Understanding P2P Lending and Loan Defaults

P2P lending platforms like 8lends make borrowing easy by linking people who need cash with those ready to lend it based on credit checks. Even with clever systems, someone can still miss a payment or not pay back what they owe. This slip happens when borrowers skip interest or the main sum, and it feels risky. Both the borrower’s situation and how the site works play a part in figuring out what’s behind these misses.

Determinants of P2P Loan Defaults

Real-world studies show exactly why some peer-to-peer loans go south. A deep dive into data from 2008 through 2014 pulled out the top warning signs.

The table below lays out these factors to guide your understanding.

This study showed a 10.9% default rate – 2,666 out of 24,449 loans – and makes it clear that who the borrower is (their income and past credit) and what the loan looks like (its size, term, interest) really matter. The mix of those personal traits and loan details can make or break repayment.

Digging into China’s P2P world adds more color. One look at Renrendai data found that people who passed quick checks like video calls or phone confirmations actually missed payments more often, while those who provided solid ID or asset proof cut their risk, and the models nailed it with over 90% accuracy, to predict defaults well.

Then there’s the shocker: by 2019, defaults in China hit 87.2%. That sky-high rate got blamed on a poor match between borrowers and backers, investors flying blind on finance, and rules that just weren’t strong enough.

Case Studies: Notable Failures and Their Postmortems

Looking at real-life cases of P2P lending failures helps uncover deep-rooted problems in the system. Take China’s P2P crisis, which hit its worst point in 2015. Out of around 3,500 platforms, two-thirds collapsed. Many failed because of scams, fake investment schemes, or acting like illegal banking operations.

Regulators couldn’t keep up, with just a handful of staff trying to monitor thousands of platforms, so things spiraled out of control. Close ties between platforms and local governments often meant loans went to risky ventures. When officials started warning investors, panic spread. By July 2018, active investors dropped by a fifth, and total loans plunged from over 1.3 trillion yuan to below 1 trillion.

LendingClub in the U.S. had its own troubles. For a time, they limited transparency around loan details during their “Quiet Period,” and their CEO was caught altering data. These moves made investors uneasy, adding to the sense of risk.

In China, Renrendai faced similar challenges. Weak regulations, high rates of defaults, and sudden cash shortages exposed flaws unique to the platform. Each story shows how fragile these systems can be, especially when rules aren’t clear or risks aren’t managed with care.

Lessons Learned from Failure Postmortems

Looking at past mistakes teaches us valuable lessons for building better systems. Here’s what we’ve learned:

- Being Open Matters: When platforms don’t share clear, updated details about their work, people stop trusting them. Take GraduRates or Encash—both shut down quietly, leaving lenders confused. Sharing honest, timely updates helps everyone stay informed and confident.

- Rules Aren’t Optional: Ignoring guidelines can lead to big problems. In China, weak oversight allowed fraud and risky behavior to spiral. Sticking to regulations, like India’s RBI rules, keeps platforms legally safe and protects everyone involved.

