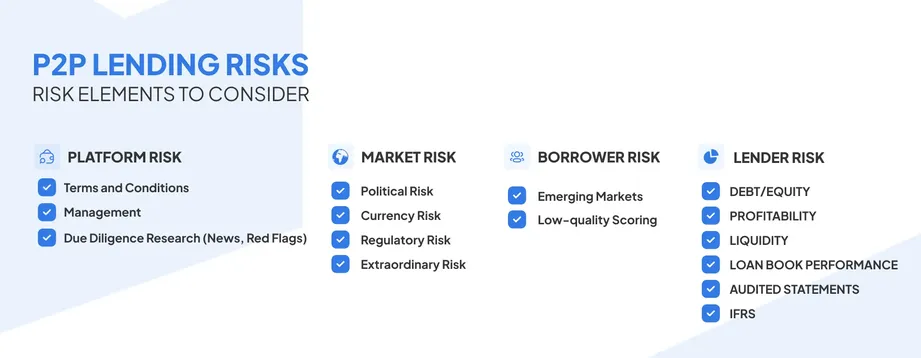

Why Platform Risk is Often Overlooked

Whenever individuals think about risk in peer-to-peer lending, they typically consider the borrower. What happens to the borrowers when they default on the loan? Do they have a good credit history? Those are good concerns. However, they are just part of the story. The platform is probably the biggest unaccounted-for risk in P2P lending.

Investors assume that a platform is running if it is safe. But sometimes that isn't so. A platform may be poorly managed, underfunded, or poorly overseen. And even borrowers making repayments might not save investors from losing access to their money if that platform fails.

Many retail investors skip this altogether. However, understanding platform risk is as important as evaluating a loan on a case-by-case basis.

Why Platform Risk Matters

P2P platforms facilitate the entire loan lifecycle by matching investors with borrowers. They:

- Vet and list borrowers

- Handle payments & repayment schedules

- Manage communication and collection

- Offer investor dashboards and updates

When this middleman collapses, things get messy. If a borrower continues to pay, who collects that payment anyway? Who makes sure it reaches you? Who handles disputes?

Without strong safety measures, your investment may be stranded, or even worse, completely lost.

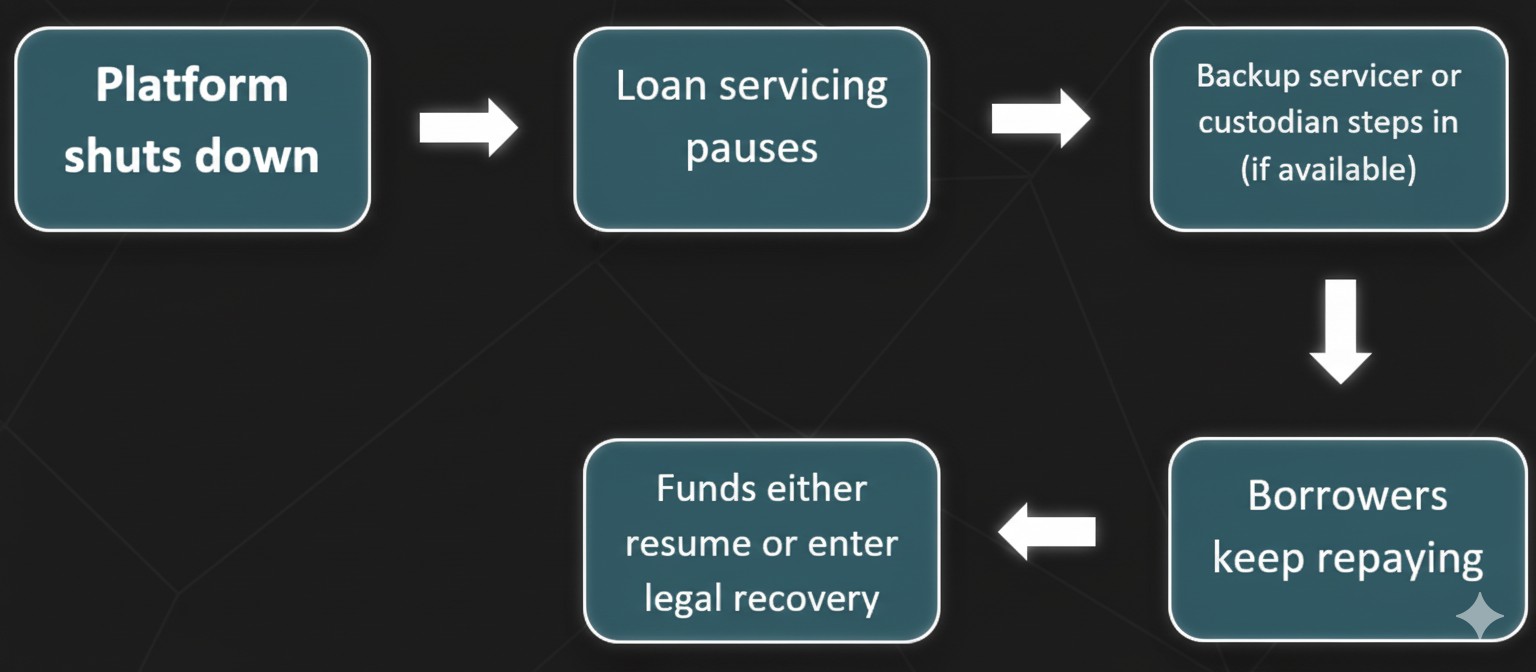

What Happens if a P2P Platform Fails?

