Understanding the Dual Framework

Different European countries operate different virtual cash duties regimens, but here's where France switches things up. Its unique dual taxation system targets gains from blockchain transactions. Interestingly, this gives residents some options and flexibility on how they want to pay, legally minimizing their duties.

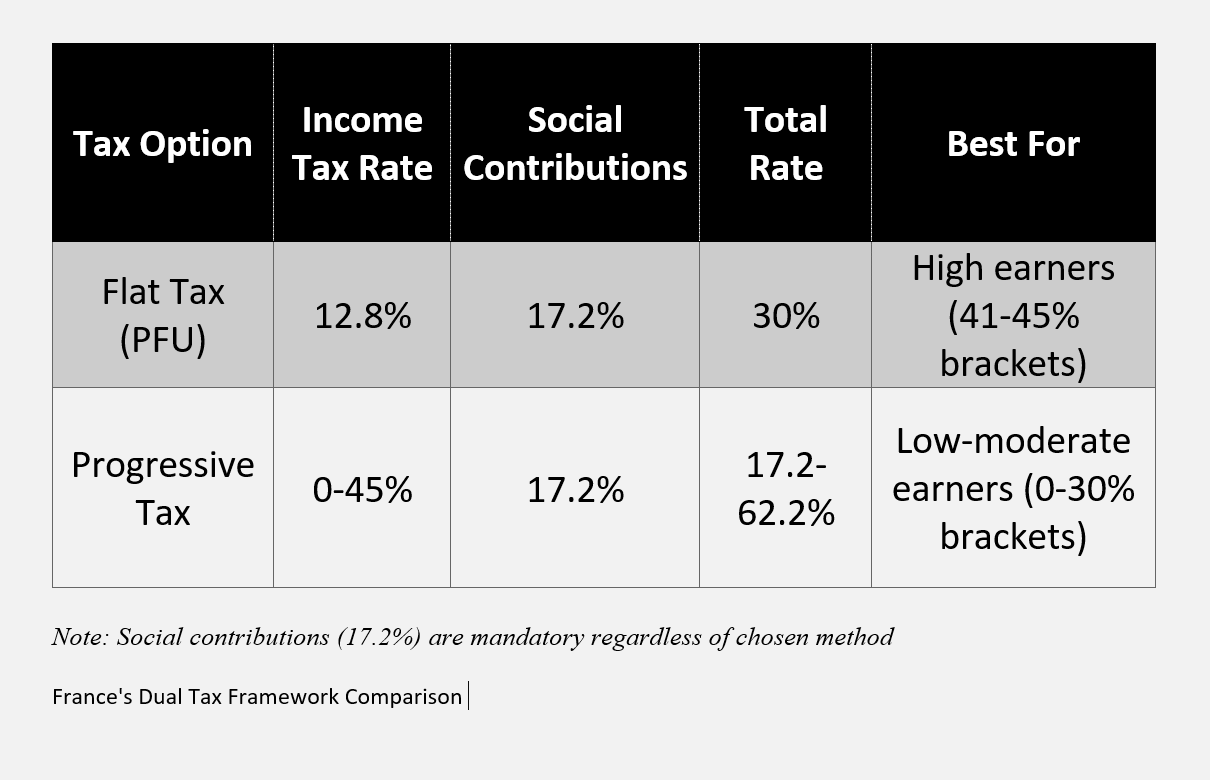

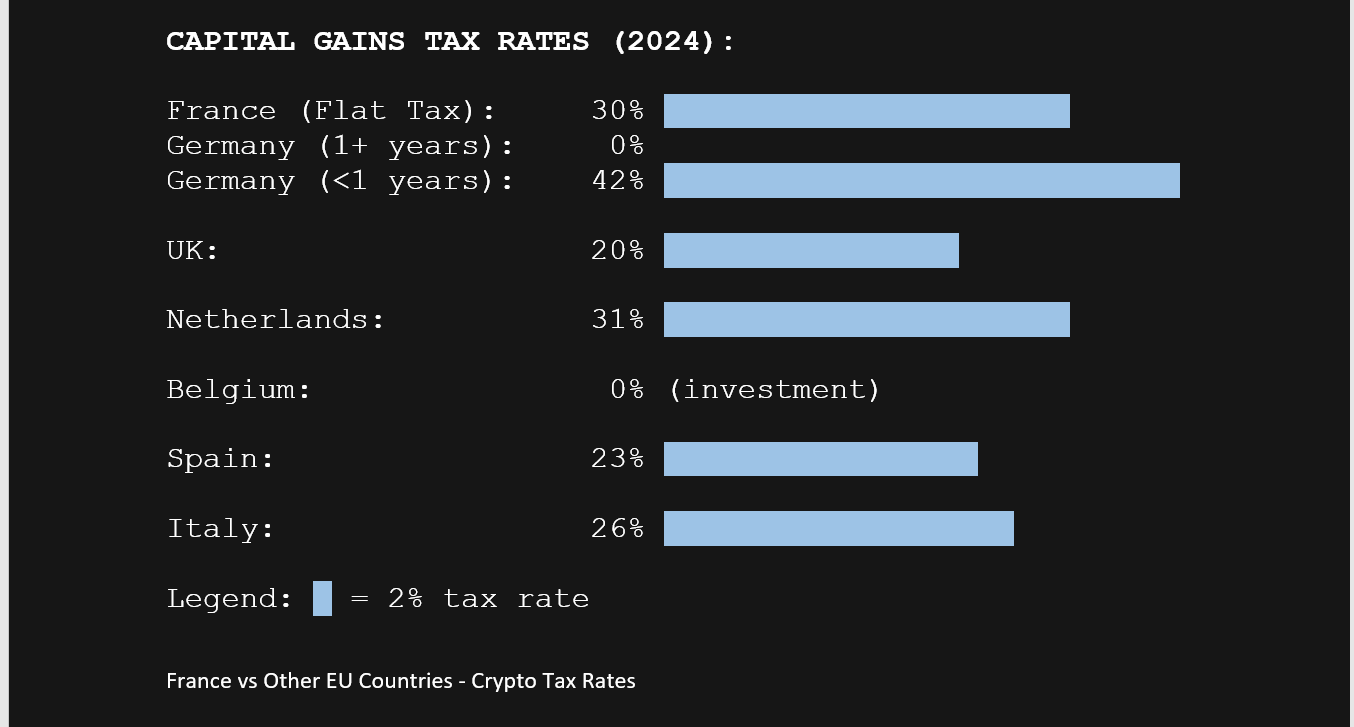

The Flat Option limits what’s levied on digital currency investors to 30%, with 12% for income and 17.2% for social contributions. If you are a high earner in the blockchain market, this would be a better option than the progressive option.

The progressive option is an alternative option (0-45%), which also includes the 17.2% social contributions. The gain here is the lower debt for lower-income individuals. Nevertheless, you still must choose an option, as it is not automatically calculated.

The €305 Tax-Free Threshold: France's Hidden Gift

Investors stand to benefit here on both gains and alienations. This is France’s hidden gift to small investors that can maintain that threshold. While it might seem like a token, those strategizing with dollar-cost averaging will find it beneficial.

The strategic implications of this can be rewarding if applied well. For instance, postponing a December payment that would have given you some capital gains till January is a smart move. This helps you maintain your threshold for the year. Still, exceeding the threshold within the same year does not accrue additional charges.

What Triggers a Taxable Event?

Now, how do you know you’re due for levies? In France's virtual cash terrain, there are some unique markers.

Obligation-triggering events often include virtual coins-to-euros conversion, making purchases with digital assets, and receiving payment in it.

