Tax residency determination

Residency is determined by actual ties to the country — not formal checkmarks alone.

Center of vital interests

This refers to where your personal or financial life is chiefly based.

Personal ties may include:

- Loved ones' location

- Permanent home

- Kids' school

- Social affiliation

Economic ties include:

- Workplace

- Business address

- Banking and holdings

- Income source

Six months per year

183+ days in a year on the whole means you're a resident, including partial days. This is especially relevant for remote workers and individuals who split time between Poland and other jurisdictions.

If either of these conditions applies, you pay KAS tax in unlimited, global fashion.

Taxable income

When it comes to crypto taxes, the primary obligation for most people is the flat 19% capital gains tax owed when you profit from disposing of crypto. That applies to situations where:

- You paid off debt with your crypto

- You converted to fiat

- You bought goods or services with it

In order to calculate your gains, you take the price at which you disposed of your crypto and subtract what you paid for it along with any directly associated fees and commissions paid to the platform or for gas fees. None of your business expenses incurred in an effort to generate crypto income can be subtracted from your tax obligation. There is also no minimum threshold for tax obligation and no standard deduction.

If you were gifted crypto or obtained it through an airdrop or mining, you don't owe taxes at the moment of receipt — but when you dispose of it, your cost basis will be zero in all of these cases, meaning you will end up paying a larger total tax than if you had acquired it at a documented price.

Documentation necessity

Changing tax residency can significantly affect how and where your cryptocurrency income is taxed, so timing and documentation matter just as much as the transactions themselves. For anyone planning to leave or enter Poland, proactive tax planning can help avoid unexpected liabilities, reporting errors, or disputes with the KAS.

One of the most important steps is to clearly document the moment your tax residency changes. This includes keeping evidence of departure or arrival dates, rental or purchase agreements, employment contracts, school enrollment for children, and any official deregistration or registration documents. Because Poland allows "split-year" or broken tax residency, the exact timing of your move determines which income is taxed as Polish-source and which falls under another jurisdiction.

Non-taxable events

Simply holding crypto is not taxable, regardless of price changes. Likewise, buying crypto with fiat does not create any tax liability, although the purchase price and fees should be recorded as future cost basis. Transfers between your own wallets or exchanges are also non-taxable, as long as ownership does not change.

Receiving crypto as a gift or inheritance is not subject to PIT-38 at the time of receipt. Instead, it falls under inheritance and donation tax rules, with close family members often qualifying for full exemption if they file the SD-Z2 form on time. Tax only arises later if the crypto is sold.

Rewards are generally not taxed when received, but become taxable upon disposal — usually with a zero cost basis unless documented otherwise. Finally, unrealized gains or losses caused by market price changes have no tax effect until the crypto is actually disposed of.

Changing tax residency in the middle of the year

Polish tax law allows for what is commonly called "split" or "broken" tax residency, meaning a person may be treated as a Polish tax resident for only part of a calendar year and a non-resident for the remainder, provided the factual conditions are met. The tax authorities assess a change in residence based on facts, not declarations alone.

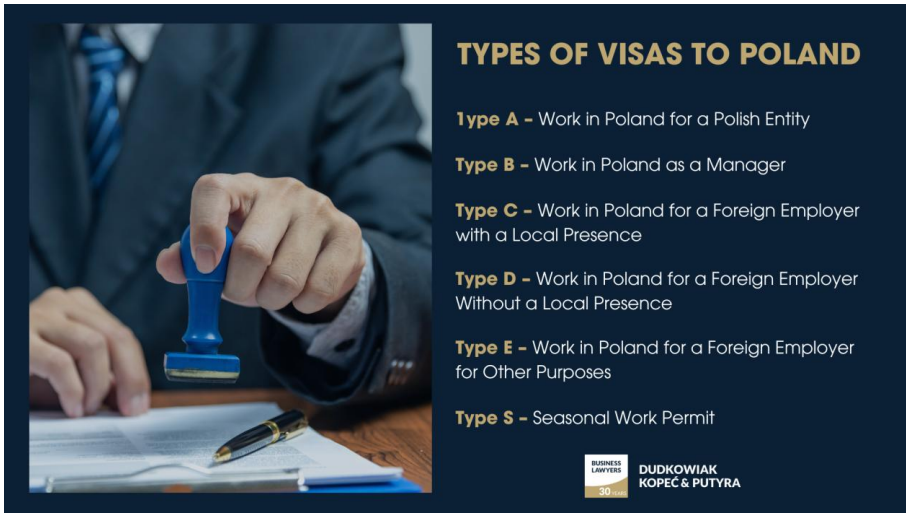

Polish visa options

Poland offers several ways for non-EU professionals to live and work legally:

- Freelance / "digital nomad" route: Register as a sole proprietor (jednoosobowa działalność gospodarcza) to work for domestic or international clients. The visa is valid for 1 year and extendable up to 3 years. You also gain access to Poland's social security and healthcare.

- Work visa: For those with a job offer from a Polish employer. Requires a contract and proof of qualifications. Validity typically matches the employment term.

- Business / investment visa: For entrepreneurs starting a business in Poland. Requires business registration, financial proof, and a plan for sustaining operations.

Balancing crypto risk with alternative investments

While cryptocurrency offers high potential returns, it is also volatile, and tax obligations in Poland apply strictly to disposals — making careful planning essential. One way to balance risk is by incorporating other types of investments alongside crypto. Crowdlending, for example, provides a more predictable income stream, often with clear tax reporting and lower volatility compared to crypto trading.

Platforms like 8lends allow investors to fund loans to vetted borrowers, spreading risk across multiple participants. Income from these loans is generally straightforward to report in Poland and can complement your crypto portfolio, helping manage both cash flow and tax exposure. Such investments are free of VAT and PCC obligation.

Conclusion

Grasping tax residency and crypto reporting in Poland may seem complex at first, but getting it right will save you money and stress. By being fully aware of how the law evaluates your ties to Poland, documenting your transactions meticulously, and correctly reporting gains and disposals through PIT-38, you will put yourself in a much more advantageous position. Knowing which events are taxable and which aren't gives you another major edge that you can actively plan around.

For investors looking to balance high-risk crypto holdings with more predictable income, crowdlending is an excellent option. 8lends lets you invest in loans to vetted borrowers, offering structured returns, simplified tax reporting, and reduced exposure to market volatility.