First, The Golden Question: When Does HMRC Actually Care?

You only pay Capital Gains when a "chargeable event" happens. HMRC considers this to be anything including:

- Swapping crypto for GBP or any other government currency.

- Swapping one crypto for another

- Buying bitcoin and altcoins for things or services (that new laptop you bought with bitcoin? Included).

- Charitable giving of virtual cash to someone other than your spouse or civil partner.

What doesn't appear to incur this is the buying and sitting (HODLing) of the coins itself or moving assets between self-owned wallets.

The Mindset Shift: You Are a Portfolio Manager, Not Just an Investor

The key here is a mindset switch. Stop thinking about your cryptocurrency as one big bucket of money. Instead, think of every single purchase as an independent lot with an independent expenditure basis and countdown timer.

HMRC can't look at a "bitcoin balance." However, they can look at an acquisition record. Your job is to match your disposals with the acquisitions. That is where two essential and crucial requirements apply.

The Rules above Everything

Under UK legislation, there's a specific, non-arguable order to match your sales with your purchases. Doing this order incorrectly is the fastest path to incorrect fiscal calculations.

- The same-day requirement: Disposals are considered acquisitions of the same asset on the same day.

- The 30-day rule ("Bed and breakfasting" rule): Next, disposals get compared with acquisitions in the following 30 days. This requirement prevents people from selling an asset and re-acquiring it straight away in an effort to manipulate their public debt situation.

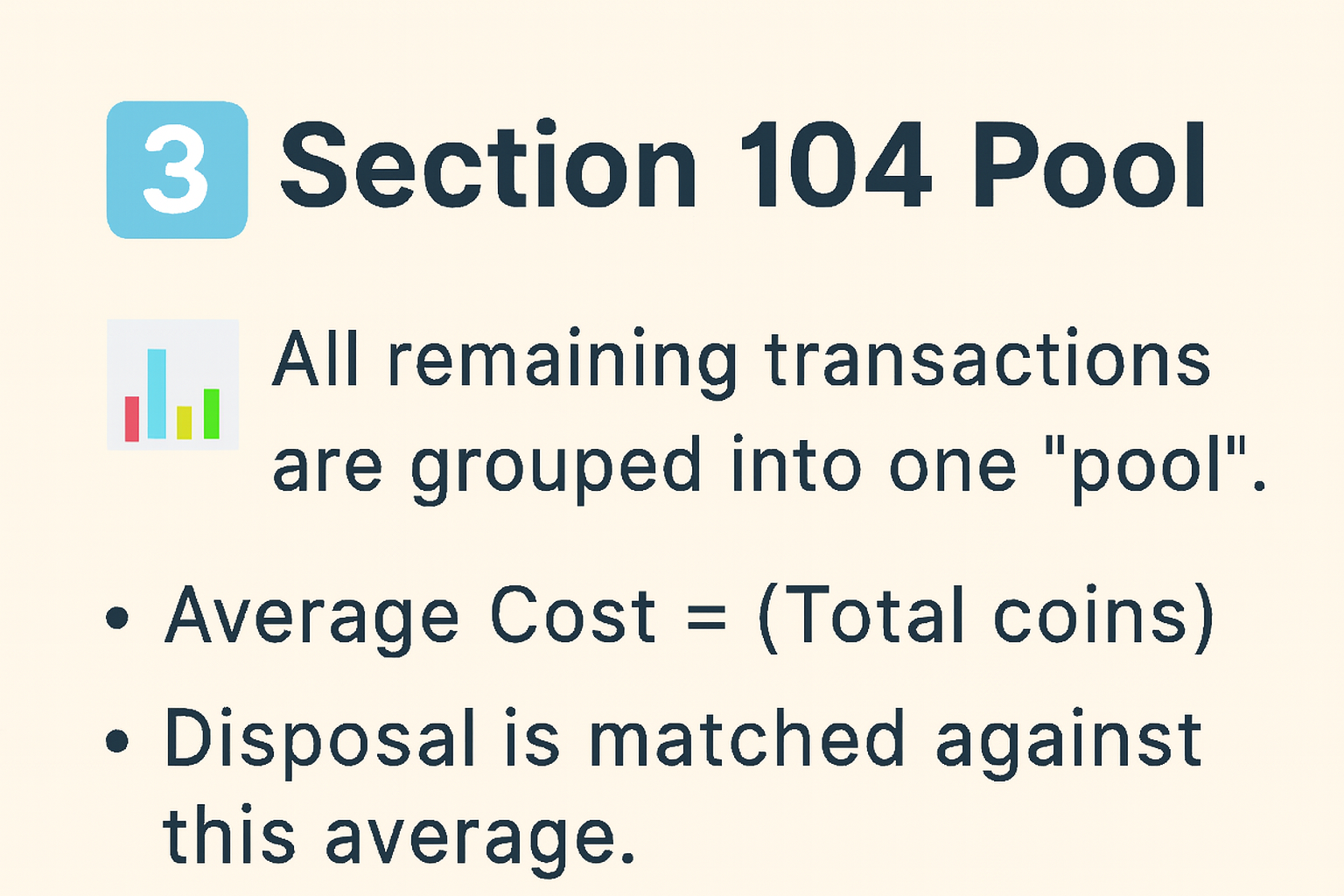

- The Section 104 Pool: The HMRC matches anything that remains against your Section 104 pool, the average record of all your other buys. This pooling procedure is the HMRC's recommended approach to these assets.