For non-fiscally-related events, conversion between digital currencies is uniquely free of charges for French investors. Euro to digital coin conversion, moving coins between your personal wallets, holding virtual money without selling and trading virtual cash for NFTs, stablecoins, or tokens also do not require payment.

These categorizations of different events requiring government payments distinguish France from the rest. Jurisdictions like the U.S. operate with stricter rules. This allows investors to rebalance portfolios and switch between digital assets without immediate levies, giving them a huge leverage for dynamic portfolio management.

Professional vs. Casual Activity Classification

Frankly, your blockchain activity sheet could determine what you’d pay. Again, the DGFiP makes a critical distinction between professional traders and casual investors to determine what rate applies to you and your entire framework.

Casual Investors, according to DGFiP, include blockchain activities liable with the €305 exception under the capital gain regime. Also, occasional trading activities, accessing favorable progressive or flat options, and long-term virtual currency holding all of which also fall under the capital gains regime.

Professional Trader classification includes short-term speculation pattern, consistent trading activity, and blockchain transactions you’d pay on under Bénéfices Non Commerciaux (BNC) as business income. Also, blockchain trading with a 34% allowance on annual turnover up to €77,700 is often accessed through the micro-BNC scheme.

When determining your classification, DGFiP places a microscopic focus on your trading tools, trading strategies, and trading frequency. Additionally, the DGFiP also checks if trading is your primary source of income. However, you could be wrongly classified as a professional trader, which you can challenge with evidence. Hence, the documentation of your trading becomes a critical requirement for this inquiry.