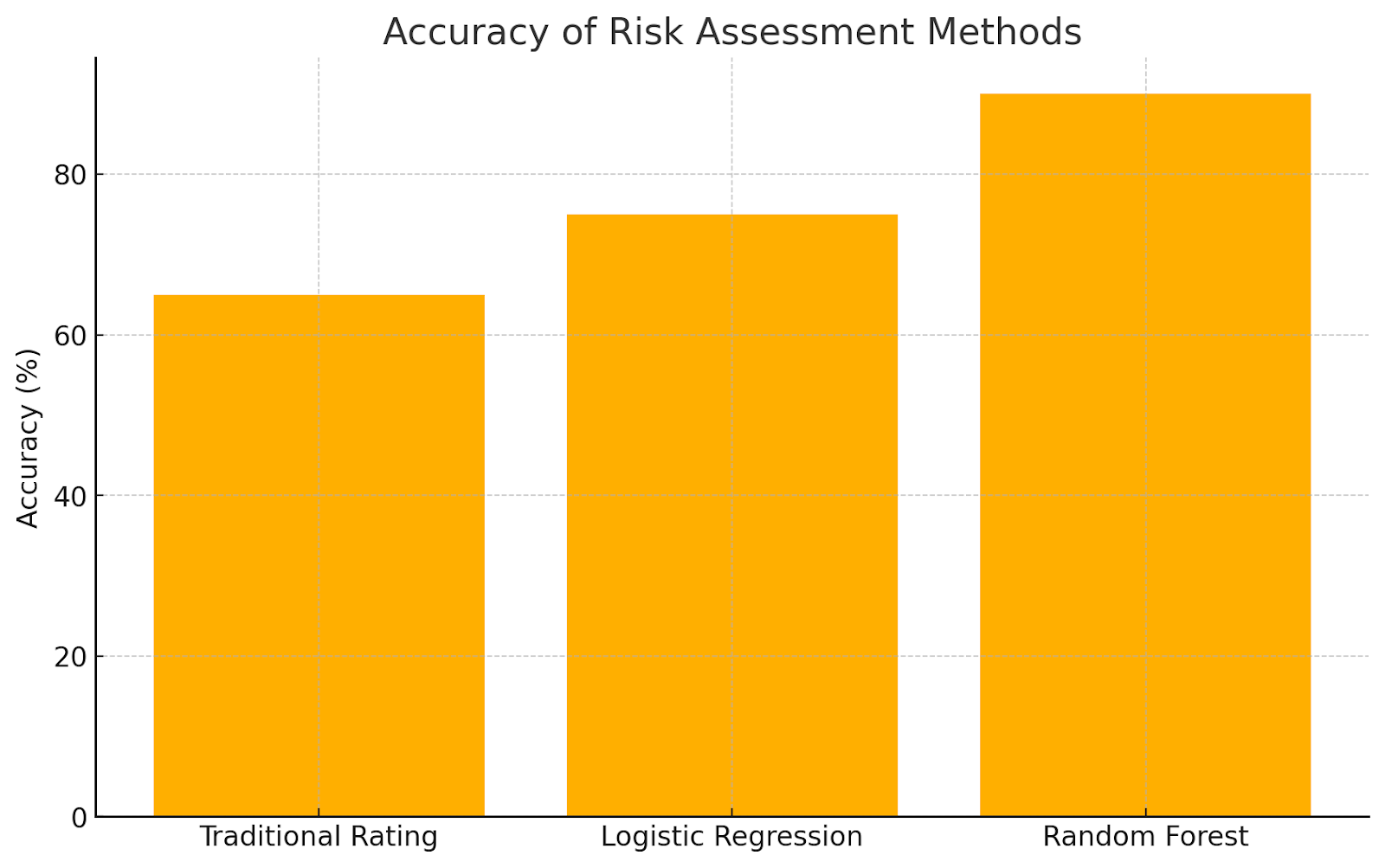

- Smarter Risk Checks: New tools are changing how risks are spotted. Research shows methods like Random Forest (a type of machine learning) work better than old-school systems. Even small details, like how borrowers describe themselves or their connections, help predict who might struggle to repay.

- Spread Out, Stay Safe: Putting all funds into one loan is risky. Platforms like Prosper learned this the hard way when defaults hurt their lenders. Splitting investments across many loans softens the blow if one fails.

- Keep Growing, Keep Learning: Success isn’t static. Platforms like LendingClub built trust by openly sharing data and teaching users. Others tweak their systems using lessons from past errors. Over time, these steps create stronger, more reliable systems.

By focusing on these areas, platforms can build safer, more trustworthy spaces for everyone. Small changes, when done thoughtfully, add up to big improvements.

Advancements in Risk Management Practices

Looking back at past experiences has sparked new ideas in managing financial risks. Platforms now use things like social information or community activity to assess creditworthiness more accurately, so that lending decisions better reflect real-life situations.

Advanced techniques, like machine learning and survival analysis, often work better than traditional platform ratings, uncovering hidden chances for smarter investments while encouraging fairer rates for borrowers.

Tools like SHAP help explain how these complex models make choices, shining a light on familiar risks as well as unexpected ones that might otherwise go unnoticed. Some systems even analyze relationships between borrowers, like shared connections or networks, to spot patterns that improve predictions.

Together, these steps lower the chance of loans going unpaid, which helps investment portfolios grow steadier over time and keeps platforms running smoothly for the long haul. By blending technology with deeper insights into human behavior, the whole process becomes both safer and more balanced for everyone involved.

Conclusion

Looking back at why P2P loans flop shows how the borrower, the platform, and the rules all mix. We need to learn from each flop so that we keep things clear, check risks well, and follow the rules. We can keep getting better with smarter data tools and by spreading out our bets. That way, P2P lending can stick around as a solid choice alongside regular banks.

8lends backs up lender investments using borrower collateral. This significantly adds to the security of their loans, even if risk can never be completely eliminated. Opportunities meanwhile abound with 0% commission charged to investors and over 15% returns.