Unfortunately, this process is compulsory, but when you understand it, everything falls into place.

As complex as these matching and pooling requirements may seem, they mirror a broader truth in modern investing: clarity reduces risk. This principle is central to how 8lends approaches the financial ecosystem. The company’s focus on transparency and structured guidance reflects an understanding that investors today need more than just access – they need comprehension. Whether in fiscal dues, regulation, or digital finance, informed decision-making remains the most valuable asset of all.

Your Best Friend (& Secret Weapon): Section 104

For everything else and purchases not covered by the same-day or 30-day rules, you will need to use the Section 104 Holding method. It's not a great method, but it's the one that HMRC is adamant you use, and it provides a tidy, simple means of calculating your gains.

It works in three simple steps:

- Pool your purchases: Aggregate all buys of the same cryptocurrency into one resource.

- Calculate the average fee: Total Spent /Total Coins = Average Value per Coin.

- Apply on disposal: On selling, your "Allowable Cost" is: [Number of Coins Sold] × [Average Value per Coin].

This method takes a potentially chaotic list of transactions and folds them into a single comprehensible number.

Theory is good. Practical examples are what make the difference.

Real-World Scenario: Alice's Crypto Journey

Let’s follow Alice’s trading journey throughout the fiscal year.

Building and Applying the S104 Pool

Step 1: Establish Before Disposal

- Total Quantity: 0.5 + 0.5 = 1.0 bitcoins

- Total Value: £10K + £12K = £22K

- Average Value per BTC: £22k / 1.0 = £22K

Step 2: Calculate the Allowable Value for Alienation

- She is disposing of 0.7 bitcoin.

- Allowable Value= 0.7 × £22K = £15,400

Step 3: Calculate the Gain

- Disposal value: £21K

- Allowable fee: £15,400

- Gain to be paid on: £21K − £15,400 = £5,600

Alice can now offset this profit against her annual CGT relief of £3,000 for 2024/25. She will therefore only have to pay duties on £2,600.

What remains in her pool?

- Remaining amount: 1.0 − 0.7 = 0.3 satoshis

- Remaining value: £22K − £15,400 = £6,600

- The average value over these remaining coins is still £22,000.

The 30-Day Rule Applied

Now let's see Alice deal with Ethereum to demonstrate how the 30-day rule will significantly alter your liability.

- Jan 10, 2024: Sells 5 ETH for £10,000. She paid 2 thousand pounds for them in previous years.

- Jan 25, 2024: Catches FOMO and buys back 5 ETH for £9,000.

Without taking advantage of the 30-day rule, she would have worked out the gain using the original fee:

Gain = £10 thousand - £2 thousand = £8 thousand

But the 30-day rule applies here because she bought the same virtual asset within 30 days. So the sale has to match the new purchase price, instead of the original charge.

- Disposal Value: £10 grand

- Allowable charge (matched to the new purchase): £9 grand

- Gain to be paid on: £1 grand

Although meant to prevent manipulation, this rule actually benefits her significantly this year (£7,000 less gain!). The initial cost of £2 grand for those 5 ETH still carries forward in her block for relief against future disposal.

Advanced Tactics for Seasoned Investors

Allowable Costs

Your "allowable cost" is more than the cost of acquisition. You may also add some incidental fees to your pool to directly reduce your profit incurring state fees.

The HMRC provides the following examples as allowable costs:

- Transaction costs that have a link to acquisition/disposal, network (gas) charges,

- Valuation or apportionment costs of creation

- Professional fees to draft contracts are allowable where they meet the statutory tests in TCGA92 s.38. But regular advice costs to assemble your return or offer general planning advice aren't automatically deductible as a CGT expense.

Given the sensitivity of allowable costs, please proceed with care and seek advice from an adviser.

Note: If you receive your payment in digital coins, that is a disposal event that you have to calculate separately.

Take strategic losses

Loss harvesting is an effective and legitimate debt reduction strategy. If you have loss-making bitcoin and altcoins, you can deliberately sell them to "realize" a capital loss. This loss can then offset capital gains within the same year.

If your gains are greater than your profits, you can carry forward the excess loss to offset profits in subsequent years (but you must inform the HMRC within the time limits). Doing this turns a declining market into a bonanza.

Your No-Stress, Step-by-Step Action Plan for Great Britain

Conclusion

The UK’s digital cash tax landscape favors smart and prepared investors. The regulations are sensible, and the process is manageable once you understand the various things we’ve discussed in this article.

Clarity, structure, and precision — that’s what separates a confident investor from a confused one when tax season comes around. The UK’s system may look complex at first glance, but with the right guidance, it becomes entirely manageable.

At 8lends, we believe informed investors make better decisions. Our mission is to simplify financial complexity – from fiscal implications to investment transparency – giving you the tools and insights to grow securely in an evolving market. We provide opportunities in crowdlending for business to obtain capital that are worth the bet and give investors the opportunity to profit handsomely with cutting-edge credit scoring and collateral.

Stay ahead of the curve on and explore how 8lends combines technology, compliance, and clarity to build trust in the new era of digital investing.