While understanding your classification is essential, maintaining accurate documentation is what truly protects you during audits or reviews. Specializing in governance, risk, and compliance solutions, 8lends helps organizations and investors implement robust frameworks that make financial and regulatory tracking effortless. Whether you’re documenting wallet movements, exchange records, or reporting to the DGFiP, 8lends ensures your compliance processes are streamlined, verifiable, and audit-ready.

Mining and Staking: The Complex Frontier

A distinctive type of tax challenge often accompanies staking and mining. As such, they are treated based on regularity, scale, and purpose.

Mining activities are generally classified under BNC as professional income, and rewards require state payment as when received at the fair market price. However, expenditures such as operational costs, electricity bills, and equipment depreciation are deductible.

Staking rewards, in contrast, vary significantly in their treatment. For example, while large-scale staking operations often fall under BNC, small-scale staking can become eligible for capital gains treatment. More importantly, a decline in asset values can result in a cash flow challenge, depending on the event timing.

The challenge here is one of valuation, as you need to calculate the fiscal value of your digital cash rewards immediately it's received, which can be challenging for a market that operates around the clock across different time zones.

Record-Keeping Requirements

In France, fulfilling your fiscal obligations goes beyond calculating your fiscal figures. You’ll need to be thorough in ensuring an accurate sum. Hence, an expectation of a comprehensive documentation similar to a professional accountant’s work.

Here are the essential records expected of you in your virtual cash clarification with the French budgetary authorities. All prices are in euros.

- Prices and dates of purchase

- Bank transfer records

- Prices and dates of sale

- Exchange rate during transactions

- Total transaction fees and costs

- Exchange statement screenshots

- Transaction hashes and wallet addresses

Other documents considered advanced, especially for complex portfolio managers, are detailed spreadsheets tracking portfolio activities and records from professional software. Furthermore, data backups for exchange APIs and legal opinions on classification options should be included.

The digital footprints left on blockchain platforms count as your paper trail for all transactions. For this reason, the fiscal department can analyze blockchain to monitor your activities. This makes accurate self-reporting both strategically wise and ethical.

Penalties for Non-Compliance: The High Stakes Game

With their generosity in allowing certain advantages, it is only natural that stringent measures would be against those trying to evade their obligations. Some of these penalties are:

- Each Undisclosed wallet carries a €750, and misstatement or omission carries €125 each, capped at €10,000 per declaration

- Undeclared gains carry a 40% fine

- Undeclared foreign accounts carry an 80% fine

Double penalties are implemented when wallet values exceed €50,000 at any instance of the fiscal year. Also, criminal charges may follow a proven case of serious violation. Additionally, holders of foreign virtual cash accounts are required to declare in a Form 3916-BIS. Failure to declare will result in stern penalties.

Planning for Tax Season: Your 2025 Action Plan

There’s no last-minute approach when it’s the French virtual coins liability season. This is because you have a whole year to prepare. For instance, France’s income statement declarations opened on April 10, 2025, for the 2024 fiscal year. This means you should have prepared your report before then.

Here are some key preparation steps for you to consider when compiling your return.

- Gather all your transaction records together, including purchases and sales, exchange statements, and wallet transaction histories,

- Ensure you sum up your disposals to confirm if you’re still within the €305 threshold

- Evaluate the filing options (flat or progressive) to determine your best option

- Identify and complete the required form for your regimen (2042, 2042-c, 2086, and 3916-bis)

- Seek professional consultation when faced with complex circumstances.

Interestingly, several platforms leverage advanced technology to help you stay on the right side of French legislation. Some of the pitfalls to consider, especially as a French investor, include combining both business and personal virtual cash, disregarding the dual fiscal option, and missing out on foreign virtual currency accounts. Failing to consider these pitfalls might cost you dearly.

Conclusion

In a nutshell, mastering the French crypto fiscal landscape entails understanding a complex but unavoidable system. Successful investors understand their classification as either a professional or casual trader, and then maintain a perfect record. In addition, they optimize the tax options available and are abreast of regulatory changes.

Furthermore, with about 6.5 million owners of virtual assets in France, the parameters for tax collection encourage compliance. This, in turn, fosters a more favorable fiscal environment. As the crypto revolution continues to move at a bullet speed, your tax preparations must be in sync with your records.

While understanding your tax classification is essential, maintaining accurate documentation is what truly protects you during audits or reviews. 8lends specializes in governance, risk, and compliance solutions, It helps organizations and investors implement robust frameworks that make financial and regulatory tracking effortless. Whether you’re documenting wallet movements, exchange records, or reporting to the DGFiP, 8lends ensures your compliance processes are streamlined, verifiable, and audit-ready.