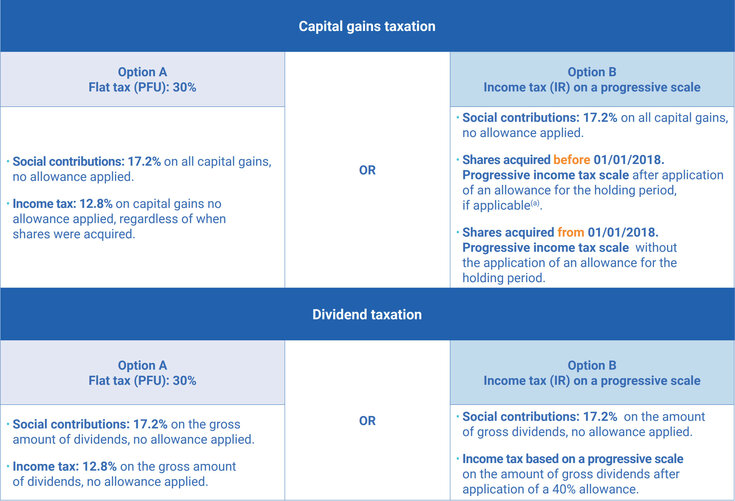

Decoding the 30% Flat Rate

For the sake of simplicity and appeal to a target section of the virtual investor public, the Prélèvement Forfaitaire Unique provides you the choice of a 30% route for your obligation on all your blockchain earnings. This is not only straightforward but also offers high earners the ability to make significant savings. Furthermore, the 30% is broken down into 17.2% for social security contributions and 12.8% as income.

This 30% strictly applies to your digital asset earnings and does not apply to your other sources of income, especially if you are also a high-income earner. You may see it as an additional savings to your earnings if you already fall into the 41-45% bracket. Again, for exceptionally high virtual profits, an additional maximum rate of 4% applies, further increasing the effective rate for wealthy investors.

But who benefits from this 30% constant rate? They include individuals with annual earnings above €78,570, investors managing a significant number of portfolios, high-net-worth personalities, and individuals seeking simple fiscal administration. So, it might be suitable for you if you are in any of these categories.

Choosing between the stable and bracketed choice may sound like a simple math problem, but in practice, it’s much more strategic. Small details – such as how your gains are recorded, which accounts you use, and the type of investor classification you fall under – can change your total liability significantly.

That’s where 8lends comes in handy. By automating digital cash accounting and providing precise compliance tools, it enables individuals and organizations to evaluate each tax route with accurate, data-driven insights. Instead of navigating complex French rules alone, you can make confident, well-documented decisions that align with your income and investment strategy.

Understanding the 0-45% Bracketed Alternative

The alternative payment schedule is the increasing kind, where you climb higher up the ladder alongside your revenue. However, there is a need to understand its functioning to make sound financial decisions. Here is the breakdown in the table below.

But here is a key insight many gainers who fall between 0-11% often miss: you have the opportunity to waive the 12.8% income tax under the progressive system.

This leaves you with only the 17.2% social security contributions and 11% income. For instance, suppose your earnings are €5,000 annually as an income earner within the 11% bracket.

This means your total income gets levied 28.2% (11% + 17.2%), which is less than the 30% stable system. In the end, you’ll pay €1,410 instead of €1,500, effectively saving €90, and this is just a modest example.

Doing the Math

Now, let’s consider some real-world investor scenarios to help drive home the reality of these choices and how best to approach these decisions.

- Scenario one: take a modest virtual cash investor with a €22,000 annual income and a gain of €5,000. This investor should opt for the progressive route. It brings their total obligation to 28.2% (11% + 17.2%), resulting in a total fiscal value of €2,256, compared to €2,400 if they had opted for the constant rate. Annual savings are €144.

- Scenario two: imagine a mid-tier professional making €50,000 annually, with a gain of €12,000. Income range falls in the 30% range, so it is better to pay a steady rate of 30% (€3,600) than an incremental obligation, which includes the 30% + 17.2% (47.2%) with a value of €5,664. Annual savings are €2,064.

- Scenario three: is a high-net-worth individual with €120,000 annual income and €25,000 digital cash earnings. Their income range is 41% + 17.2% (58.3%), bringing it to €14,550 for progressive duties and €7,500 for the steady route. Annual savings are €7,050.

These three distinctly different scenarios give you a quick reference when deciding the obligation payment method that is best for your situation.

Factors Influencing Your Strategic Decision

Now that the math is sorted, you can consider specific factors that may positively influence your strategy.

It is often beneficial to choose the constant duties option when your top priority is simplicity in fiscal administration and you prefer a predictable plan. It is also better when in the 41-45% bracket or when you have significant proceeds. If your income range exceeds thirty percent and most of the income comes from your virtual cash investment, then choosing the thirty percent constant method will be wiser.

On the other hand, the progressive tax method is often favorable if your income tax bracket is less than thirty percent and also if complex calculations are not for you. Again, if a huge chunk of your income is not from virtual coins and if you’re looking to optimize your obligations by spreading it across all revenue sources, that suggests a bracketed system.

Looking critically at these considerations hints at the thirty percent as the break-even point. This means that you generally want to adopt the constant route once your income tax bracket shoots above the thirty percent mark. Below this mark, the brackets will work out better for you.

