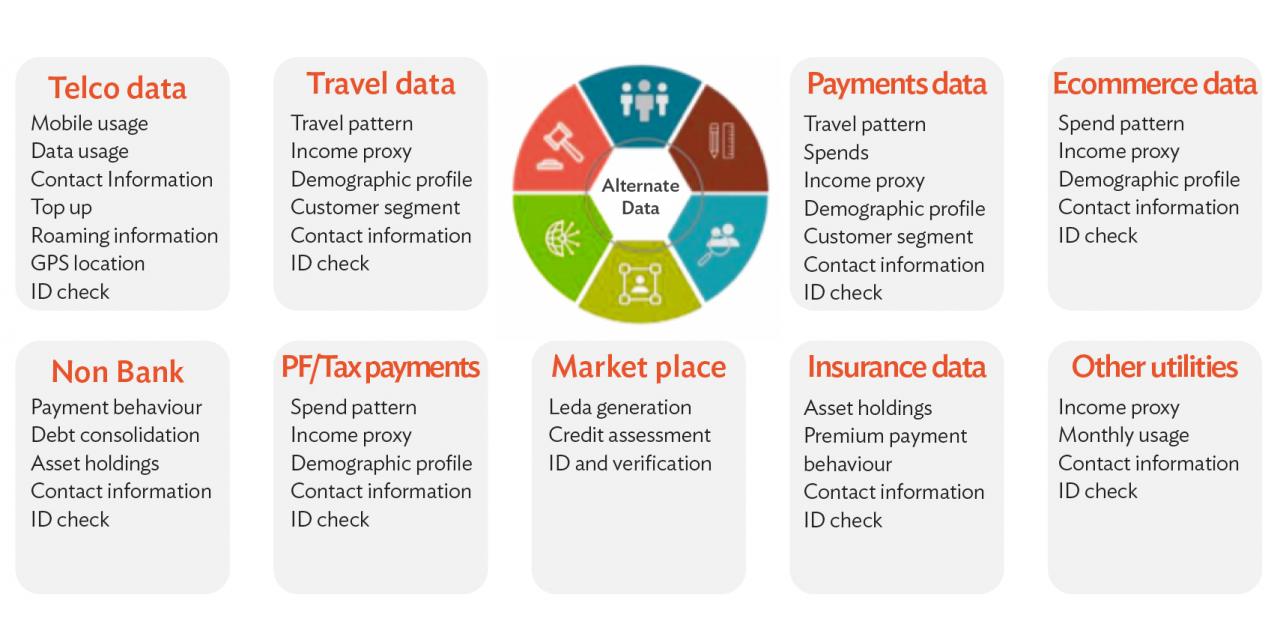

Alternative Data: It’s Not Just About the Credit Score

A lot of people, especially in developing markets, don’t have traditional credit scores. That used to be a problem. Now, lenders can look at alternative data. Think mobile phone top-ups, utility payments, rent records, or even social media behavior.

For example, someone who pays their phone bill on time every month is statistically more likely to repay a loan than someone who doesn’t. Doesn’t sound super scientific? Well, the models disagree.

Case Study: 8lends

8lends, a crowdlending platform based in Switzerland, uses alternative data from borrowers’ smartphones to assess creditworthiness. This includes outstanding loans, marital status, and more. They’ve been able to offer loans to thousands of people and haven’t had a default or late payment yet.

That’s the power of smart tech when used responsibly.

A report by the World Bank shows that using alternative data can significantly reduce default rates while expanding access to credit. It’s a win-win.

