What is Automated Underwriting?

Automated underwriting uses AI and machine learning to check loan applications. It looks at things to build a fuller picture like:

- credit scores

- income

- job history

- bits of social media activity

- spending records

Underwriting by hand takes time and leans on each person’s own judgment. Crowdlending sites handle so many loans that they rely on automation to keep things moving. It speeds up decisions and feels fairer, yet it brings about certain issues that need careful handling.

Pros of Automated Underwriting in Crowdlending

Automated underwriting offers several advantages for crowdlending platforms:

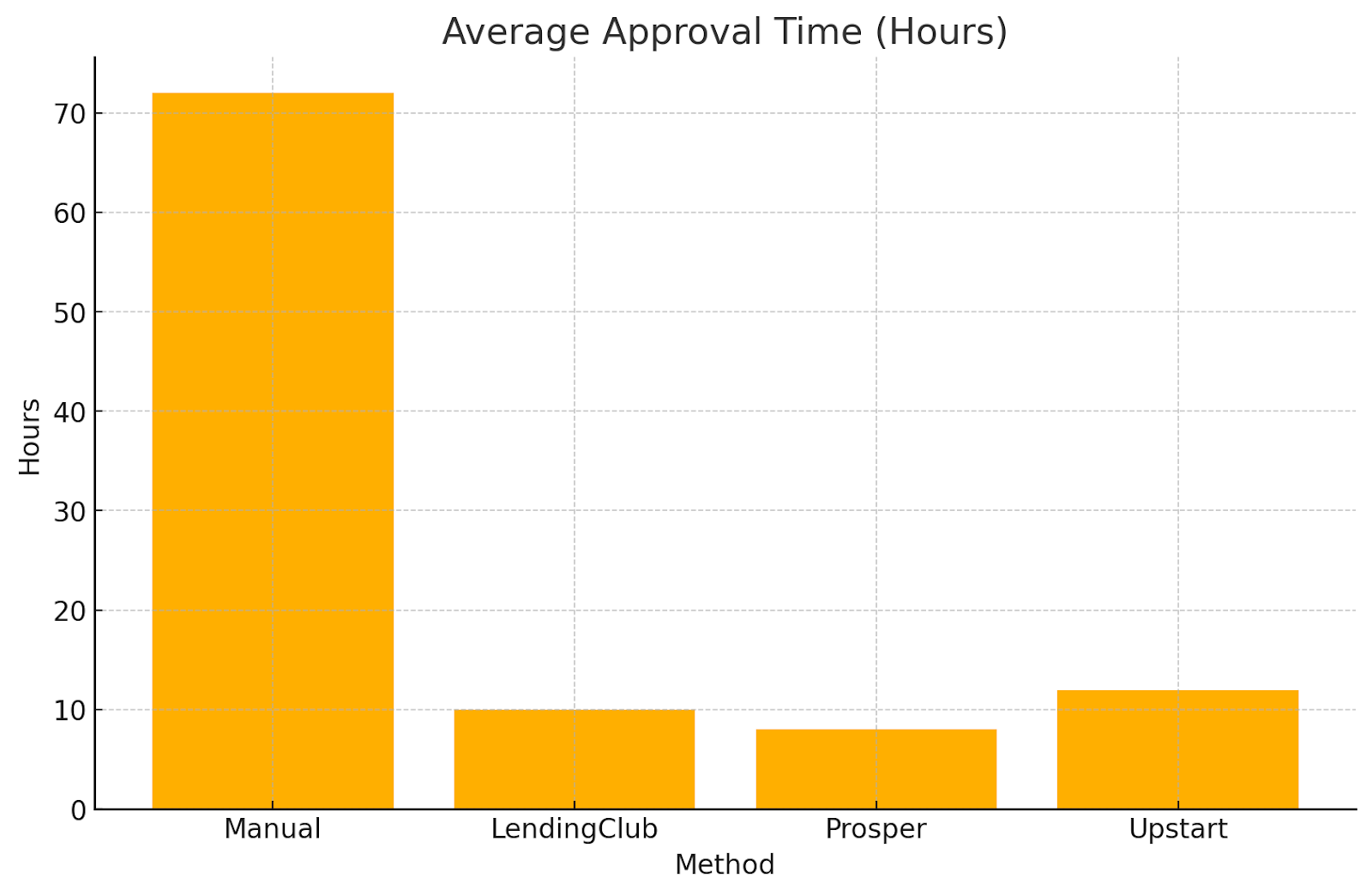

Speed and Efficiency

It speeds up loan approvals from days or weeks to just minutes. This quick turnaround is a real help for crowdlending sites that deal with many small loans every day. Platforms such as 8lends count on fast decisions to keep things moving smoothly. Fast responses make borrowers happier and draw more investors in.

