Risk Profile and Creditworthiness

Let’s kick things off with the risks because nobody likes surprises when money’s on the line. With individual lending, things are pretty standardized. You've got things like:

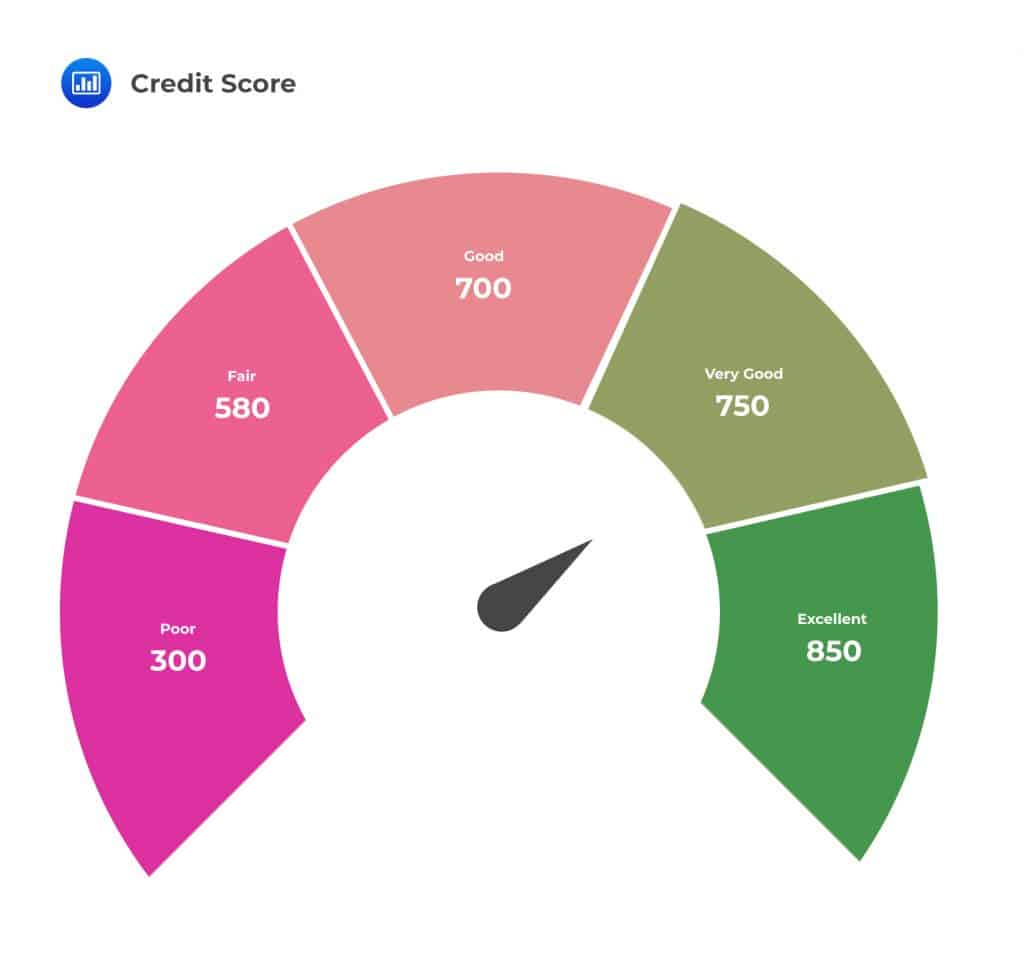

- FICO scores

- income verification

- debt-to-income ratios

It is easy to determine your creditworthiness with these. It’s like a paint-by-numbers approach to figuring out who’s good for the money. SMS are a whole different ball game. A lot of small businesses don't have tidy financials or credit scores you can rely on. Some don’t even have proper books. And when something like a pandemic or inflation hits, SMEs can feel it hard and fast. That unpredictability adds an extra layer of risk.

But here’s a twist: SMEs often have assets. Maybe it’s equipment, inventory, or even future receivables. That means if things go south, there might be something to recover. Individuals? Not so much. Most of them barely have any collateral to use as a safety net.

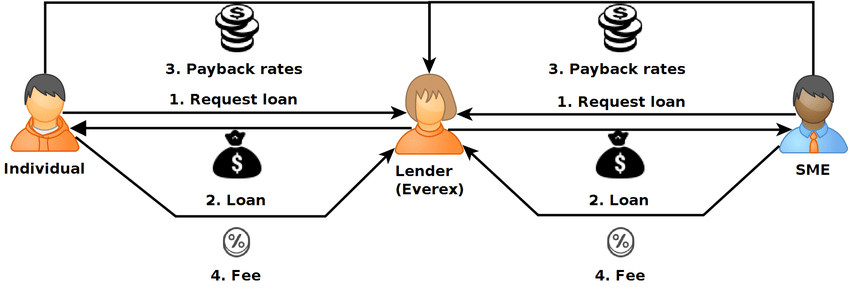

Within the last ten years, crowdlending has taken much of the world by storm and is extending credit to people who have never had access to it, as well as presenting brand new lucrative income opportunities for investors who can pitch in and share the burden of multiple loans. One such project is 8lends.

