Reference Point for Debts on Earnings

Since the present piece isn’t a masterclass in digital assets jargon, let us simplify things to their ones & zeroes. Whenever one shells out for a crypto token or coin, they compensate via a specific £ price for it – the original price. The original sum in pounds with any extra fees tacked onto it for the operation or charges from the platform is what the state goes on to form what’s called the “cost basis”.

At some point, every UK DeFi investor ponders whether the government gives a hoot about that. Assuming you’re harboring similar thoughts or are currently wondering about it, let’s lay that to the wayside.

Significance for Crypto Duties

Since the foundation for cost basis is the charges to get one’s hands on a cryptocurrency plus all the extras involved in the pursuit thereof, that renders it absolutely crucial to know number-crunching procedures like the back of one’s hand as one’s assets abound. Since one must pay duties on them.

Fortunately, legislators hate complexity, simply considering that complex duties guidelines turn enthusiasts off. Hence the foolproof math they’ve devised.

This formula helps one arrive at one’s wins & losses. Furthermore, a higher reference point lowers the appreciation paid on. Let’s reemphasize that for clarity.

Even if you don’t remember much about high school algebra, you probably recall your algebra teacher, Mr. X/Y, saying something along the lines of “knowing a formula is one thing; applying it is a whole different ballgame.”

That statement rings true here, and its meaning is perhaps why UK decentralized finance enthusiasts struggle to get this part of their state charges right, especially due to pooling rules.

Complexity is often what discourages people from taking control of their own finances – and that’s exactly where clarity becomes power. It’s the same ethos driving 8lends'approach to explaining taxation and compliance: breaking down what feels impenetrable into something that makes sense, even to the non-specialist. After all, understanding is the first step toward confident investing.

There are 3 British calculation guidelines to know.

3 Ground Rules for Calculation

UK virtual coins investors should know the following three rules:

- The same day rule

- The 30-day rule

- The section 104 pool

These requirements run in order, so let us focus on each one individually.

Same Day Rule

Imagine a scenario where one unloads one 1 satoshi at £100,631.41 today (10/7/2025) and purchases a single satoshi for £85,631.41 immediately after. Your cost basis for the vended satoshi is what you shelled out for that single satoshi you acquired.

This is the 1st virtual cash fiscal obligation applied by UK. The fiscal authority matches same-day crypto alienations and token acquisitions.

In other words, the single-day-window framework assumes precedence since timing doesn’t affect it: the state pairs same-day transactions first.

Therefore, within the framework:

Since you’re taking on profit, HMRC will await you to pay unto Caesar what belongs unto him: duties off your wins.

30-Day Period

Following any matching-day operations on wallet addresses, they turn their attention to happenings within a 30-day period and put into effect the bed and breakfast rule.

That distinction is foundational since during your investment career, you encounter instances where your best interest is to alienate coins under explicit intent of repurchasing them fast, quicker than a month.

The UK has determined:

- The sale counts as alienation (budgetary agency assumes since you unloaded it, you therefore accrued and ought to report).

- Should the buyer and you agree on one single purchase and repurchase simultaneously, it doesn’t count as capital-reaping alienation.

When you sell and buy the same virtual cash within 30 days, the authority expects you to match the buy/sell over the month.

Suppose:

- On January 5, 2025, you buy 1 ETH for £3,000 and pool it using Section 104 holding (more on this in a bit).

- On January 15, 2025, you sell 1 ETH for £3,300.

- On January 20, 2025, you buy 1 ETH for £3,000.

Since the 24-hour requirements won’t factor into that history, the tax body will exercise the 30-day rule since it’s all within a month.

To calculate your book value in this case, match selling/buying like:

- On January 15, 2025: Sold 1 ETH for £3,300.

- On January 20, 2025: Bought 1 ETH for £3,000.

- In this example, you’ve realized a taxable £300 capital gain.

Although it seems unfair, that requirement ensures everyone stays ethical. The state authority implemented it upon realizing that supposedly shrewd investors would sell securities to go into red to not have to pay the government, but then rebuy them.

