The Golden Rule: It's All About the Taxable Event

Whereas Germany has a more period-based possession policy, the UK regime is event-oriented. You're only liable when a "taxable event" occurs.

Your main triggers are:

- Converting coins into GBP/fiat: The simplest thing to occur. You convert your asset into government-printed money.

- Swapping tokens for tokens: This is wholly necessary. Swapping Bitcoin for Ethereum, or any currency for another, is a taxable exchange in the UK. The taxman views this as selling one investment and acquiring another.

- Trading digital currency: Spending your crypto holdings on a laptop, a cup of coffee, or anything is essentially no different than a sale. You are giving up the asset.

- Earning tokens: Receipt of tokens as payment for goods/services or as rewards for lending/staking counts as income (below).

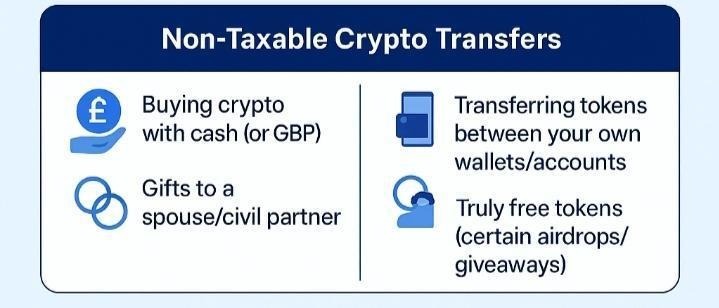

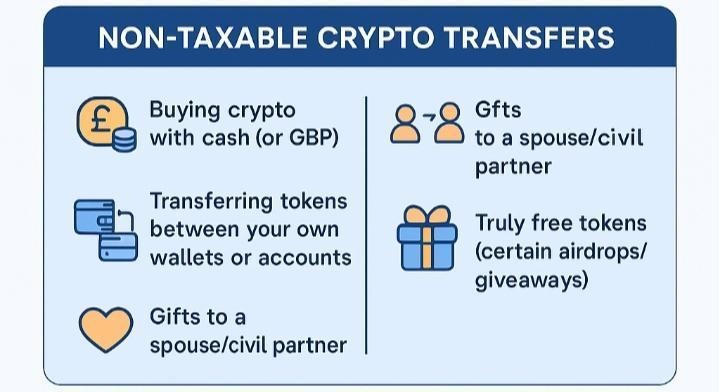

What is not a taxable event?

Buying coins with GBP and keeping them.

- Moving your assets from one of your accounts to another: not usually a sale, provided that you retain beneficial ownership; maintain open records to validate this.

- Gift aid on charitable giving: gifts of tokens can't be gift aid-eligible (the taxman does not regard such holdings as "money"). There are some gifts with certain CGT relief, but the rules are complex, so don’t assume relief is automatic until you look at the details.

The Two Pots of Levy You Need to Know

Your digital-asset transactions fit into two pots of charge, each charged at different rates and subject to different rules.

Capital Gains Tax (CGT)

It's the most frequently met charge. The taxman levies it on profits you earn if you sell or otherwise dispose of your shares.

How to calculate gains:

Sale Price (in GBP) - Cost Basis (in GBP) = Gain

Your "cost basis" is what you paid for it and any commission you paid to buy it.

Tax-free allowance (annual exempt amount)

In 2024/25, the tax exemption limit is £3,000. The first £3,000 of your net gains in a tax year are not taxable (reduced from £6,000 for 2023/24).

Tax rates (for 2024/25)

The authority altered CGT rates halfway through the year:

- 6 April 2024 – 29 October 2024: 10% (basic rate) / 20% (higher & additional rate).

- 30 October 2024 – 5 April 2025: 18% (basic rate) / 24% (higher & additional rate).

Example

You swap £1,500 for 1 ETH. You swap it for DOT when 1 ETH is £2,800. You have a chargeable gain of £1,300. That's under your £3,000 allowance, so you owe no CGT.

Income tax

That's where it matters when you get tokens as wages in some situations, as if it were a wage or a bonus.

When it matters:

- Staking rewards (if paid).

- Interest on lending (if paid out).

- Salaries (being received in tokens for work or services).