Cost Savings

Cutting out much of the manual work slashes costs for crowdlending platforms that run on tight budgets. Those savings can turn into lower rates for borrowers and better returns for investors. This edge makes these platforms more competitive than old-school banks.

Consistency and Objectivity

Automated systems treat every application the same way, which removes personal bias and keeps decisions fair. That fairness builds trust with investors who need reliable risk ratings. It also helps keep loan quality high by preventing human mistakes.

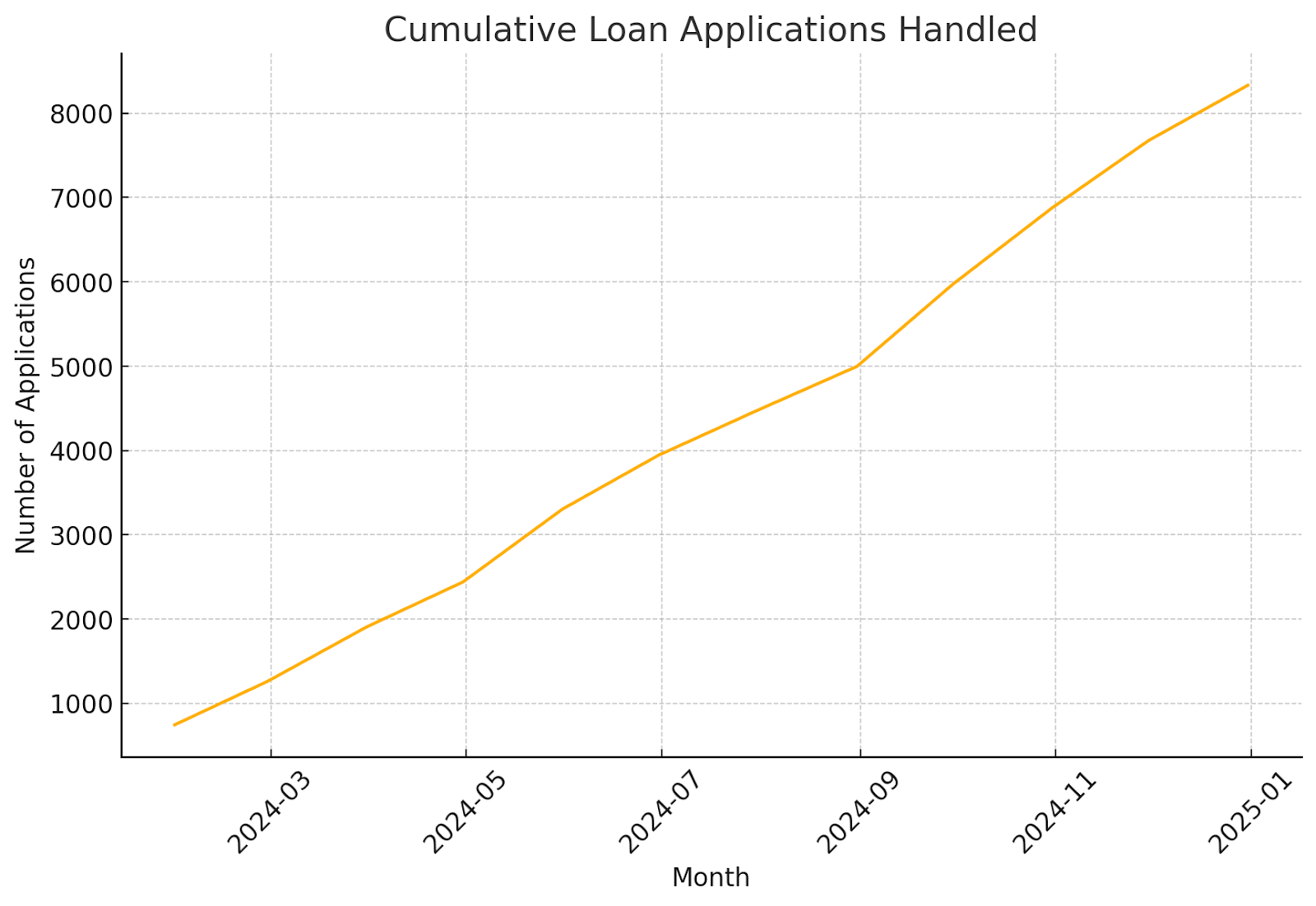

Scalability

When crowdlending platforms grow, they need a way to handle more applications without hiring more staff. Automated underwriting scales up easily, so sites can expand without stretching their teams too thin. This is key for platforms serving people around the world, where they might face almost endless demand.

Data-Driven Decisions

Smart algorithms look at everything from credit scores and income to job histories and even online activity. This full-picture approach often spots good borrowers that older methods miss. Some systems blend traditional and alternative data for instant, precise credit checks. So lenders know they’re making solid choices.

Cons of Automated Underwriting in Crowdlending

Despite its benefits, automated underwriting has notable drawbacks.

Risk of Bias

Algorithms seem fair, but they can repeat unfair patterns when they learn from biased data. A Lehigh University study showed that some lending models turned down more black applicants and charged them higher rates than white applicants with similar profiles.

The Federal Reserve also spotted gaps in denial rates that may come from hidden biases or missing information. In crowdlending, this can hurt diverse borrower groups, so strong fair-lending checks are needed.

Demographic Group

Denial Rate (%)

Lack of Flexibility

Automated systems follow pre-configured rules and may fall flat in the event of unusual situations. Someone with irregular income or a one-of-a-kind financial story could be unfairly denied. Human underwriters can look at life details and make judgment calls. Automated tools can’t match that kind of a personal review.