The Multi-Year Perspective

Frankly, having a long-term strategy is often beneficial than the knee-jerk reaction many investors have to the yearly cycle. This will mean an active system in place for managing fiscal obligations beyond one year. Here are some strategies you can adopt that can help.

- Monitor all sources of income to effectively track and anticipate the effective amount of income duties due

- Coordinate your virtual cash strategies with other income sources

- Evaluate each transaction to ensure that they are within a more advantageous tax bracket

- Plan the timing of your sales to take advantage of a favorable fiscal choice

Essentially, assess how every decision helps you build wealth, especially when choosing an optimal government duties system. You’ll make huge savings by consistently choosing the best system each year, which may lead to much wealth if reinvested over the years.

Additionally, you should consider the possibility of future income affecting your choice. Promotions and salary increases, salary reduction due to job change, or retirement are some factors that can affect your future choices and should be considered critically.

Common Misconceptions That Cost Money

The dual system in France, though unique, is simple with a few dynamics. Yet there are misconceptions around its operation, with many becoming well-circulated myths.

- Myth 1: Many believe they can apply different rates to different crypto earnings. The truth is that all gains made from cryptocurrency are treated uniformly within the bracket the earnings fall in.

- Myth 2: "You can negotiate social contributions." The reality is that the social contribution of 17.2% is a mandatory fiscal obligation as a French resident, irrespective of your option.

- Myth 3: "Your fiscal choice is unchangeable once made." You have the choice to change your mind on the method you choose every year.

- Myth 4: "The even rate of thirty is always the simpler choice." The truth: though that percentage remains administratively simpler; nevertheless, your choice between the two options will not always be that simple, as this predictable percentage might not always be the best option every year.

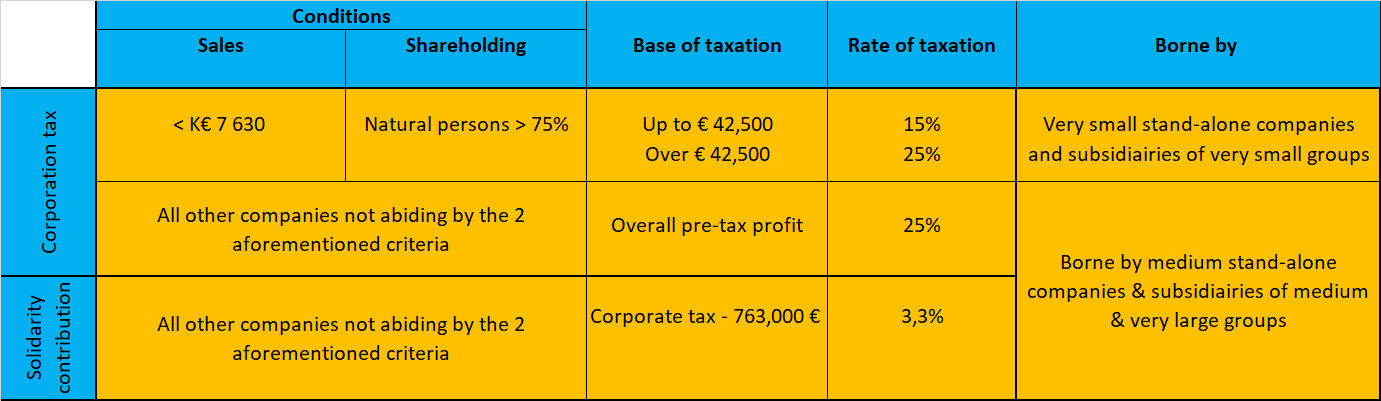

- Myth 5: "Professional and occasional crypto investors have the same choices." Here, the professional investor can leverage some opportunities and advantages, such as the micro-BNC allowance under the BNC regime with different rules applying.

All of these underscore the necessity to keep abreast of recent developments on the fiscal landscape. This will help to make informed and strategic decisions so that you don't make any financial errors.

Looking Ahead: Planning for Future Changes

The crypto landscape and the laws governing it are ever-changing, and Paris’ crypto laws, especially legislation on government payment obligation, are no exception.

Although there have been recent discussions around a potential future increase, particularly for the thirty percent model, this hasn’t been implemented. Still, investors will need to start considering its break-even impact analysis to see if the progressive option becomes the better method.

Most importantly, strategic adaptability, including amendments in casual and professional trading. Also, being updated about international fiscal treaties and any changes to social contribution rates will prove beneficial in your strategic adaptation.

Conclusion

In a nutshell, France gives you the freedom to make your choice of two options. However, the responsibility to make the best decision is also automatically conferred on you.

This unique flexibility is often seen as a plus when compared to other countries, but making the right choice will also require staying current with the relevant information needed to make informed financial decisions. Ultimately, the crypto landscape will continue to shift, but also remember that you have a choice. Always reevaluate your choices as your situation changes and readjust to one that is most beneficial to your financial reality.

Deciding between France’s 30% flat tax and the 0–45% progressive system is more than just a yearly choice – it’s a long-term financial strategy. The key is having a system that tracks your income, gains, and deductions with absolute accuracy. 8lends delivers exactly that. With automated crypto compliance, integrated reporting, and up-to-date regulatory alignment, you can stay informed and fully compliant while optimizing your returns.

Plan smarter, reduce uncertainty, and take control of your crypto tax strategy with 8lends.