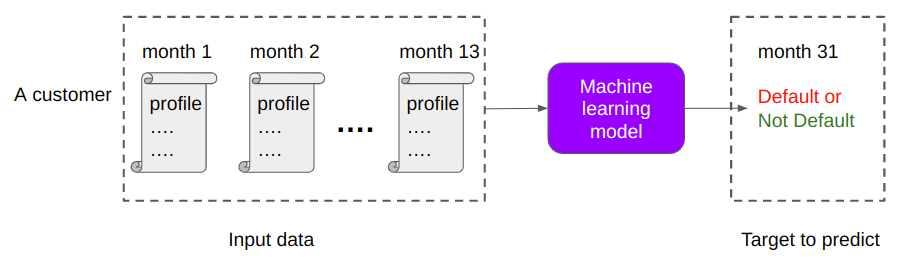

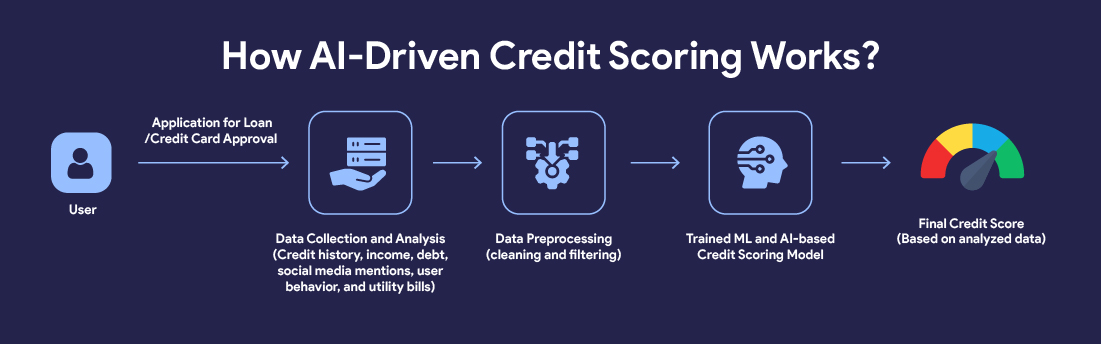

Machine Learning Models: The Real Brains Behind It All

So how does it all work behind the scenes? Thousands, maybe millions, of past loans are fed into a machine learning model. The model learns which loans defaulted, and which ones didn’t, and then finds patterns among them. Did borrowers who lived in a certain area tend to default more? Was there a link between loan amount and repayment success? Did people in certain industries default more?

The more data you feed it, the smarter it gets. Over time, these models can become eerily accurate. But they still have flaws. If the data going in is biased or incomplete, the predictions can be way off. That’s where human oversight still plays a key role. It is essential to feed it data that cuts across the board. This will make it easier for predictions to deal with a wide variety of situations.

Real-Time Monitoring: Not Just a One-and-Done

Prediction doesn’t stop at loan approval. Many platforms keep monitoring borrowers in real-time. They can track payment behavior, spending habits, and even changes in mobile app activity.

Let’s say a borrower who usually pays on the 3rd suddenly misses two payments. A smart platform can flag that immediately, trigger reminders, offer restructuring options, or start the collection process before the loan spirals out of control.

Some platforms even use sentiment analysis to read emails or support tickets. If a borrower starts writing in a more stressed or negative tone, it might signal financial distress. This may be considered creepy and even invasive, but they have been considered useful in limiting loan defaults.

Fraud Detection and Identity Checks

Another big piece of the puzzle is making sure the person applying is actually real, and not trying to scam the system. This has become really essential due to the emergence and increased use of technology such as deep fakes to trick live facial recognition systems. It doesn’t end there, now documents are also easily faked to the point where it is hard to tell a real one from a phony.

Lenders now use facial recognition, document scanning, device fingerprinting, and even geolocation checks to ensure that they are lending money to an actual person.

A sudden change in IP address or someone applying from a high-risk location might raise red flags. It’s like airport security, but for loans. The systems track subtle inconsistent behaviors and flag them.

Ethics and Privacy Concerns: Where's the Line?

Now, let’s pause for a second. With all this tech peering into people’s lives, privacy concerns are 100% valid. Should a lender really be allowed to track your phone habits or scan your Facebook posts? There’s a balance to be struck between effective risk assessment and ethical data use. Many platforms are working under strict data protection laws (like GDPR in Europe), but others? Not so much.

At the end of the day, transparency matters. Borrowers should know what data is being used, and why. Unfortunately, even when lenders try to tell what their data is being used for, borrowers rarely read the fine print.

The Future: Predictive Models Get Smarter

So, where is this all going? Models will only get smarter as more data becomes available. AI is already being used to simulate entire economic environments, test out how borrowers might respond to different interest rates, and more. The real goal? Personalizing loans to fit each borrower’s reality. Imagine a world where your loan terms adjust automatically based on how you’re doing financially.

Final Thoughts

Technology is making lending more fair, efficient, and accessible. But it’s not perfect. It still needs the human touch. Whether that's setting ethical boundaries or stepping in when the tech gets it wrong. Default prediction isn’t just about math. It’s about understanding people. And as tech continues to evolve, the platforms that balance brains and heart are the ones that’ll win.

Because at the end of the day, lending isn’t just about risk. It’s about trust. And trust? That’s still pretty human. People do not trust machines. Without a human touch, people will not trust the system and processes.

Crowdlending platforms like 8lends allow people to spread out the risk of defaults across multiple different projects while sharing the risk with other investors in each project. Fortunately, in 8lends the risk is very low, since there hasn’t been a late payment yet.