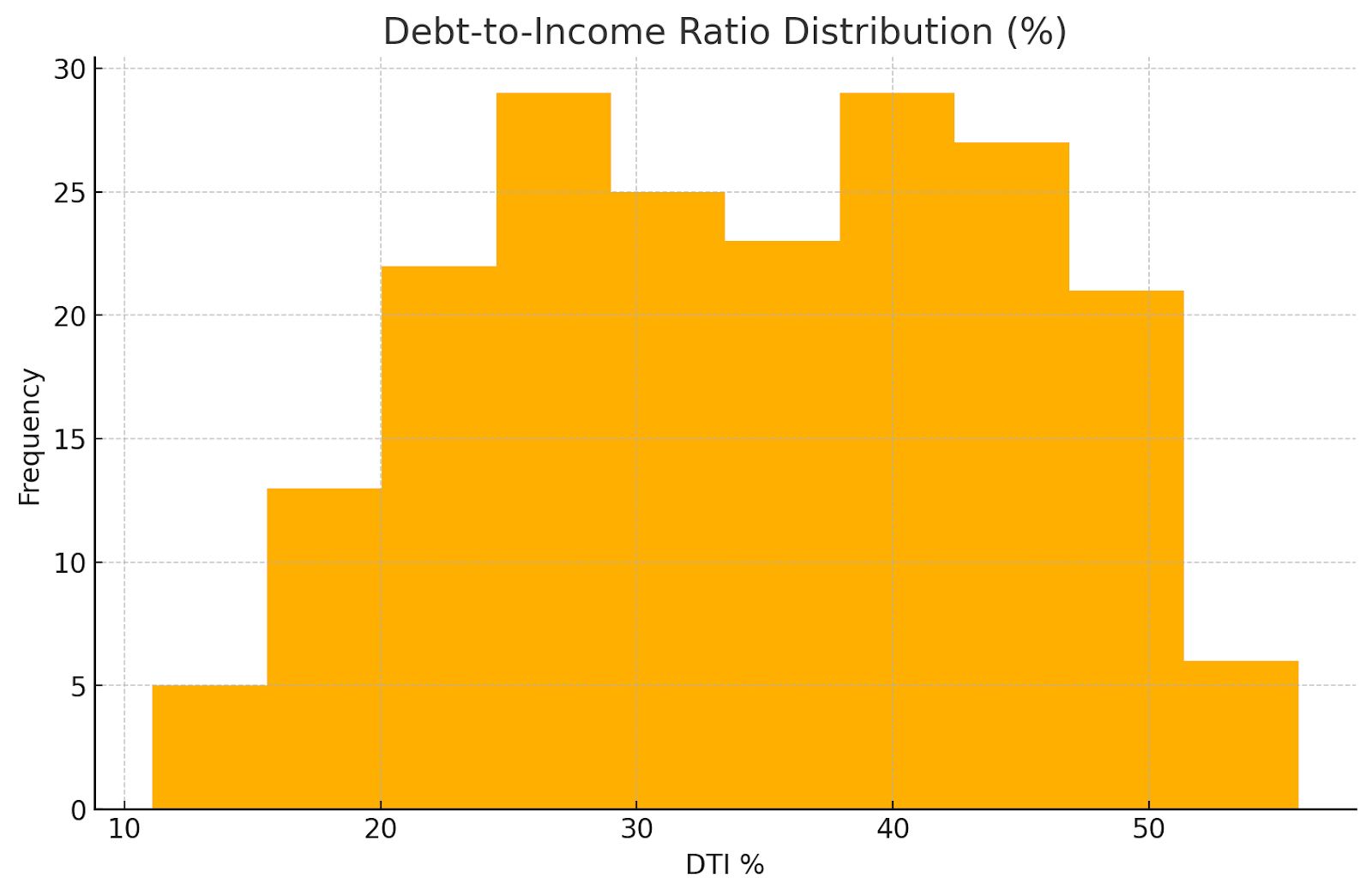

Dependence on Data Quality

Good decisions need good data. If the data is wrong or old, the system might approve a risky borrower or refuse a safe one. This problem grows when data comes from outside sources. Connected, up-to-date data is key so that automation can work well.