Returns and the Profit Puzzle

Now let’s talk money, because at the end of the day, that’s what most investors care about. SME loans usually bring in higher returns. Why? Because businesses are more willing to pay a premium when they need funding to grow, survive, or pivot.

But managing SME loans is pricey, unfortunately. You might need people in the field, detailed documentation, and longer processing times. It's an arduous process. Contrary to that, consumer loans are often automated. All you need is to log in, answer some questions, and upload some documentation. You get approved and you get some funds. Everything can be done online and it takes less time.

So it’s a classic trade-off. High returns with higher costs for SMEs. Lower margins but better scalability with individuals.

Default Rates and Real-World Performance

Statistically, individual loans usually have lower default rates, especially in places with strong employment and solid financial regulations. But that doesn't mean they’re a free pass. If someone loses their job or has a medical emergency, they can easily default on an unsecured loan.

SMEs, on the other hand, tend to default more often, especially in countries where the economy is a bit shaky. But wait, it's not all bad news. They also present an advantage, they also have better recovery rates. Why? Because even if a business closes, there’s often something left behind to collect. They often have machines or even buildings that can be sold to cover the loan.

A 2023 report from the IFC found SME loan recovery rates can hit over 60% in emerging markets. Not too shabby. Meanwhile, unsecured personal loans often go completely bust.

Regulation: The Rulebook Factor

Lending to individuals comes with a well-worn rulebook. There are consumer protection laws that spell out what you can and can’t do, from interest caps to how you handle debt collection. It’s structured, sometimes annoyingly so, but it brings predictability.

SMEs, on the other hand, are murkier. In some countries, there's a total lack of formal lending rules for small businesses. This presents advantages and disadvantages. The good thing is that lenders have more room to be flexible. The bad side of this is that the legal gray areas can lead to headaches if things go wrong.

That said, there's momentum building. Governments and global organizations are realizing how vital SMEs are to economies. According to the OECD, SMEs can account for up to 70% of employment and half the GDP in many countries. That’s a big deal. And it’s pushing for better frameworks and access to capital.

Demand and Market Trends

There’s massive demand for personal credit. People want loans for everything from smartphones to college degrees. Fintech companies are cashing in by making it all digital and lightning fast.

But the SME side? It’s still underserved. A lot of banks won’t touch small businesses because they don’t fit into neat little boxes. That’s where alternative lenders, P2P platforms, and microfinance players are stepping in.

The World Bank says SMEs in emerging markets face a whopping $5 trillion credit gap. That’s not just demand, that’s an open door.

Meanwhile, the personal lending space has become a crowded marketplace where everyone's fighting over the same borrowers. SME lending is where the real white space exists for lenders willing to think differently. And if they play the game right, they will reap the benefits of lending to these small businesses while encountering minimal risks.

How Macroeconomics Plays a Role

Let’s make no mistake – none of this happens in a vacuum. When the economy shifts, both individuals and businesses feel it. When high inflation and rising interest rates hit, people are badly affected and well laid financial plans crumble. Then, paying back loans isn’t so easy.

Individuals might start defaulting on personal loans because they need to keep the lights on and food on the table. SMEs? Depends on the industry. A logistics company might thrive while a boutique clothing shop struggles.

Diversifying across borrower types can be a good way to hedge against these shifts. What hits one group hard might leave another relatively untouched.

The Tech Factor

Tech is a game-changer in both camps. For personal lending, we’ve seen massive leaps. We also mentioned how digital changes have made applications and approvals easy. In recent times, we see apps that approve you in minutes, real-time credit scoring, even AI-powered risk models.

For SMEs, it’s catching up. Lenders are now using alternative data like POS transactions, social media engagement, and supplier history to get a clearer picture of a business’ financial health. Products like invoice financing and revenue-based loans are also helping tailor solutions to how SMEs actually operate.

It’s not perfect, of course. Tech alone can’t replace good judgment, and in both segments, over-reliance on algorithms has led to some notable busts. Still, innovation has improved the ability to scale lending while keeping an eye on risk.

Final Verdict: So, Who Wins?

Should you prioritize lending to individuals or to SMEs?

It depends. Consumer loans are great for scaling quickly with predictable processes. SME loans can deliver higher returns but need more work, more analysis, and more patience.

Some of the smartest lenders out there are doing both. They blend strategies to balance risk, reward, and resilience.

At the end of the day, it’s not just about numbers. Lending has the power to change lives. Whether it’s helping someone pay for college or giving a mom-and-pop shop the boost it needs to stay afloat, it matters. And that might just be the best return on investment there is.

Hence, it will not be easy to identify If you would like to try your hand lending to individuals or businesses through the groundbreaking technology of blockchain, 8lends provides you that opportunity with the loans backed by borrower collateral and no commissions charged to the creditors.