A platform failure does not necessarily mean your money is gone. However, recovering is complicated by many factors. These include:

Disrupted Loan Servicing

Backup servicers keep track of repayments and borrower communications if the platform fails. If the platform goes down and no backup servicer is available, payments from borrowers could stop. Communications would break down, and you may not receive your expected income.

Custodian Account / SPV

Reputable platforms often protect investor money through Custodian accounts / Special Purpose Vehicles (SPVs). This keeps investor funds separate and ensures they are less likely to disappear with the platform.

Activation of Backup Servicer

Some platforms have agreements with third-party servicers that can take over loan management when required. This may keep repayments up and limit losses.

Bankruptcy and Legal Process

Investors become unsecured creditors if the platform goes bankrupt. What this means is that you might get only a fraction of your money back. And even that may take months or years.

Real-World Examples of Platform Failure

Lendy (UK, 2019)

Lendy was once one of the top peer-to-peer lending platforms in the UK and yet things went wrong. The firm entered administration in 2019 after there was an increase in default rates and increased concern over poor transparency. The failure of the loans was worth more than 160 million pounds and years later there are still investors waiting to be paid back in full.

Grupeer (Latvia, 2020)

Grupeer, a P2P platform operating in Latvia, suffered platform failure; its sudden freezing of the withdrawals caught its users completely unexpectedly. It would be later realized that all the listed loans on the platform had some fake loans. Most investors sustained huge losses, especially with the lack of a straightforward plan of recovery and legal options. In most of the instances, the amount recovered was less than 20% of the original amount invested.

These examples demonstrate that a platform's power and regulation create a significant impact on whether investors retrieve funds or not.

8lends is a Swiss-based crowdlending company built with platform security and long-term investor protection at its core. With regulated operations, robust credit vetting, and transparent loan structuring through SPVs, 8lends offers not just strong returns – but peace of mind that your capital isn’t left exposed to platform chaos.

How To Know if a Platform is At Risk

Several signs can suggest trouble is coming.

Red flags also include sudden shifts in strategy. For example, switching from low-risk consumer loans to high-risk crypto assets without sufficient transparency. If you notice one or more of these, it's wise to consider exiting early.

Factors That Determine Recovery Success

Recovery depends on several technical and legal factors:

Visual Guide: What Happens When a Platform Collapses

Zopa’s Pandemic Response

Zopa, a regulated UK P2P platform established in 2005, ended the early 2020 market turmoil quite differently. Zopa implemented some protections and still operated despite investor withdrawals.

They froze new loan listings and capped withdrawals temporarily to maintain liquidity.

Weekly updates on portfolio and loan book performance were sent to investors. Zopa used its well-capitalised reserve and backup mechanisms to keep borrower repayments flowing.

Consequently, the platform did not collapse, and most investors continued to receive repayments. Zopa was transparent and prepared. And this proved to be pivotal in weathering a stressful period. This crisis-tested resilience bolstered Zopa's reputation and later helped it to gain traction as it transitioned to a fully licensed bank.

Risk Types

It’s important not to confuse platform failure with borrower default or other types.

Even if a borrower is paying on time, you won’t get your money unless there’s someone to process and pass on that payment.

Steps to Protect Yourself

Here’s what you can do:

- Confirm Custody Arrangements

Verify that the platform uses separate accounts or custodians. Avoid platforms that jumble investor money with operating cash.

- Understand the Legal Setup

Do loans under your name exist as SPVs or security? If so, they can be transferred more easily if there’s a collapse.

- Know Where It’s Regulated

Licensed platforms are generally safer, for example, the UK's FCA. Other jurisdictions are more risky.

- Diversify Across Platforms

Don’t put all your money on one platform. Consider 2-3 reliable ones, as they will reduce your risk tremendously.

- Monitor Platform Health

Watch for delayed withdrawals, broken dashboards, or long silence. They are all early warnings of trouble.

- Keep Your Own Records

Download contracts, payment schedules & communications. They might be crucial in legal proceedings.

Summary Table: Platform Risk at a Glance

Final Thoughts

Platform risk isn't flashy, but it's real. It can be easy to get lost in interest rates and borrower profiles and not consider the platform itself as the glue holding everything together. The good news? You can minimize this risk by doing a little homework upfront: Pick regulated platforms, custodians & SPVs, lend across different asset classes, and be on the lookout.

Looking for a platform that takes your capital seriously? 8lends is redefining peer-to-peer lending with one of the most advanced risk-management frameworks in the industry. Whether you care about borrower quality, loan transparency, or long-term platform viability – 8lends delivers on every front.