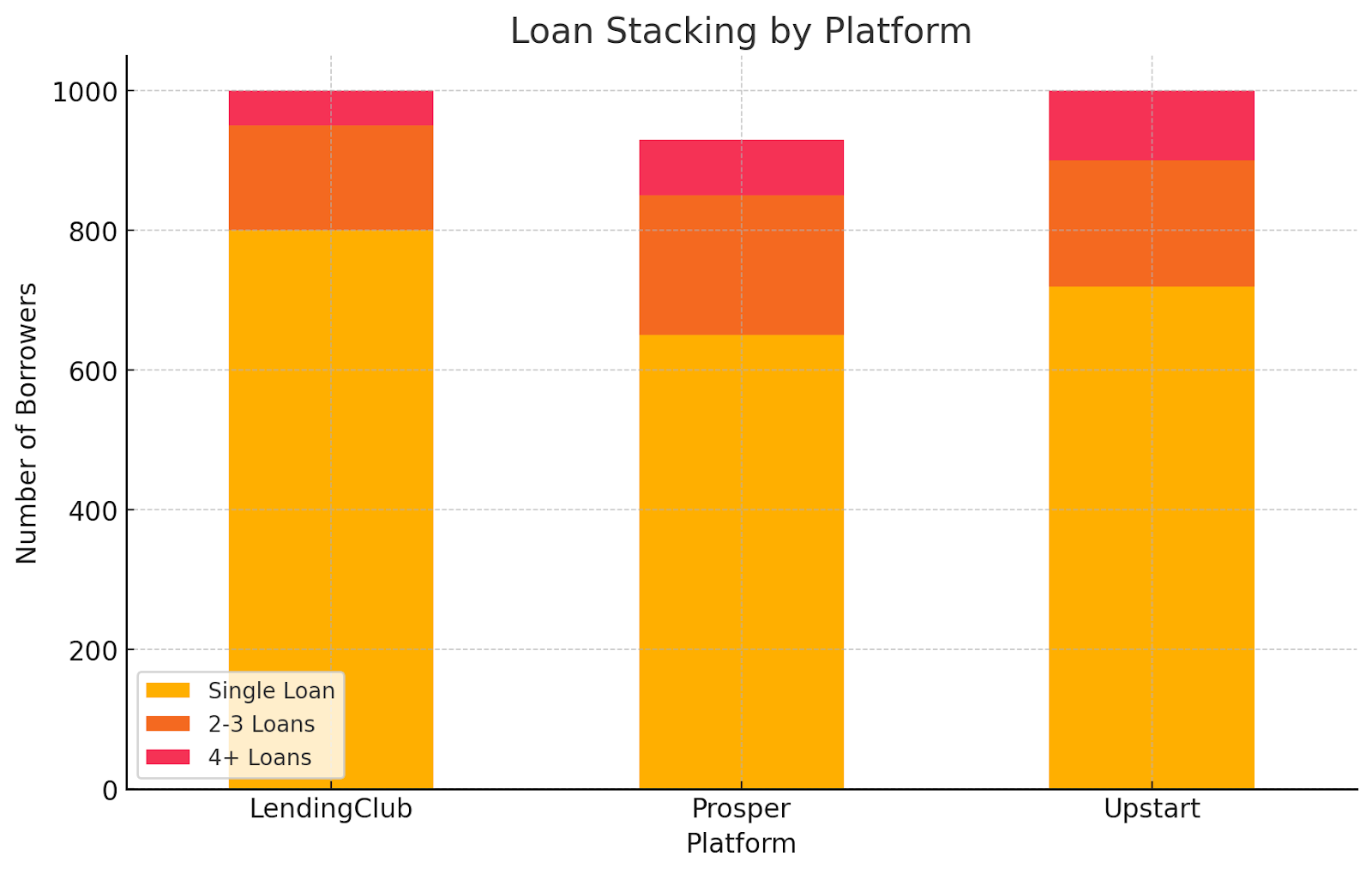

Potential for Stacking

Stacking happens when borrowers take out several loans in a short time, often hiding their total debt. Automated systems may not catch this, and people can end up over-borrowing. This risk affects both the platform and its investors, especially in crowdlending where each site works on its own.

Regulatory and Compliance Risks

Underwriting software must follow laws like the Equal Credit Opportunity Act (ECOA) and Regulation B. It must not treat age or other protected traits unfairly. Regulators watch these systems closely for bias. NAFCU raised alarms about age-based differences, and the Consumer Financial Protection Bureau (CFPB) warned about bias in automated checks. Keeping algorithms up to date to meet rules takes time and resources.

Addressing the Challenges

To lower the risks in automated underwriting, crowdlending platforms can take the following steps.

- Regular audits and checks: Carry out reviews of underwriting models on a set schedule. Find and fix biases or mistakes. Stay in line with fair lending rules.

- Use varied and fair data: Train the models on data from many different groups. This cuts down on old biases that might creep in. It also answers worries about racial bias in AI.

- Mix machine work with human review: Let the system handle most cases, but flag the tricky ones. Then have a person step in to make the call. This blend speeds up simple loans while still giving room for judgment when it’s needed, so that no case is rushed.

- Strengthen data checks: Put strong verification steps in place. Make sure all borrower information is accurate and complete. This fixes the problem of models choking on bad or missing data.

- Share insights across the industry: Team up with other platforms or trade groups to pool data on total debt levels. Spot borrowers who take on too many loans at once. Joining efforts like the Small Business Finance Exchange can help stop stacking before it starts.