- Airdrops (if paid out as part of trade or commerce).

The value of the tokens at GBP when you are receiving them is added to your income balance that year.

As for taxes, your usual income bands will come into play (20%, 40%, 45%). It is not a preferential allowance; it's on top of your pay.

Once you've had these tokens and taxed them as income tax, they are now a capital asset. Further down the line, if you sell or exchange them, you may have to pay CGT on any future gain from then on.

Maximising Your £3,000 Allowance

Your annual exemption is your best friend. Clever traders use it to their advantage.

Tax-gain harvesting

If you have profitable crypto investments, you can actively sell enough of them in a tax year to bring gains to the value of £3,000, totally CGT-free.

But be careful: if you buy the same item within 30 days, the matching rule becomes dominant. This changes your cost basis and ruins the advantage. To avoid this, wait 30 days, and then you can buy back or buy a different but similar instrument (e.g., selling Bitcoin and buying a Bitcoin ETF).

Offsetting losses

You can sell declining assets to realize a capital loss. You can use the loss to offset gains for the same year. Should total losses exceed gains, you can carry forward the balance to offset gains in the future.

Your Action Plan for Compliance & Peace of Mind

Since good crypto investors often fall back on a good tax compliance checklist, here’s your compliance and peace of mind action plan.

- Record every transaction: This is essential. For every purchase, sale, trade, swap, or reward, you should record the date, value in GBP, and category of transaction.

- Use tax software: Connect with UK exchanges, automatically convert transactions to GBP, calculate gains/losses, and generate reports acceptable to HMRC. These software tools are great, but they’re no replacement for accurate records or professional advice.

- Consider a professional: If you're involved in complex affairs (e.g., high volume, DeFi, mining, or residence issues), an experienced accountant who knows about tokens is worth the money.

- Report through Self-Assessment: You'll need to report disposals and gains where overall gains are over the £3,000 exemption. Otherwise, you'll have to send in a tax return.

Inform it on the Self-Assessment Capital Gains Summary pages or through the online service. Avoid blanket thresholds; see the official "Do I need to pay?" guidance for your situation.

True confidence in crypto compliance comes from structure, not guesswork. 8lends helps financial institutions, fintechs, and enterprises implement governance, risk, and compliance systems that keep reporting accurate and audit-ready – no matter how complex the portfolio. When your oversight is unified, every transaction has a clear trail, and every filing stands on solid ground.

The Gifting & Inheritance Loophole

Another powerful but often underused tactic is gifting. Token transfers between spouses or civil partners living together are tax-free because the tax agency considers them "no gain, no loss". The recipient keeps the initial cost basis and has to pay CGT only if, or when, they later dispose of the asset.

For most, gifting is still a taxable event for the giver. It is worth a sale at market value at the time of the gift, which could trigger a charge to CGT if its value has increased since you acquired it.

But if the gift is to charity, it will usually be exempt from CGT. Note, however, that tokens are not considered "money", so Gift Aid will not usually apply unless first realized into money, and that realization can itself be sufficient to trigger a taxable event.

The Non-Dom & Residence Question

Your UK liability is extensively subject to residence and domicile. The remittance basis has been in force until 5 April 2025. However, its abolition came into effect on April 6, 2025, and was substituted with a 4-year Foreign Income & Gains (FIG) regime for certain qualifying new residents.

If you've previously relied on the remittance basis, transitional provisions may still tax remittances of past foreign income/gains; seek expert guidance before acting on historic assumptions.

In addition, when entering or leaving the UK, you must keep an eye on the Statutory Residence Test. You are only charged UK CGT for disposals while you remain a resident. Record meticulous travel movements before large disposals on a move.

Conclusion

UK taxes on digital assets are all about moving from fear to action. The regulations are straightforward, and there are allowances for a purpose. By knowing what constitutes a taxable event, optimizing your £3,000 allowance, and employing the proper tools to track activity, you can transform tax time from a headache into a quick review.

Knowledge brings clarity, but structure brings control. 8lends empowers organizations to manage compliance, documentation, and audit processes across multiple jurisdictions with precision and transparency.

See how 8lends can turn your compliance process into a seamless system built for growth.