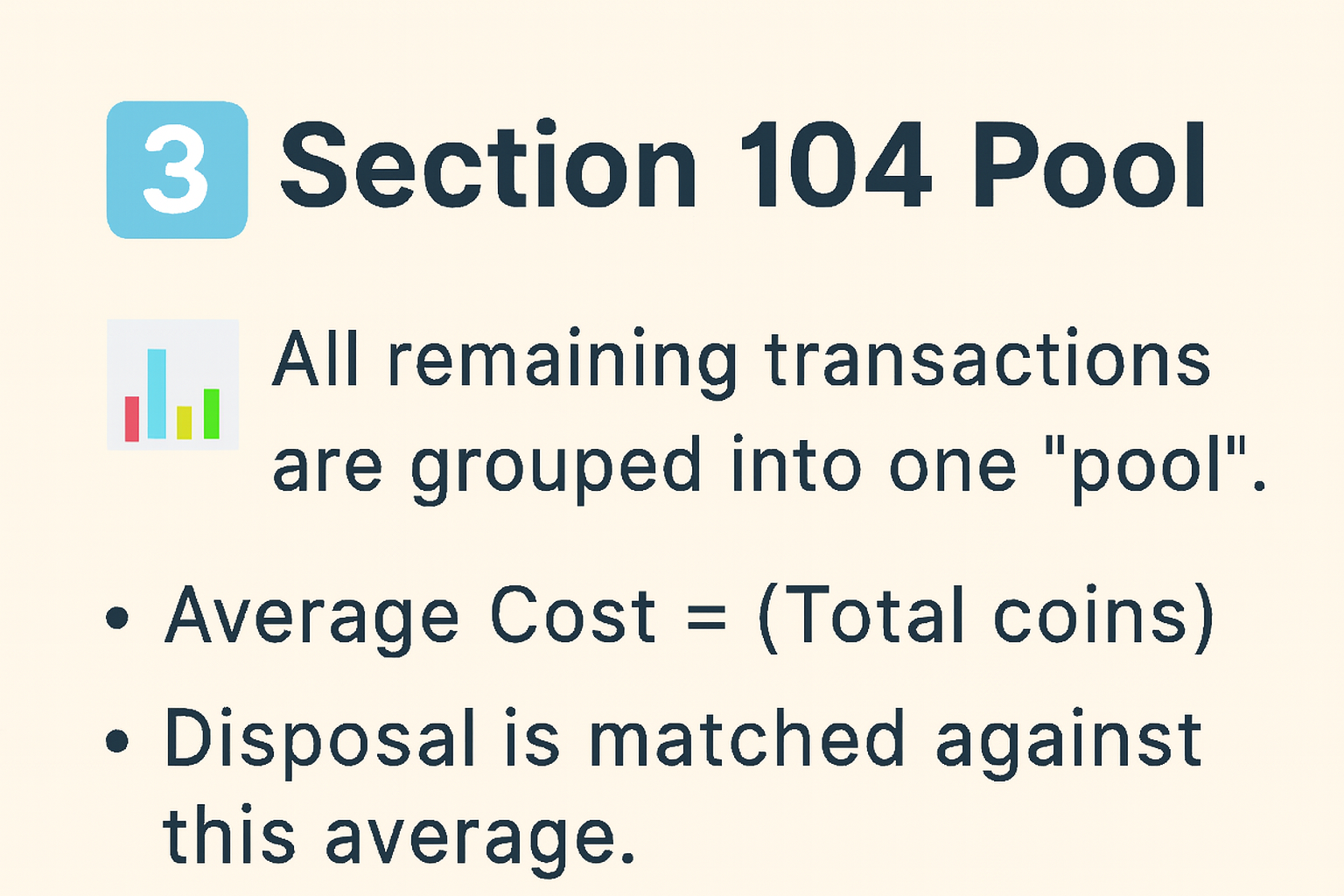

Section 104 Pool

Where blockchain dealings don’t qualify as matching-day or month, Section 104 pooling comes into play.

This dumbs down virtual cash computation because the HMRC creates an S104 pool for similar digital assets. Suppose you’d sat on your Monero for more than a month. That generates a Monero pool. So you then procure additional Monero and keep them for over a month. Those automatically enter the pool.

The tax basis here is the overall procured amount over the denominator of total held assets. Suppose 3 bitcoins were bought at different prices, intending to hold them.

Here, overall charges are £286,262.41. Since you held onto three bitcoin, the pool’s default book cost is the sum bought with the denominator of three bitcoin – £95,420.80 in the present case.

After covering these obligations, you’re probably despairing and entertaining thoughts like, “The taxation regimen will eat the largest share of the pie of my trading gains.” Don’t despair.

The authority wants you to succeed so you can pay taxes for longer. That’s why they have allowable expenses and deductions every blockchain investor should know:

Key Value Foundation: Considerations and Tax Deductions

Quick refresher here.

Disposals

We’ve mentioned disposals a fair amount in this article, but what exactly counts as a disposal?

Capital gains-wise, disposals are anything that involves:

- Exchanging one token for another, for example, trading TC for ETH.

- Using digital money to pay for products and services.

- Giving virtual cash to anyone besides a civil partner or registered charity.

- Selling cryptos for GBP, USD, and other government currencies.

Anything within these parameters will attract capital gains taxation under the three rules.

Deductible costs

Some things you can deduct from your cost basis after calculating it:

- All transaction fees related to buying and selling your bitcoin or altcoins.

- Related professional fees.

- The original British Pound price of purchasing your virtual assets.

The Annual Capital Gains Exemption

The government gives every UK duties payer an annual capital gains exemption. For the current year (2024/25), it is £3,000. Remember to deduct this against your capital gains that have to be paid on; that is the most government-allowed way to pay a lesser financial obligation.

Conclusion

Fulfill these obligations on all bitcoin and altcoin operations to stay on the straight and narrow. From everything we’ve discussed, it’s clear the power that records have as a compliance weapon. UK requires duties on crypto, mining, and staking. Don’t let that fine print mess up your compliance status.

If you’ve made it this far, you’re already ahead of most investors — because you’re learning to master what others avoid. That’s precisely what 8lends was created for: to make financial intelligence as natural as breathing, whether you’re dealing with taxes, tokens, or tomorrow’s opportunities.

Discover how 8lends helps investors cut through the noise – and take control where it matters most.