Real-World Examples and Case Studies

Specific stories show both the good points and the hurdles. LendingClub, a well-known crowdlending site, now uses an automated process that looks at hundreds of details instead of fixed cutoffs to approve borrowers who might have been turned away before.

Yet LendingClub and other platforms ran into trouble when some people took out several loans at once, showing a need for stronger checks. Research from Lehigh University and the Federal Reserve also highlights bias worries, revealing racial gaps in AI-driven mortgage choices that likely carry over to crowdlending too.

Conclusion

Automated underwriting changed crowdlending in a big way. Loans now move faster and cost less, and platforms can handle more applications without breaking a sweat. It checks each file the same way every time, so that small lenders can grow and stand up to banks. Still, it isn’t perfect. Bias can slip in, rules can feel too rigid, and poor data leads to poor choices. There’s also the chance of too many loans stacking up, plus the maze of regulations to navigate.

Facing these issues head-on makes all the difference. Crowdlenders can build in checks against bias and keep their data clean. They can tweak rules when life doesn’t fit a formula, and stay on top of new laws. Doing so brings together speed and fairness. As the field moves forward, watching for risks and staying flexible will help both borrowers and investors enjoy the best of this technology.

8lends is a spectacular platform when it comes to efficient underwriting, providing justified opportunities for those who are truly strong borrower candidates and lucrative returns with little to no downside. 8lends has yet to experience a default or late payment.